FEATURE-1: What is for iron ore in ‘20 after dramatic ’19

Will the history repeat itself or will now be the turn for the Chinese steel mills to be at the centre of the stage for 2020?

A turbulent 2019 – a battle between demand and supply

Last year, iron ore supplies from both Brazil and Australia, the world’s two core production countries, went through rather unexpected disruptions in the first half with Vale’s dam collapse on January 25 and the severe Tropical Cyclone Veronica sweeping Pilbara over a weekend in late March, and the aftermath, especially from Vale’s accident, last throughout the whole year.

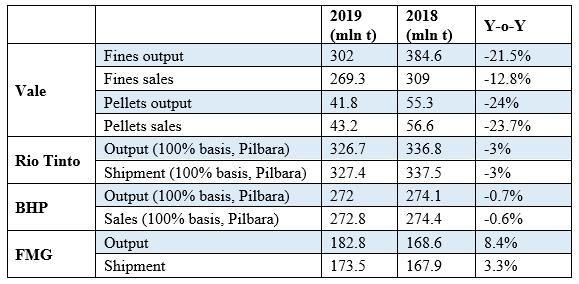

The impact on global iron ore supply, however, turned out to be less severe than many market participants had feared, especially with the variable in Vale, as the company shared its estimation that 92.8 million tonnes/year iron ore capacity including both fines and pellets would be affected by the accident, and it lowered its iron ore and pellets sales guidance for 2019 a few times to 307-312 million tonnes.

In reality, though, for 2019, the company’s iron ore production including fines and pellets fell about 96 million tonnes on year to 343.8 million tonnes, while its sales for the two forms of iron ore totaled 312.5 million tonnes, even higher than the upper range of its guidance, or down about 53 million tonnes, as it had used stocks in its whole process to make up for the gap and to best safeguard its market share.

For 2019, Australia’s top three iron ore miners of Rio Tinto, BHP and Fortescue Metal Group (FMG) all trimmed their respective iron ore production or shipment guidance for the calendar year or their FY2019 (July 2018-June 2019) because of the cyclone, but all ended on a higher note with the catch-up in the following months.

By the end of 2019, Rio Tinto’s Pilbara iron ore shipments fell 10.1 million tonnes or 3% on year, while BHP’s volume was almost flat from the previous year, and the shipment from FMG was even up 5.6 million tonnes or 3.3% on year.

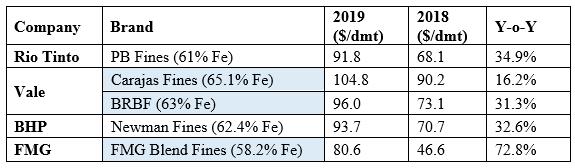

Well, no one had the foresight to know what was going to happen for the rest of 2019, and the theme about possible supply tightness or even shortage saw Mysteel’s SEADEX 62% Fe Australian iron ore fines hit its nearly 5.5-year high of $127.15/dmt CFR Qingdao on July 3, up $54.65/dmt or 75.4% from the end of 2018.

Iron ore price fluctuation of such a degree had not been seen ever since China’s steel industry crawled out of the deep lossmaking hole since 2016, and this had also seriously challenged all the Chinese steel producers on how to run their businesses when steel margins were on the decline.

World’s top four miners’ iron ore output and sales for 2019 (calendar year)

Mainstream iron ore brands in 2019

Mainstream iron ore brands in 2019

When the global iron ore price shot up to above $80/dmt CFR Qingdao and persisted at above the level throughout 2019, as a result, triggered a spree for non-mainstream iron ore suppliers and China’s domestic iron ore miners to join the party, ramping up their supply to China either to fill up the gap left by Vale and the Australian iron ore miners or to compete for some market shares too when margins were so attractive.

China’s Customs data for 2019 did show that China’s iron ore imports from Australia and Brazil dipped by 15.4 million tonnes and 4.7 million tonnes on year respectively, but the volumes from other sources such as India, Ukraine, Russia and Canada grew substantially by 23.2 million tonnes on year.

Written by Victoria Zou, zyongjia@mysteel.com

Edited by Hongmei Li, li.hongmei@mysteel.com