ANALYSIS: Rebar-HRC price spread to remain wide in Apr

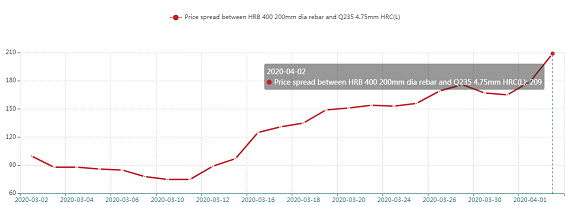

On April 2, the price gap between the HRB 400 20mm dia rebar and Q235 4.75mm HRC two had widened to Yuan 208/tonne ($30/t) with the former being at Yuan 3,578/t, and the latter at Yuan 3,370/t, both including the 13% VAT, according to Mysteel’s daily price tracker, as against the difference of Yuan 100/t on March 2.

Chart 1 Price spread between rebar and HRC

Source: Mysteel data

China’s demand for longs on a steady recovery

The different pace in demand recovery for both long and steel explained why back on March 1-10 the rebar-HRC price spread was as narrow as Yuan 75-100/t, as the downstream industries for both has just commenced the process of resumption after most of the quarantine measures and lockdowns gradually loosened across the country since mid-February.

The long steel market revival, however, has accelerated since mid-March when most of the construction projects especially infrastructure projects have been back online on the strong encouragement of Beijing, and even as of now, China’s steel consumption model remains heavily leaning on long steel especially those for construction.

By March 16, the actual operational rate of 10,449 construction sites under Mysteel’s close tracking recovered to 74.5%.

“Beijing is eager to abate the impact of COVID-19 on the economy as soon as possible, and it is a common practice for the Central government to find a solution in propping up the infrastructure sector,” commented a Beijing-based macro-economy analyst.

Besides, Beijing can’t afford for the national economy to stall for an even longer period in 2020 after a widespread halt in many industrial sectors since late January and for most of February because of the Chinese New Year Holiday and then the COVID-19, and the year itself holds the paramount significance being a year of milestone for China to become a well-off society, Mysteel Global understands.

Under the circumstances, China’s sales volume of long steels comprising rebar, wire rod and bar-in-coil among 237 sampled steel traders across the country totalled 174,588 tonnes/day as of April 1, or up 261% on month, according to Mysteel’s data.

China’s flat steel suffering the blow in domestic sales and exports

China’s auto makers, machinery and home appliances manufacturers, however, have not been able to resume operations as fast, mainly as the retailers’ consumption has stayed largely dormant and spare parts supplies have remained an issue especially for the auto industry, Mysteel Global understands.

“Some of laptop models will not be available to the market for a while, as we have been procuring spare parts globally, and the COVID-19 has disrupted the some of the supplies,” a Beijing-based source from a laptop producer admitted in late March, and it is hard to predict when the supply will return to normal with the explosive growth in the COVID-19 confirmed cases outside China, he added.

China’s auto sales, at the same time, are expected to stay lukewarm for the first quarter, and the sales for the first two months plunged 79.1% on year to 310,000 units, as reported. Chinese auto production in February notably shrank to a mere 285,000 units, plummeting 79.8% on year, according to the data from China Association of Automobile Manufacturers (CAAM).

Besides, as of February, China’s automobile sales had posted year-on-year declines for 20 straight months as of February, and “We expect another batch of negative numbers in the auto sector for March, as few auto makers have been willing to operate at their full capacities amid the gloomy situation and the market will not change much for the better in April,” a Shanghai-based market source said.

As for China’s home appliance industry, all the major products including air conditioners, refrigerators, televisions and washing machines posted plunges in production over January-February.

Table 1 China's white goods output during Jan-Feb

|

Products |

Air conditioners |

Refrigerators |

Washing machines |

Televisions |

|

Output (million units) |

16.29 |

6.67 |

7.76 |

19.7 |

|

Y-o-Y (%) |

-40.2 |

-37.4 |

-20.2 |

-26.6 |

Source: China's National Bureau of Statistics (NBS)

The decline in home appliances consumption had to do with that China’s domestic property market fell into a stagnancy partly because of the COVID-19, as well as that the Chinese citizens, amid economic uncertainties, have been consciously controlling their expenditures on non-essential items such as home appliances or those that are with huge investments and long commitments such as housing.

China’s property sales area slumped 39.9% on year to 84.8 million sq m over January-February, among which that for residential housing fell 39.2% on year, as reported.

Other than the challenging domestic demand for flat steel, the Chinese flats makers felt the squeeze from outside China, as the coronavirus has hit hard some of their export destinations especially ASEAN countries, market sources pointed out, noting that some countries have come to a standstill because of their lockdowns.

China’s flat steel exports account a bigger share than long steel, and in the first two months, China’s total steel exports slumped 27% on year to 7.8 million tonnes, among which flat steel tumbled 26.1% on year to 4.75 million tonnes, as Mysteel Global reported, and China’s steel exports are expected to be consistently challenged as the growing uncertainties in the development of the COVID-19 and therefore in the global economy.

Written by Venus Wang, wangyi@mysteel.com

Edited by Hongmei Li, li.hongmei@mysteel.com