Market: China’s iron ore and steel prices deviation to persist

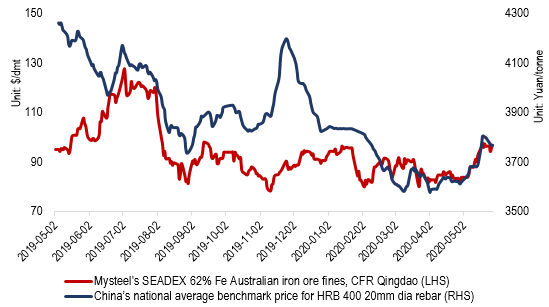

Starting late May, iron ore prices have been strengthening in contrast to the softening in the steel prices, and the phenomenon may last for a while due to the differences in fundamentals and market sentiment, market sources on Thursday.

China’s national price of HRB 400 20mm dia rebar subsided by Yuan 37/tonne to Yuna 3,768/tonne ($529/t) including 13% VAT as of May 28, after having touched a high since February 3 on May 20, while Mysteel’s SEADEX 62% Fe Australian Fines had been ranging $94.1-97.15/dmt CFR Qingdao over the same period, according to Mysteel’s data.

Compared with a year ago, the contrast was even more outstanding, as the rebar price was Yuan 409/t lower while the iron ore pricing index was just $8.85/dmt less.

Source:

Mysteel

Source:

Mysteel

China’s market sources, however, acknowledged this with little surprise at the divergence even though both the commodities are facing uncertainties and iron ore is mainly consumed in China.

“For now, iron ore fundamentals seem slightly better (with the concern on supply) than steel, and this will take a bit of time to correct,” a Shanghai-based analyst commented, pointing out that it is a common understanding that steel inventories at the Chinese steel mills and traders are still running high despite the consistent declines since mid-March, which has kept steel prices under pressure.

Imported iron ore, in contrast, has seen port inventories declined and touch new lows since late 2016, which has naturally lent support to iron ore prices, he highlighted.

An analyst from Southeast China’s Fujian agreed on the prediction that the deviation between iron ore and steel prices will go on some time.

“Recently spot rebar trading volume has shown signs of waning while supply has kept rising, and given that iron ore prices stands chances for resilience, the softening in steel prices will be the means to convince Chinese steel mills to cut down on production in the end to match a slower pace in demand,” he explained.

CISA warns of the divergence in raw materialand steel prices

The divergence, however, was not defined “normal” in the eyes of the China Iron & Steel Association, and its secretary general He Wenbo even shared the phenomenon when interviewed by the Chinese media as a representative of the “Two Sessions” on May 22.

“The pandemic has dampened many steelmaking raw materials prices, while the imported iron ore price has been an exception, holding firmly at around $80-90/dmt, despite that Chinese steel mills have been struggling at the break-even line,” he said.

According to He, the pandemic is estimated to have affected 60 million t/y blast-furnace ironmaking capacity in foreign countries so far and the iron ore consumption, as a result, may reduce by over 30 million tonnes for the second quarter along.

Global iron ore mining companies, nevertheless, have been operating largely as per normal so far, and supply from Australia and Brazil will recover from the seasonal affection in the first quarter, which mean an extra 40-70 million tonnes of iron ore will be shipped to China.

Under the circumstances, He felt that the spot iron ore prices have failed to truly reflect the real fundamentals, but have been strongly influenced by the pricing indices that have referred to derivatives market for directions whenever the physical market is quiet.

Resource investment is the solution for Chinese mills

To get rid of the awkward situation and avoid the repetition of the divergence in iron ore and steel prices, He proposed higher domestic iron ore supply, overseas resource investment and higher scrap utilization.

It will be durable if China’s iron ore supply can fulfill 20% of the domestic steel mills’ needs, and to achieve the target, Beijing will need to cut taxes and feed on Chinese iron ore mining companies to lessen their burden and also to encourage new investments.

As for overseas resources investment, He suggests Chinese steel mills to cooperate with the established iron ore miners in Australia and Brazil in exploiting opportunities as well as looking beyond into resources in Africa and Canada.

Cao Zhiqiang, chairman of Valin Group in Hunan in Central China, shared a similar view on the overseas investment when interviewed by the Chinese media during the “Two Sessions”.

He, however, reminded the Chinese steel mills of the challenges in doing so, such as the lack of related government policies, laws and financial support from the company’s own experience as the current third largest shareholder of Fortescue Metals Group (FMG) with an around 10% company stake, according to FMG’s public sharing.

Besides, Chinese companies are also lacking the related know-hows regarding investment and iron ore mining operations in the foreign countries, he added.

Valin became FMG’s second largest shareholder in 2009, in exchange for steady iron ore supply and investment returns from the Australia’s 170 million tonnes/year iron ore miner.

Both He and Cao mentioned on different occasions the need for Chinese steel mills to increase scrap utilization in steelmaking as a leverage against iron ore, as it is more eco-friendly, a complete substitute, and can be competitive in prices when the supply quantity reaches a certain benchmark.

Written by Victoria Zou, zyongjia@mysteel.com

Edited by Hongmei Li, li.hongmei@mysteel.com