MARKET-1: China’s domestic steel demand to fall in H2

Xu’s remarks aligned with the prediction of the World Steel Association (WSA or worldsteel) that the global steel demand may contract by 6.4% on year to 1.65 billion tonnes, mainly because of the COVID-19 crisis, according to WSA’s latest Short Range Outlook (SRO) released on June 4.

His warning may have spoken out the concern of many in China’s steel market, as many are getting more jittery by the day witnessing the ever-rising steel output in China when the whole world is talking about a global economic recession in 2020 and many agree that the worldwide situation is even worse than the last financial crisis around 2008-2009.

China’s high domestic steel consumption hard to sustain in H2

China’s strong recovery in the domestic steel consumption ever since mid-March after stagnant February has caught many market sources by surprise, and many of them are waiting for the end of powerful rebound to come, though, so far, nothing has happened.

Mysteel’s daily tracking on spot sales of construction steel comprising rebar, wire rod and bar-in-coil among the 237 traders across China confirmed the dreamlike reality with the daily transaction volume averaging 234,572 tonnes/day for April-May, even higher than 206,588 t/d on average a year ago when no threat of the pandemic hung in the air.

April and May are always a golden period for construction steel consumption in China when the weather is pleasant and cooperative for construction projects to progress, but April and May in 2020 had appeared exceptionally good months for China’s steel sales partly as all the deals that had been unable to be inked or fulfilled in the first quarter had been rushed through.

Besides, China’s domestic steel demand especially for long steel products had surged in April and May with Beijing’s reiteration of injecting more funding in national economy especially in the infrastructure construction.

“In the first quarter (this year), China’s steel demand was estimated to have contracted by as much as 20% on year because of the coronavirus,” Xu acknowledged.

For the H2, however, Chinese steel market may not be able to maintain the blooming demand in the domestic market when the global economy is struggling to avoid a too serious contraction, he warned.

WSA confirmed that, unlike the last financial crisis, developing countries have been hit just as hard as the developed economy, and the short-range outlook has not looked into the impact on the trade flow of related steel products, according to Edwin Basson, director general of the association.

A market sources from North China’s Shanxi also highlighted the seasonal factor. “The apparent consumption of rebar in domestic market had already surged to its record high in the past two months, and it will probably not be able to be spared from the dampening by the hot and wet weather in the southern part of the country,” he added.

The regions south of the Yangtze River in China are usually hit by the extremely high temperatures and the great humidity if not heavy rainfalls over June-August, making it almost impossible for outdoor construction projects to continue as per normal out of employees’ health and safety concerns, Mysteel Global understands.

Other than the climate challenges, China’s steel demand from the commercial property projects including both residential housing and non-residential buildings may remain problematic afterwards, according to some market sources.

“It is a big question and equally crucial whether the funding in new property projects will return to positive growths not to mention back to last year’s level,” a Beijing-based ferrous analyst pointed out.

All the uncertainties in the global and Chinese economies have kept many Chinese citizens away from housing purchases either for their own needs or for investments for 2020 in general, though some signs of slow recoveries had emerged since the start of the second quarter thanks to a series of preferential policies by local authorities including granting the local IC or “hukou” in Chinese to welcome the talented personnel, he added.

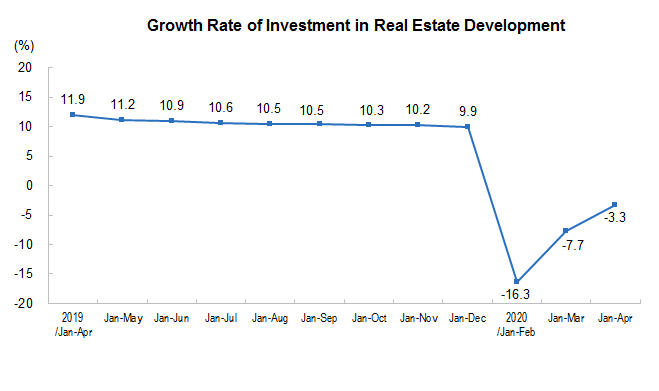

The data from China’s National Bureau of Statistics (NBS) showed obvious recovery in China’s property starting April, as the on-year decline in the investment narrowed to 3.3% on year from the 7.7% drop for the first quarter, and that in newly-launched property projects narrowed 8.8 percentage points from Q1 to 18.4% for January-April.

Chart: Growth rate of investment in China’s real estate development

Source: NBS

Click here for part 2 of the feature