Click here for part 1 of the feature

High

steel output and stocks to persist in H2

The unsolvable

uncertainties in demand will only lead to the rises in finished steel

inventories on the zealous output, which will test the Chinese steel market

resilience in the latter half of 2020, keeping the market participants always

on their toes, Xu pointed out.

“Demand has been

just back to the normality, while production has definitely been at full blast,

and the balance will be the decisive factor for China’s steel price movement,”

a senior official from a steel mill in Northeast China’s Liaoning province

shared the worry.

As of June 4,

the blast furnace capacity utilization among the 247 Chinese steel mills had

surged to 91.9%, having climbed for twelve consecutive weeks or way above the

widely-acknowledged sustainable and healthy 80-85%, according to Mysteel’s

survey.

“This is a

multi-year high and almost at the full capacity in essence,” an official from a

steel mill in East China’s Shandong province commented, admitted that his

mill’s daily finished steel output rose too, reaching 70,000 tonnes/day by the

end of May from 52,000 tonnes/day a month ago.

It is rather

concerning that Chinese steel mills have so far ignored the fact that the

existing finished steel inventories in China are far higher than a year ago

even with the steady declines since mid-March, according to Mysteel’s related

surveys.

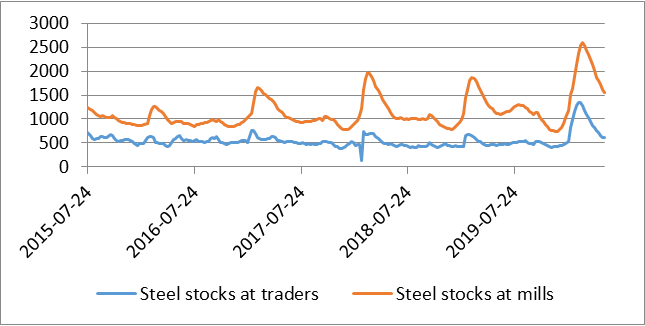

As of June 4, stocks of five major finished steel products including rebar, wire rod, medium plate, hot-rolled coil, cold-rolled coil, in the commercial warehouses in China’s 35 cities were 43.3% higher on year at 14.9 million tonnes, and the volume at the 184 Chinese steel mills totalled 5.7 million tonnes, or 23.6% higher on year even after twelve and 13 consecutive weeks of reduction respectively.

Chart: China’s finished steel stocks at traders and mills

Source: Mysteel Data

Nevertheless, “(rebar and wire rod) output has recently reached their five-year highs, and may well grow further even though sales may come down in the rainy season,” a steel trader from East China’s Shandong province grumbled.

A Singapore-based iron ore trader shared the uneasy feeling too. “I can’t see any definite signs of steel demand increase in the long run even in China, to me it is more like sentiment driven and the make-up after the lost time in the first quarter. I am waiting for the balloon to burst. I feel it is just a matter of time,” she said.

Steel

exports unable to relieve much pressure from high supply in China

For 2020,

Chinese steel market sources are well aware that steel exports may not be a

solution anymore to balance out the fundamentals, just as back in 2015.

China’s earlier

escape from the virus simply because of being hit the first resulted in higher

domestic steel prices than elsewhere in the world,

and the less steel consumption outside China including the core export

destinations such as EU and ASEAN countries because of the pandemic will fail

to help digest much steel supply from China.

Besides, China’s

steel exports have been losing the pricing competitiveness against supplies in

the past many years and they look rather pale against the lower-priced supplies

from India and Turkey, a Shanghai-based trader admitted. By the end of May,

China’s B500B 18-25mm rebar, for example, was offered at $431/t FOB Shanghai

port as against Turkey’s rebar offering at $420/t CFR Hong Kong.

“The country’s

steel exports may decline to 55 million tonnes (this year),” Xu predicted,

which is translated to a 14.5% o-year decline from 64.3 million tonnes for

2019. Over January-May, China’s steel exports dived by 14% on year to just

above 25 million tonnes, according to the Customs data.

On the contrary,

China has been importing more steel products including semi-finished steel and

HRC from outside including India, Xu noted, estimating China’s steel imports to

total 20 million tonnes, or up substantially from last year’s 12.3 million

tonnes.

Steel

price resilience on high production costs a false positive signal

Amid all the

complexities in the fundamentals, the balloon may really take a bit longer to

burst.

The support on

China’s domestic steel prices from the rising steelmaking raw material costs in

H2 may send a false positive signal to the steel market participants in and out

of the country, which may lead to even higher steel output and delay the

unavoidable but with even greater consequences, market sources noted.

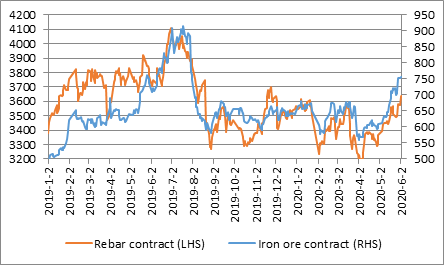

In early June,

the most-traded iron ore contract on Dalian Commodity Exchange (DCE), for

instance, was Yuan 144.5/dmt or 23.7% higher on month, while the most-traded

rebar contract on Shanghai Futures Exchange (SHFE) rose too but by Yuan 242/t

or only 7% on month.

Chinese steel

mills have not made more money but less as the comparison has not included the

rising costs in other steelmaking materials such as scrap, coke and

ferroalloys, Mysteel Global noted.

Chart:

Most-traded rebar and iron ore contract price movements

Source: DCE,

SHFE

Iron ore price,

on the one hand, may not subside soon, as the market has been consistently at

the mercy of speculation after speculation on supplies especially from Vale, as

the world’s largest iron ore miner has yet fully recovered from the dam

collapse in late January 2019 and its operations have also been challenged by

the explosive spread of the COVID-19 in Brazil in 2020.

The

ever-declining imported iron ore inventories at China’s 45 major ports to a new

low since late October 2016 to 107.5 million tonnes as of June 5 also

further fumed the market optimism on higher iron ore prices, even though Vale

has confirmed on a few occasions not

to further

cut its iron ore fines production guidance from 310-330 million tonnes after

the downward adjustment from 340-355 million tonnes in April when the pandemic

impact had already been in consideration.

It has not

helped to cool down the iron ore market much either even though until June 5 Vale had outright admitted more shipment to China

in 2020 because

of the waning demand from those steel mills in Europe and Japan.

“Many traders

are still frantically ordering new shipments recently and at fixed prices,” the

Singapore trader said, admitting that she had been careful with the booking

since the iron ore price exceeded the $100/dmt CFR benchmark on May 29.

Crude steel

output both for the whole world and China, however, will reduce sometime in

2020 if it has not emerged, according to Xu, estimating the global crude steel production

to reduce by 14.6%

on year to 1.58 billion tonnes, among which, China’s

to fall by 4.6% on year to about 950 million tonnes, according to his rather

pessimistic estimation.

“It is only a

matter of time for the market to realize this, and the imported iron ore prices

will then slump,” he commented. This, sooner than later, hopefully will help to

cool down the frenzy in China’s steel market.

Written by Venus

Wang, wangyi@mysteel.com and Olivia Zhang, zhangwd@mysteel.com

Edited by

Hongmei Li, li.hongmei@mysteel.com