FEATURE: COVID-19 testing Asian steel business models

The changes forced onto the Asian steel mills in order to survive the unprecedented situation because of the coronavirus attack could well make 2020 a watershed year in steel trade.

China’s own appetite for steel promotes inner resilience

Recent statistics for China’s steel sector tell an impressive story.

Despite being the world’s largest steel producing country by far, and the first to instigate severe restrictions on movement because of the virus, bringing the world’s second largest economy to a shuddering halt, China’s crude steel output still grew by 1.4% on year to 499 million tonnes over January-June, due to the fact that the country, as usual, is able to consume over 90% of its own finished steel output domestically.

A Hongkong-based macro-economy analyst explained this apparent anomaly simply. “China,” she said, “can very well survive on its own with its complete and comprehensive production-consumption model.” Steel in China, in short, is essentially a closed circle.

“The scale of its economy and its population basically enables internal circulation where steel is concerned. The only element lacking is the availability of raw materials, particularly iron ore, and that is why China has had imported a lot,” she added.

That uptick in crude steel production during H1 translated to a 9.6% on-year rise in China’s iron ore imports to 547 million tonnes, according to China’s Customs figures.

To safeguard the smooth internal circulation of steel, China’s central government has also adopted the right strategy by trying various financial aids packages to prevent its medium- and small-sized enterprises from going bankruptcy, she noted.

“Such enterprises are crucial links in China’s value chain for many industrial sectors including steel production and consumption, and if their operations are normal and stable, this will lead to the coherent functioning of many sectors of the economy,” she maintained.

Wire rod coil, source: World Steel Association Image Gallery

Taiwan’s CSC feeling some pain, but it’s bearable

At the opposite end of this steel sales spectrum is Taiwan whose resilience is not as strong as China’s, and its largest steel mill - China Steel Corporation (CSC) - posted a 1.6% on-year decline in its carbon steel sales in the first half of 2020 to 5.1 million tonnes, mainly because customers both inside and out of the region were hit by the outbreak of COVID-19.

An official at the mill’s Kaoshsiung headquarters, South Taiwan, asserted that the company had not been affected too badly by the weakening of steel demand globally, as nearly 70% of its steel products, as always, were sold locally.

She admitted, though, that the negative impact of the pandemic on the global market cannot be ignored as “many of our customers still need to sell their products in the global market after the processing.”

For most months, CSC’s carbon steel sales to the local market usually account for 68-72% of the total, Mysteel Global notes, and the portion for the first half of 2020 remained within the range at 68%, according the latest CSC releases.

Japan struggling with a one-third steel output cut

In sharp contrast, Japan – whose steel exports account for 40-45% of its total finished steel output – saw crude steel output plummet by 17.4% on year in the H1 2020 to about 42.2 million tonnes, according to the Japan Iron & Steel Federation (JISF) data, as in the past 12 months, its domestic steelmakers have suffered three blows, not just one.

Steel demand has been shrinking since the second half of 2019, as the acceleration in Sino-U.S. trade friction impacted exports of “Made in China” products that incorporated Japan-made components, a JISF official explained.

In October 2019, Japanese consumer spending took a hit when Tokyo raised the national consumption tax to 10% from 8%, he explained, and a few months later in March 2020, the coronavirus delivered the blow.

In the first quarter of 2020, the country’s steel output declined but by just 3.4% on year to 24.1 million tonnes, more because of a lower base number a year ago than the little impact of the COVID-19 impact, the Federation official stressed.

“If there had not been any facility issues among some major domestic mills in Q1 2019, the on-year slump would have been more substantial,” he added.

The country’s steel output during the second quarter of 2020, however, was just about two-thirds of that in the corresponding period of 2019, as the domestic steel mills had promptly trimmed their output to match the pace of the decline in demand from Japan’s rapidly slowing economy.

The severe pull-up in steel sales was not only evident in the domestic market but also in exports, a senior official with a Japanese mill elaborated. As much as 70% of Japan’s flat steel exports are destined for the Japanese-invested companies abroad, with coated sheets shipped directly to the Japanese automakers and home appliances manufacturers (and component makers), and hot-rolled and cold-rolled coils supplied to Japanese mill-invested downstream plants.

Nippon Steel, Japan’s largest integrated steel producer, for example, has 18 distribution centres in the ASEAN countries to supply to the Japanese auto and home appliances manufacturers in the region.

“The blow that COVID-19 is being keenly felt in the economies of almost all the countries, big and small,” a Japanese steel mill official said. “Thus, the Japanese steel mills have been suffering domestically and in overseas markets such as the ASEAN region where the Japanese auto makers such as Toyota are located,” he told Mysteel Global.

“In good times, this is a very good business model, but in the bad times like now, the suffering is massive,” he admitted.

Japan’s crude steel output for the present fiscal ending March 2021 is expected to decline to around 80 million tonnes from the 98.43 million tonnes for the previous fiscal, or down 18.7% on year, according to JISF.

What lesson is COVID-19 teaching steel mills?

After the lengthy and serious suffering, many steel mills will probably rethink their business models, figuring out how to enhance the resilience. Unfortunately, China’s market model cannot be replicated by all the other economies, probably not by Japan or Taiwan, due to the great variation in economic scale, population, infrastructure and business development, and therefore the domestic steel market size.

“When an economy is small in size, globalization or regionalization is the way out whether the country likes it or not,” the Hongkong analyst commented. “This year’s COVID-19 outbreak may prompt many governments and businesses to review their strengths against a crisis and look for areas of improvement, but a complete transformation may not be possible at all,” she observed.

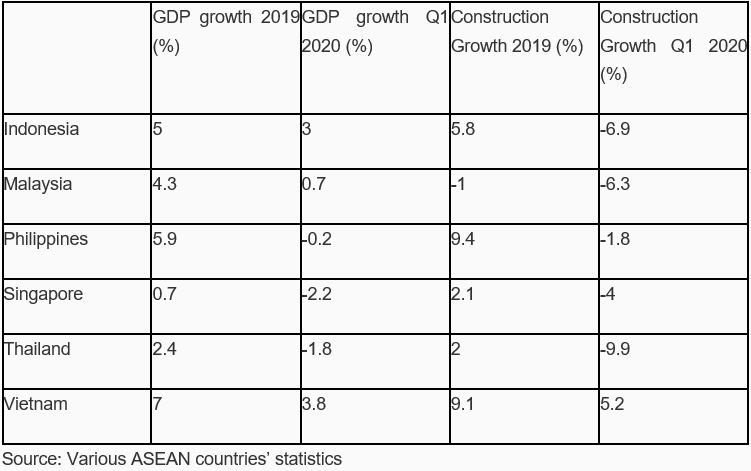

A Singapore-based market source noted that the Japanese steel mills have been exploring spot sales opportunities in Southeast Asia as the ASEAN-6 countries – Singapore, Malaysia, the Philippines, Indonesia, Vietnam and Thailand – are still a promising land for steel consumption of steel with long steel in particular in the years to come.

“This could be an opportunity for the Japanese steel mills to diversify their steel sales away from relying primarily on the Japanese manufacturers in and out of Japan,” he added.

Yet for the Japanese at least, old ways die hard, he admitted, as this has been a business models that have been operating rather well for decades, and “changes are hard in Japan as it is more about the mindset”, he pointed out.

Yet for the Japanese at least, old ways die hard, he admitted, as this has been a business models that have been operating rather well for decades, and “changes are hard in Japan as it is more about the mindset”, he pointed out.

Mexico, now hosting over 600 Japanese-invested auto-related companies, has become a new hub for the Japanese auto-manufacturers supplying the North American market, and the major Japanese mills are again rushing to set up plants there.

In March, JFE Steel and the U.S. steel manufacturer Nucor commissioned a 400,000 tonnes/year auto sheet joint venture in Silao, Guanajuato in central Mexico with the Japanese investor to supply some of the substrate from Japan to the Mexican plant.

Written by Hongmei Li, li.hongmei@mysteel.com

Edited by Russ McCulloch, russ.mcculloch@mysteel.com