MYSTEEL: China’s Aug construction steel may still shine

For August, Mysteel estimated China’s weeklydomestic steel demand at 10.5-10.8 million tonnes nationwide, or 1.2% higher on month and up 1% on year.

“The impact of the flooding will recede gradually in August, (and) construction after the natural disasters will be back on track,” the report stated, adding, “construction sites will accelerate the pace to make up for the lost time in July and more new projects will be launched, both to drive up the demand for construction steel.”

Better demand on month, thus, will be the core driving force for the recovery in the domestic steel prices, instead of the persistently high raw material prices that had lent support to the domestic steel prices over June-July, it said.

As of July 30, China’s HRB400 20mm dia rebar price, stood at Yuan 3,801/tonne ($543/t) including the 13% VAT, up Yuan 45/t on month, but still Yuan 226/t lower than a year ago.

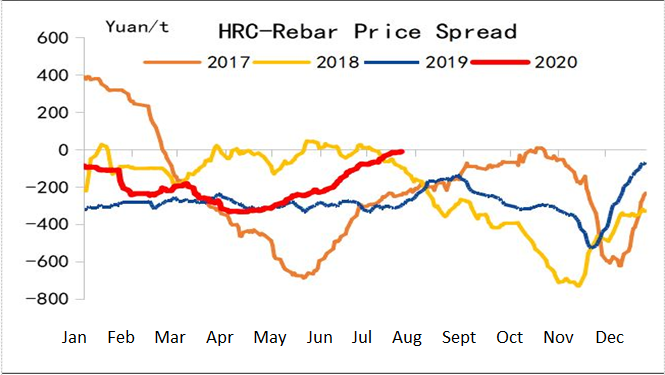

For July, China’s flat steel prices held better than long steel with less affection by the adverse weather, and HRC price finally exceeded that of rebar, with HRC having been enjoying the highest margin at Yuan 212/t against the Yuan 191/t margin for rebar.

China’s HRC-rebar price spread over 2017-2020, source: Mysteel

Hot summer days in August may detain the progress to some extent as the high temperatures may limit the hours for outdoor construction, Mysteel acknowledged, but the slow-down will not be as profound as the drag by the rains and floods in June and July, it elaborated.

In August, thus, infrastructure and property construction will be backbone of the demand for long steel products, Mysteel pointed out.

China’s fixed asset investment in the infrastructure had been recovering steadily, and the funding in infrastructure construction projects declined 2.7% on year for the first half, or narrower than the 6.3% on-year drop for the first five months, according to the official data, Mysteel Global noted.

In June alone, the investment in the infrastructure grew 6.8% on year, though the rate was 1.5 percentage points lower than the on-year rise in May because of the widespread rainfalls over June and by late July.

August will the be end of the rainy season, and Beijing disclosed on July 13 to launch 150 hydro projects at a total investment of Yuan 1.29 trillion over (2020-2022) including dams, reservoirs, irrigation and water supply, water preservation and ecological protection.

As for the country’s property market, it has shown great resilience and will continue to be a main driver for steel consumption in August when the rainfalls stops, Mysteel highlighted. The newly-launched property projects in June grew faster in size than in May even in the middle of the wet season, and “with the notable recovery in China’s property sales, the on-year decline in newly-launched property projects will narrow further,” the report shared.

In H1, the newly-launched property projects fell 7.6% on year to 975.4 million sq m, or less dramatic than the 12.8% on-year drop over January-May, as reported.

Last month, the weekly consumption of the five major steel products - namely rebar, wire rod, hot-rolled coil, cold-rolled coil and plate - fell 6% on month to 10.52 million tonnes, with the declines concentrated on construction steel, with rebar down 10.1% on month and wire rod down 7.4% on month.

As for flat steel, the auto industry, a major consumer, is expected to recover sustainably and steadily in the third quarter, as shown in the auto production and sales that posted gains of 22.7% and 11.8% on year in June, while the consumption by the white and yellow goods manufacturers may be comparatively weaker in August because of the sullen demand for such products, Mysteel shared.

Written by Olivia Zhang, zhangwd@mysteel.com

Edited by Hongmei Li, li.hongmei@mysteel.com