Covid Resurgence Shocked China's Q2 Economy, Infra Construction will Bolster H2 Oil Product Demand

China's Q2 GDP was Dragged by Consumption, Real Estate and Transportation Sector

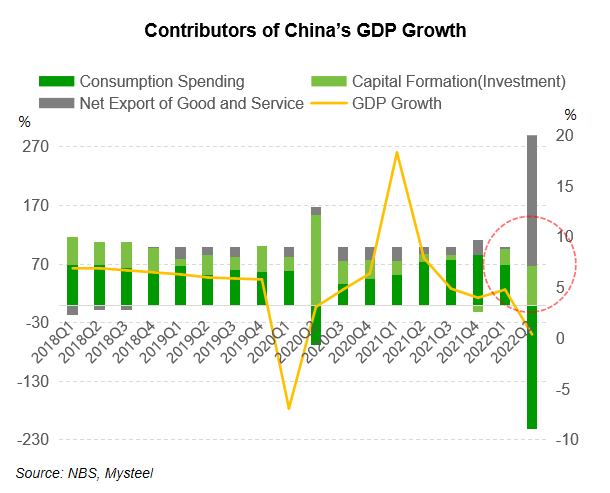

China secured its positive growth in Q2 by 0.4% YoY – the lowest quarterly growth rate since the initial shock of Covid-19 in Q1 2020 – sending the growth of the first half of 2022 to 2.5% YoY, well below the target of 5.5% set by Chinese government in early March.

Net exports accounted for 244.8% of the total economic growth, offsetting the 211.2% negative contribution of consumer spending.

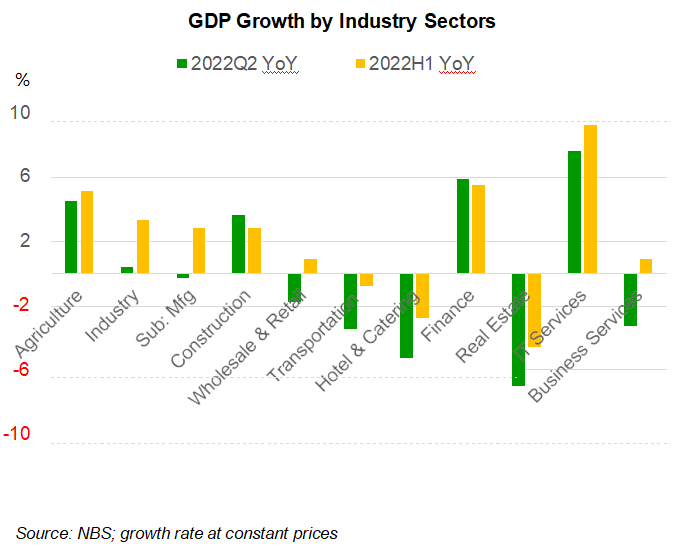

The real estate sector saw the largest decline in Q2 GDP by -7% YoY compared with other sectors. According to the preliminary GDP figure (at current prices), real estate sector accounted for 6% of GDP in the second quarter of 2022, down by 1 percentage point from the same period last year.

The manufacturing sector, which contributed the largest absolute volume, saw a 0.3% YoY decline in GDP in Q2. Accommodation, catering, transportation, and wholesale/retail sectors fell by 5.3%, 3.5%, and 1.8% YoY in Q2, respectively.

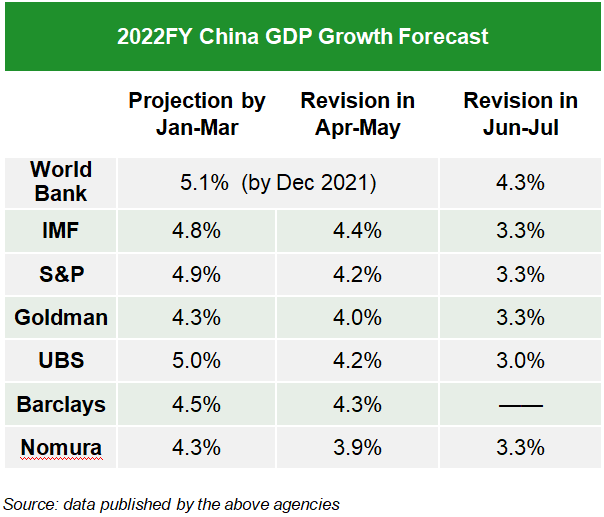

Major investment banks have repeatedly cut their full-year China GDP targets to around 3.3% due to the impact of Covid controls.

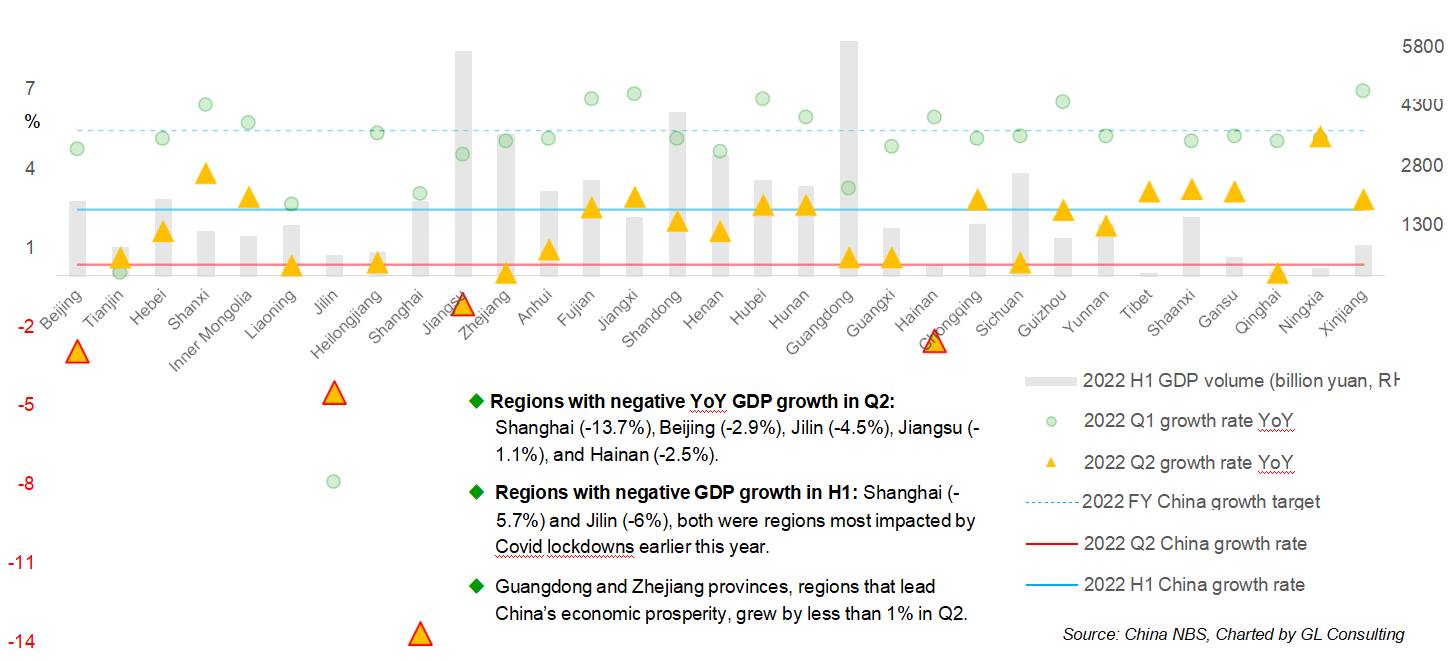

Five Provincial Regions Recorded Shrunk Economy in 2022 Q2

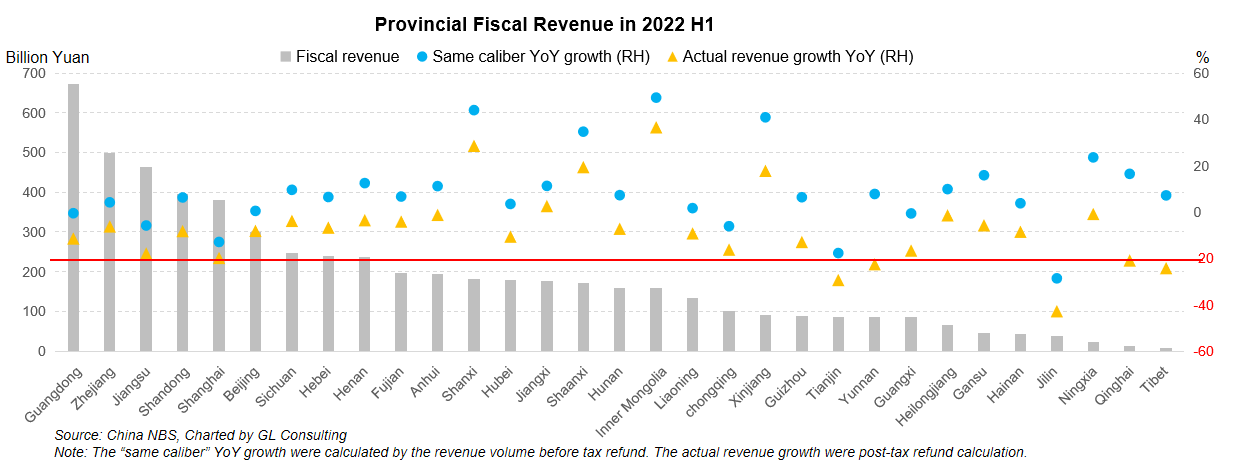

Fiscal Revenue Declined due to Tax Refund Policy

In the first half of 2022, China's national fiscal revenue recorded 5.76 trillion yuan in the first half of 2022, increased by 4.7% YoY – but if fell by 7.9% YoY when considering the tax refund policy this year to bolster economic activity. The total tax rebates budget this year is about 1.64 trillion yuan, and the State Council requires the refunds to be completed by the end of June.

Fiscal revenue of Shanghai and Jilin, which were severely shocked by Covid lockdowns, fell by 12.9% and 28.6% YoY in H1 respectively before tax rebates. Guangdong, Zhejiang, Jiangsu, and Shandong, where fiscal revenue volume ranked top, recorded -0.5%, 4.2%, -5.8%, and 6.3% in growth rate respectively before tax rebates.

Only Shanxi, Inner Mongolia, Shaanxi, Jiangxi, and Xinjiang provinces have increased their fiscal revenue after tax rebates, which are mineral resource-rich provinces producing coal and rare earth.

June Industrial Output Made a Faster Recovery

China's June industrial output gained by 3.9% YoY, the growth was 3.2pp wider than that of May. Among these, the manufacturing sector recovered to a 3.4% growth YoY in June, 3.3pp higher compared with May. Industrial output of automobile sector rose 16.2% YoY, a marked recovery from a 7% YoY decline in May.

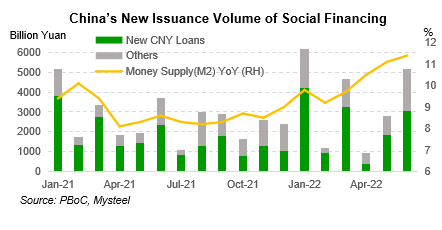

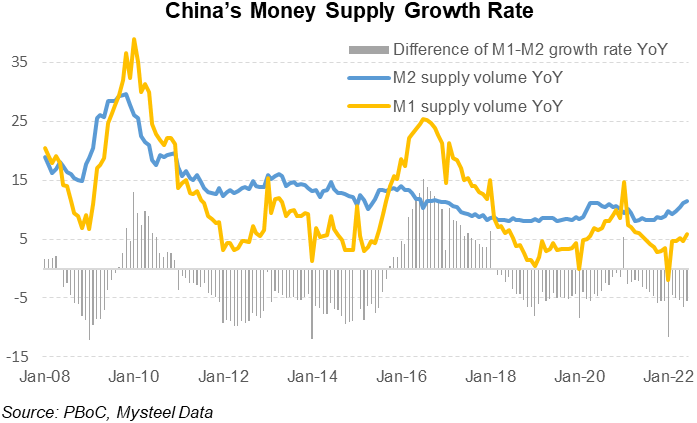

Volume of new issuance of social financing in June increased 85.3% from April, or up by 39.7% from the same month last year. Among these, new CNY loan issuance increased 68% compared with May level. China's money supply (M2) growth rate regains a rising curve following March 2020 to December 2021 period. The difference between M1 and M2 is becoming wider downward, indicating producers' confidence remains weak while the property market stays at a low ebb.

June Manufacturing PMI and Logistics Delivery Resume Expansion

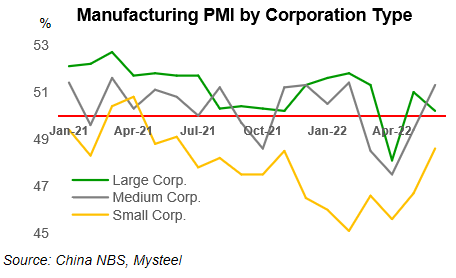

China's official manufacturing PMI recorded 50.2% in June, up by 0.6 percentage points from May, returning to the expansion range. The reading below 50% represents a contraction month on month.

Among the sub-indexes that make up the manufacturing PMI, the supplier delivery time index resumed above 50%, following contraction readings for 15 straight months (since March 2021), indicating logistic conditions of raw material suppliers keep picking up.

The two most weighted sub-indexes –production and new

orders – recovered by 3.1 and 2.2 percentage points to 52.8% and 50.4%, respectively compared with May, indicating a recovery of market demand. Both resume to expansion range.

The manufacturing PMI for the category of large corporations curb 0.8 percentage points from May to 50.2%. PMI of medium corporations rebounded by 1.9 percentage points to 51.3% in June. Small corporations recorded 48.6% with an increase of 1.9 percent point from May, although it remained below 50% for the 14th consecutive month.

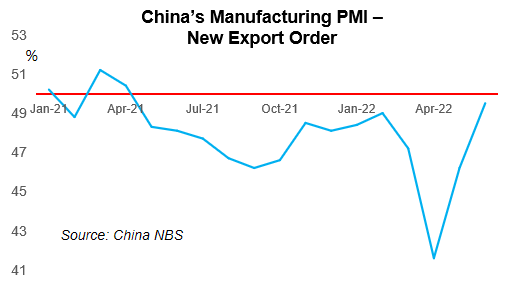

New Export Order Index Remained In the Contraction Range

China's industrial exports expanded its YoY growth to 15.1% in June, 4 percentage points faster than that of May.

New export order index relevant to the manufacturing PMI in June rebounded by 3,3 percentage points on the month to 49.5%, staying in the contraction range for the 14th consecutive month.

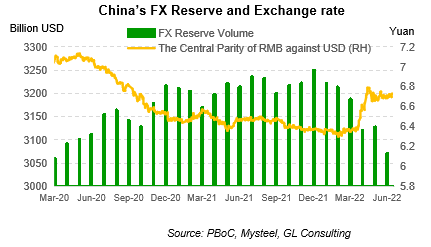

CNY keeps at a low level since the end of 2020 against USD. Due to weaker exports and foreign direct investment (FDI), along with soaring prices of imported commodities from the beginning of this year, China's FX reserves have shown a downward trend.

Oil Product Price Factors Accounted for More Than Half of the CPI Increase

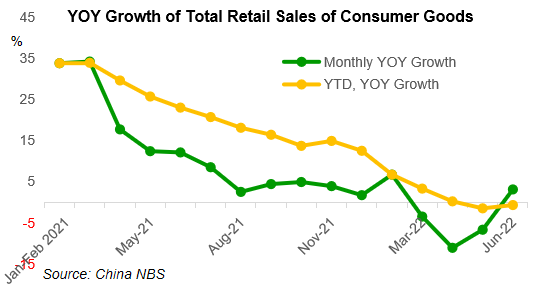

The total retail sales of consumer goods in June increased by 3.1% YoY. Among these, retail sales of automobile increased by 13.9% YoY, while other retail sales of consumer goods increased by just 1.8%. Catering category fell by 4%.

Total retail sales of consumer goods fell by 0.7% YoY in January-June period, the decline narrowed by 0.8 percentage points compared with January-May, but it still did not turn positive growth.

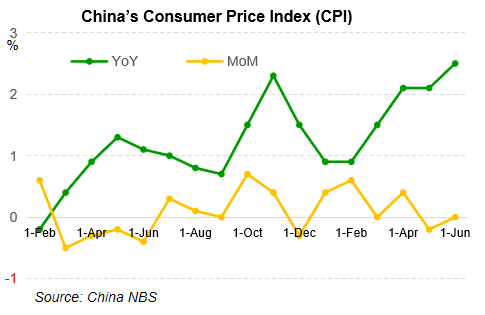

China's June CPI rose by 2.5% YoY, 0.4 percentage points wider than that in May. Among all categories, non-food categories accounted for 80% of the June CPI increase. Gasoline and diesel price increased by 33.4% and 36.3% YoY respectively in June.

China's CPI in H1 rose by 1.7% YoY, which rose by 2.3% in Q2. Impacted by soaring energy prices, gasoline, diesel, and LPG prices increased by 26.7%, 29.2%, and 23.9% YoY respectively, accounting for 53% of the total CPI increase in H1.

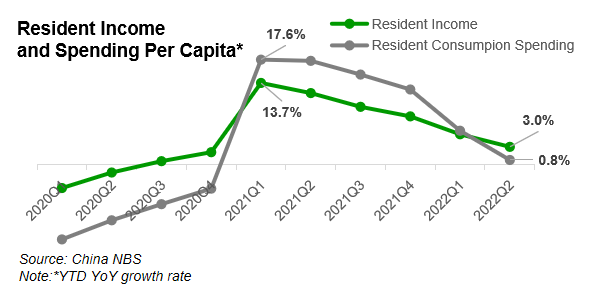

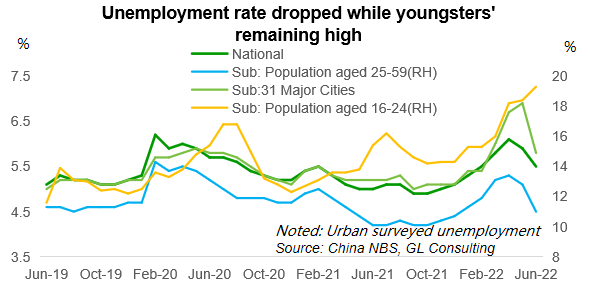

Young Unemployment Keeps in Record High, while Resident Income Growth Fell

The unemployment rate in urban surveys edged down for two straight months to 5.5% in June. Meanwhile, the rate of young people (aged 16- 24) continued to hit another record high in June, reaching 19.3%. The employment pressure increased further during the graduation season in June-July. The rate in 31 major cities was 5.8% in June, down by 1.1 percentage points from May.

The growth rate of YTD residential income and consumption spending per capita fell to 3% and 0.8% YoY in Q2, recording 2.1 and 4.9 percentage points lower than that in Q1. The growth has declined for five straight quarters.

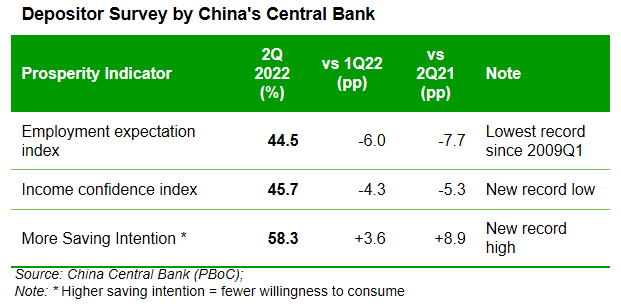

According to depositor surveys by China's central bank, the income confidence index fell by 4.3 percentage points on quarter to 45.7% in Q2. Index of "more saving intention" rose by 3.6 percent point in Q2 to 58.3%.

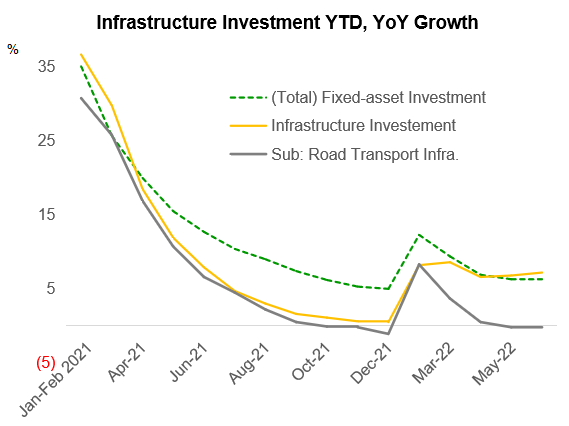

Infrastructure Investment Expanded while Property Market in Deeper Depression

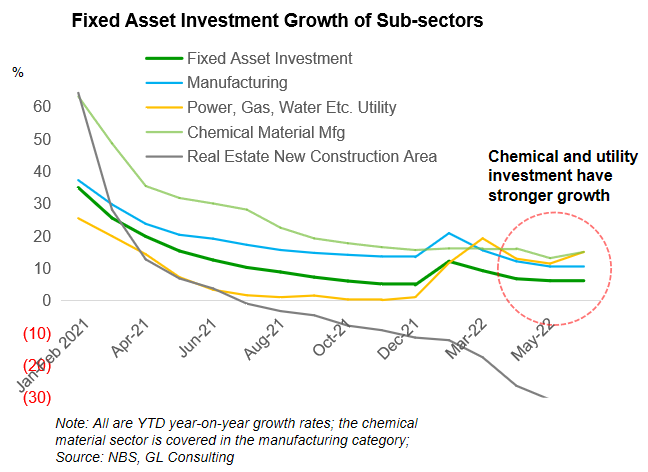

The June YTD growth rate of fixed-asset investment increased by 6.1%, and the rate narrowed by 0.1 percent point from January-May. Among these, infrastructure investment over the period increased by 7.1% with a higher rate than the overall investment. Driven by accelerating special bond issuance, infrastructure investment saw a wider growth up by 0.4 percent point compared with a month earlier.More investment is being invested in information, water, and urban facility infrastructure, as the information infra investment increased by 20.6% YoY, while water and public infra increased by 10.9% YoY in H1. Transportation sector saw weaker, as the road and railway infra investment decreased by 0.2% and 4.4% YoY respectively over the period.

Regarding manufacturing sectors, utility (incl. energy, power, and water projects) and petrochemical investments both recorded an increase of 15.1% YoY in H1, higher than overall fixed-asset investment (6.1%) and overall manufacturing sector (10.4%), while growth rates expanded by 3.6 and 1.9 percent points compared with January-May.

Property market keeps hindering construction demand, as the sector accounts for about 1/5 - 1/4 of China's total fixed-asset investment. Investment in real estate in H1 fell by 5.4% YoY, 2.2 percent points worse than the 4% decline in January-May.

Funds ready for real estate development fell by 15.5% YoY in H1, while the decline keeps diving this year. Area of new housing construction fell by 34.4% YoY in H1 (fell by 45% YoY in June), and the decline continued to expand by 3.8 percentage points compared with January-May. Due to cash flow shortages, some pre-sale housing was knocked off in many cities in China, sending a batch of homeowners claiming to suspend mortgage payments in July. Market sources are expecting the government to set up a national-level bailout fund to resolve current risks.

Infrastructure Investment Expanded while Property Market in Deeper Depression

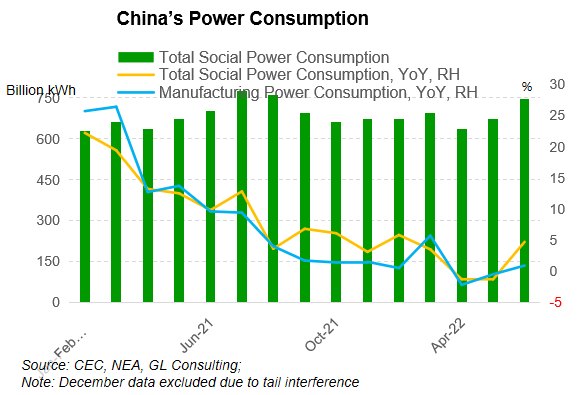

June Industrial Power Consumption Resume YoY Growth

China's total social power consumption picked up by 4.7% YoY in June, or an increase of 10.9% compared with May. Power consumed by the industrial and manufacturing sectors resume growth in June, increaseing by 0.8% and 0.9% YoY, respectively, following declines in April and May.

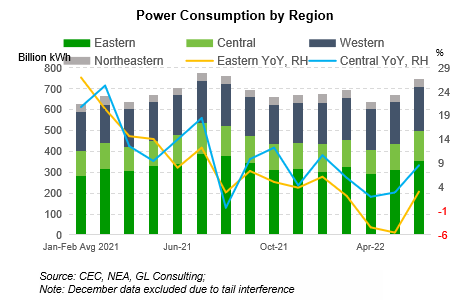

Power used in eastern China resumed growth of 3.1% YoY in June, or rebounded by 13% compared with May. Power used in the central and western regions saw wider increases by 8.6% and 5.6% YoY in June, respectively, while the growth was 5.7 and 2.2 percentage points wider than that in May, reflecting a stronger economic resilience.

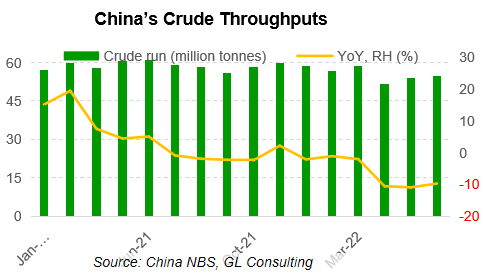

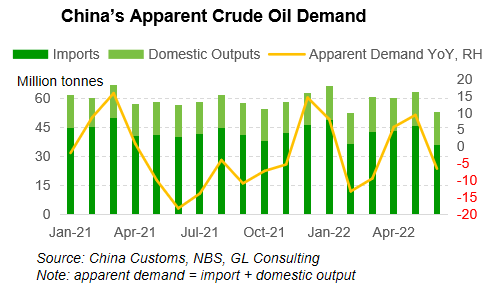

June Crude Imports Recorded a Four-year Low

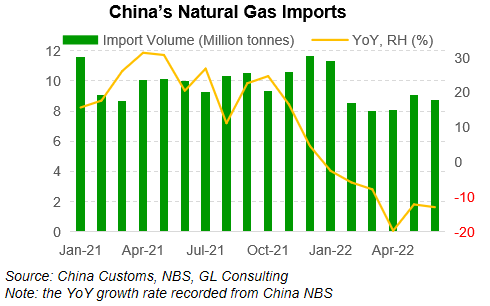

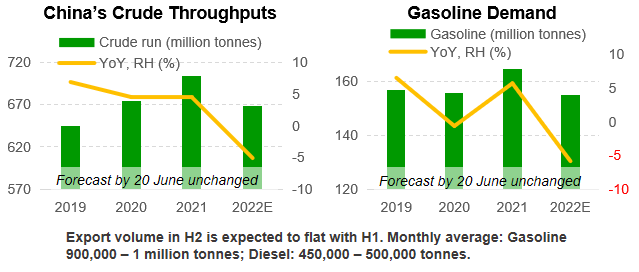

China's crude oil, natural gas imports, and crude throughputs were significantly lower than in the same period last year, given soaring global oil and gas prices as well as the shrinking demand for gas and oil products from industrial and transport users amid frequent domestic Covid resurgences.

Crude oil imports in June were 35.82 million tonnes, down by 10.7% YoY, or 19% decline from daily-averaged imports in May, recording the lowest level since July 2018. Crude throughputs in June were 54.94 million tonnes, down by 9.7% YoY, and the decline narrowed by 1.2 percentage points from May.

China's natural gas imports fell for six consecutive months, recording 8.718 million tonnes with a YoY decline of 12.9% in June. The drop expanded by 0.8 percentage points compared with May.

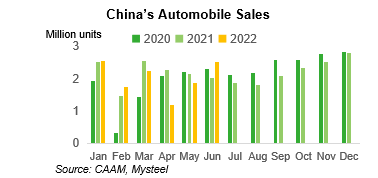

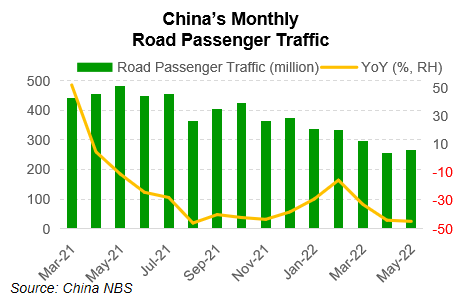

Automobile Sales Continued to Rebound, while Truck Freight Activity Impacted by Floods

Automobile output and sales keep rising:China's June automobile output was totaling 2.499 million units, increased by 28.2% YoY. Automobile sales volume was 2.502 million units, up by 23.8% YoY. It is boosted by resumed production activity from Covid lockdown in April-May, as well as halving purchase tax policy.

The incentive of passenger traveling keeps undermined by strict zero-Covid policy:the number of road passengers fell for 12 consecutive months, with a decline of 44.7% YoY in May.

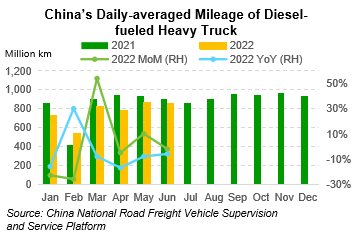

Diesel demand is still weak:many provinces in China were affected by the flood seasonin June, sending logistic fuel demand lower than the same period last year.

- Daily-averaged operating mileage of heavy trucks:-2% MoMin June compared with May, -6% YoY.

- Truck freight traffic index:+8% MoM in June compared with May, -20% YoY.

- China's Logistics Prosperity Index (LPI): 52.1% in June, +2.8 percentage points MoM.

- China road freight index provided by G7 recorded around 102 in the first three weeks of July, compared with the average of 101.6 in June, despite a 17.7% YoY decline with the downward trend compared with 2021 unchanged.

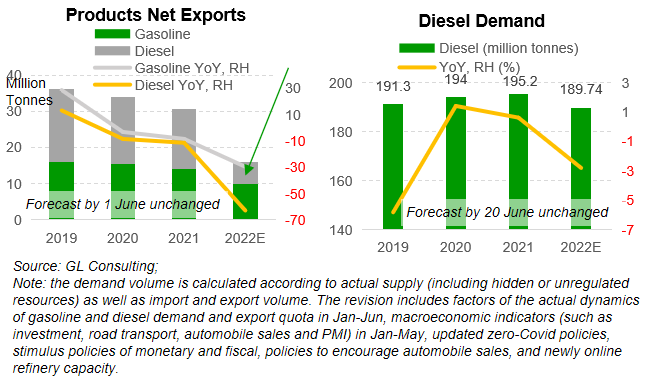

Oil Product Demand Slipped in H1 2022 while Gasoline Fell Deeper

Oil product demand fell in H1, due to factors such as Covid lockdown, slower economic growth, high crude oil prices, and EV alternatives. Gasoline demand saw a more obvious decrease, while diesel demand was relatively resilient with stronger market activity in north China.

It is expected that oil product consumption will resume growth in H2 compared with H1. The dynamic of the zero-Covid policy will remain the major uncertainty of oil product demand.

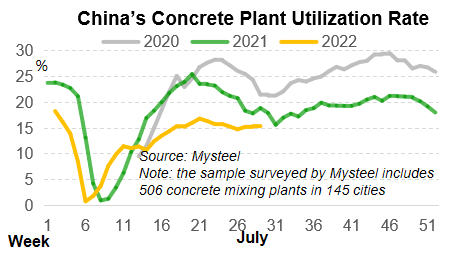

Demand for concrete, an indicator to reflect actual construction workload, has not yet resumed to 2021 levels. The relevant oil demand from infrastructure construction sites in H2 is expected to recover faster after issuance of 3 trillion yuan of new local special bonds in H1 and the 800 billion yuan of new infrastructure credit offered by policy banks, although it is far from offsetting the gap left by continuous recession of real estate market demand.

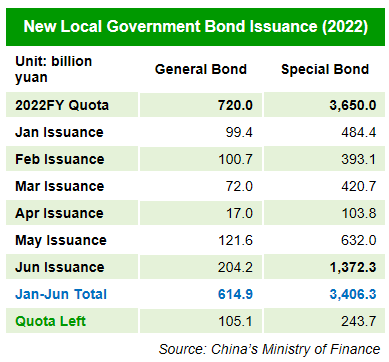

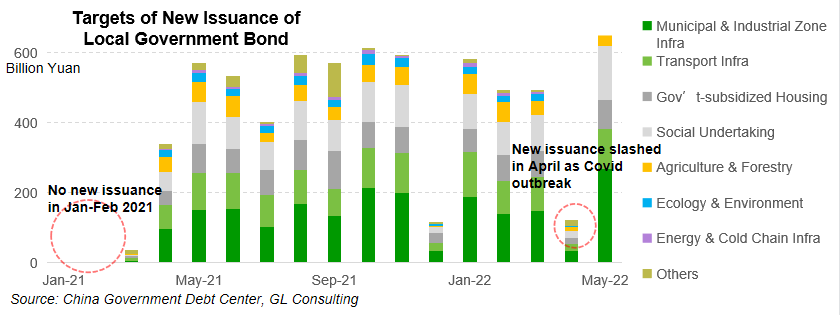

Appendix: June Local Bond Issuance Volume in Record High

New local government bond issuance reached a record high of 1.57 trillion yuan in June. Among them, special bond issuance was 1.37 trillion yuan in a single month, accounting for nearly 40% of the total issuance quota approved by the Ministry of Finance for 2022.

The State Council issued a package of 33 policies for stabilizing the economy at the end of May, calling for local governments to issue and spend the 3.45 trillion yuan of special bond quota before 30 June and 31 August, respectively. The special bond targets at leveraging investment in nine categories including municipal and transportation infrastructure, energy projects, and government-subsidized housing. (More details on analysis of 33 policies package refers to June Issue of "China Policy Perspective".)

There were 31.6% and 18.8% of newly issued special bonds in Jan-May, respectively, targeted municipal & industrial park construction, and transportation infrastructure. Meanwhile, uncertain factors might appear along actual progresses of infrastructure construction – such as the effectiveness of local funding, weather condition, and cash flow of supply chains, sending the cycle length longer from local bond issuance to physical workload.

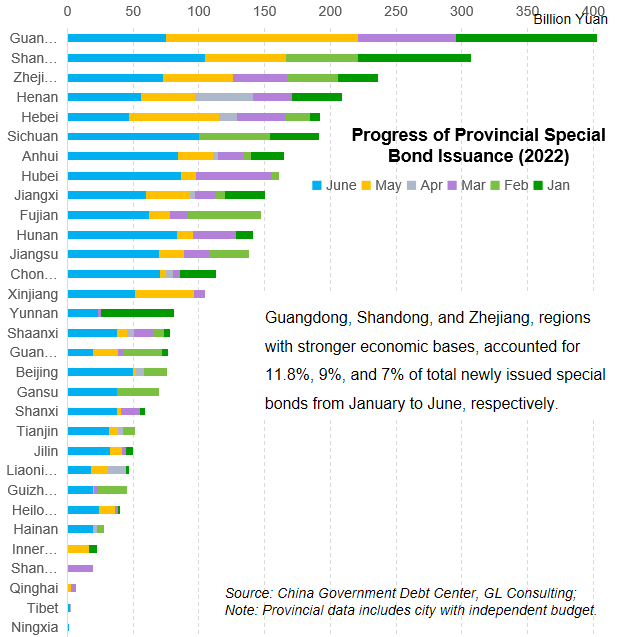

Appendix: 2022 H1 Provincial Special Bond Issuance Volume

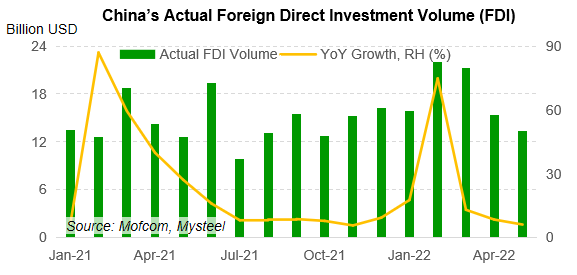

Appendix: FDI Continued a Decline Trend on Month

Appendix: FDI Continued a Decline Trend on Month

China's FDI volume (actual inflow of foreign capital) totaled 564.2 billion yuan, an increase of 17.3% YoY. FDI volume in May increased by 6% YoY, while declining by 13.5% compared with April.

Written by the GL Consulting team (Mysteel's consultancy arm on energy transition):

Edited by Nickey Fu: nickeyfu@mysteel.com