Master Plan Issued for Industrial Sector’s Peak Emission Action

"The Plan" specifies emission targets for industrial sectors: by 2025, the energy intensity of industrial value-added reduce by 13.5% compared with 2020 basis – in line with the goal in the 30-60 Emission Target master plan and the 14th Five-year Plan (2021-2025). It also proposes a goal to cut emissions intensity deeper than society's average level, but no specific number was given. The wording reflects the challenges of low-carbon transition amid current economic downward pressure while reserving more flexibility.

The industrial and energy fields are expected to issue separate and detailed implementation plans, following the master plans of each sector, including steel, petrochemical, non-ferrous metals, building materials, power, oil, and gas industries.

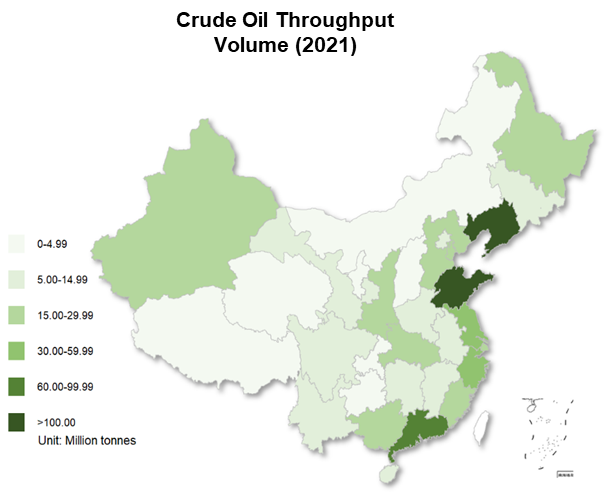

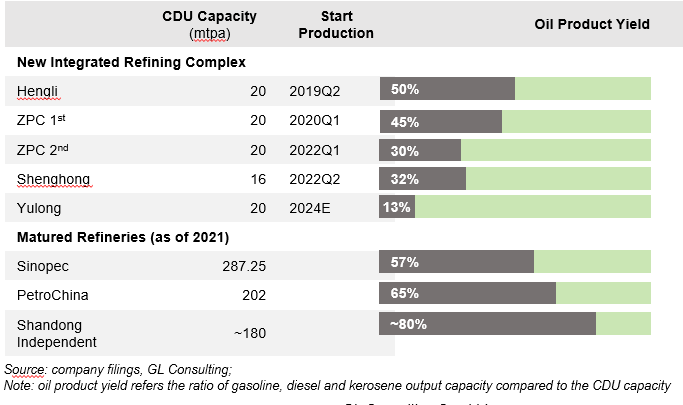

For the petrochemical sector, "The Plan" for the first time set a specific cap on oil product yield, requiring newly approved refining complexes to cut the yield below 40%.

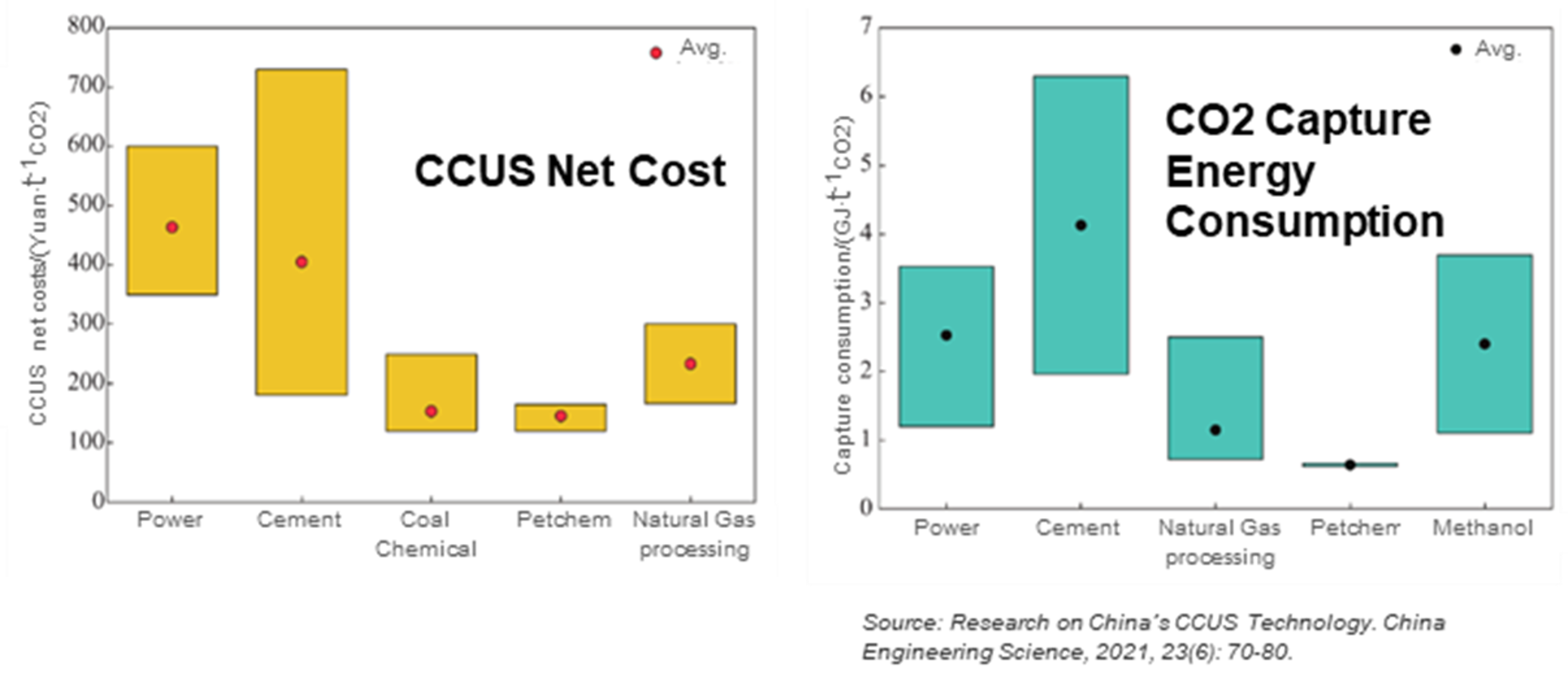

"The Plan" similarly calls for CCUS breakthroughs in the petrochemical, steel and cement sectors. The "Supportive Implementation Plan for Technology Innovation of Peak Emissions and Carbon Neutrality (2022-2030)" issued in August proposes to cut 20% of energy consumption in carbon capturing processes by 2025, compared with 2020 basis, then decrease by 30% in 2030. It's the first time to have a quantitative goal for CCUS development.

"Implementation Plan for Peak Emissions in Industrial Sectors" ("The Plan") is a core component of China's 30-60 Emission Target 1+N Policy Framework, and it is also the master plan for industrial sectors.

"The Plan" specifies emission targets for industrial sectors: by 2025, energy intensity (consumption per unit) of industrial value-added should be reduced by 13.5% compared with 2020 basis; and cut carbon emissions per unit of industrial value-added deeper than the level of the whole society, while the intensity of carbon emission in key industries drops significantly.

- The target of "energy consumption per unit of industrial value-added" is consistent with the goal of "reducing energy consumption per unit of GDP in the 30-60 Emission Target master plan and the 14th Five-year Plan (2021-2025), both by 13.5%. Industrial added value is one of the constituent dimensions of China's GDP accounting.

- The carbon reduction target only proposes a "deeper than whole society level", and no specific number was given. The wording reflects the challenges of low-carbon transition amid current economic downward pressure while reserving more flexibility. Apparently, the peak emissions and carbon neutrality goals require industrial sectors to undertake more than the average level.

- According to the outlines of the 30-60 Emission Target 1+N Policy Framework, the industrial and energy fields are expected to issue separate and detailed implementation plans, following the master plans of each sector, including steel, petrochemical, non-ferrous metals, building materials, power, oil, and gas industries.

The "Plan" once again reflects the importance of leveraging low-carbon transitions from the energy-consuming side, as industrial sectors are the largest energy end-users in China. It is a key pivot for the energy-consuming side to activate their initiatives to change energy portfolio structure. China has been long focusing more on energy supply-side emission reduction, but the current policy framework pays more effort to strengthen motivation to cut emissions from the user-side – by binding targets and economic incentives – to use cleaner energy, lower-carbon materials, and reduce high-emission products.

(Refer to "China Policy Perspective" Feb. 2022 Issue "The 30-60 Emission Targets Seen More Actions to Enrich the "1+N" Policy Framework")

Following the industrial park layouts, "The Plan" proposes another transition direction for industrial production layout:

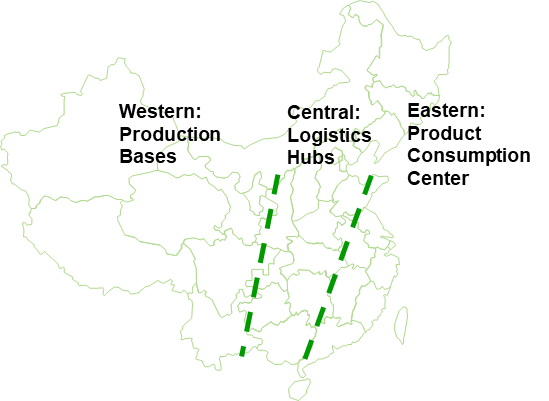

- Petrochemical: A "East-Central-Western" industry positioning

- Steel and smelting: transfer production capacities to areas with rich renewable energy resources, and environmental carrying capacity

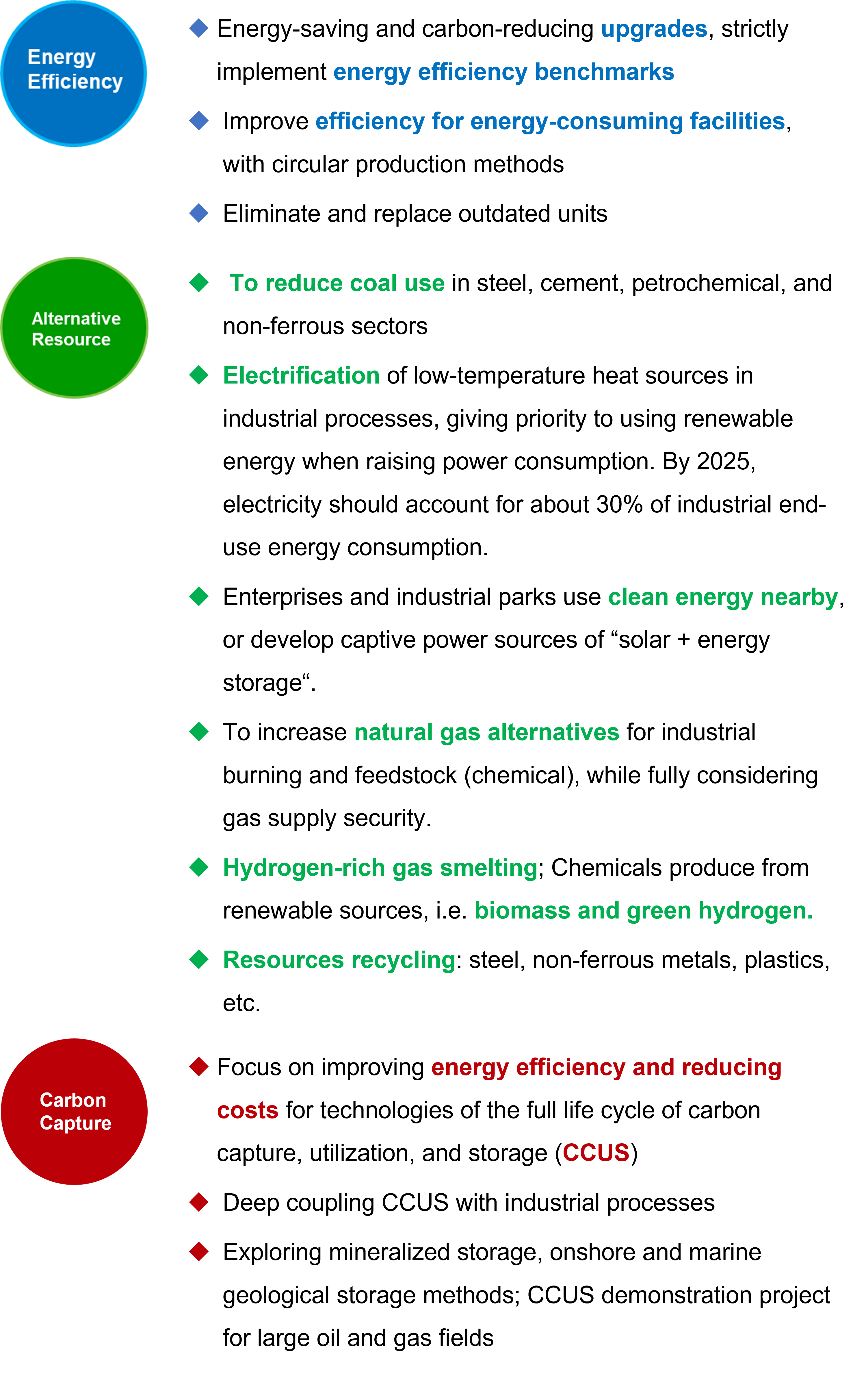

Key Tasks for Industrial Carbon Reduction: Energy Efficiency, Alternative Resources, and Carbon Capture

(Refer to CCUS topic in "China Policy Perspective" March 2022 Issue)

For the first time, the national-level policy proposed a quantitative goal for CCUS development;

Another main component of the 30-60 Emissions Target "1+N" policy framework – "Supportive Implementation Plan for Technology Innovation of Peak Emissions and Carbon Neutrality (2022-2030)" proposes to cut 20% of energy consumption in carbon capturing processes by 2025, compared with 2020 basis, then decrease by 30% in 2030.

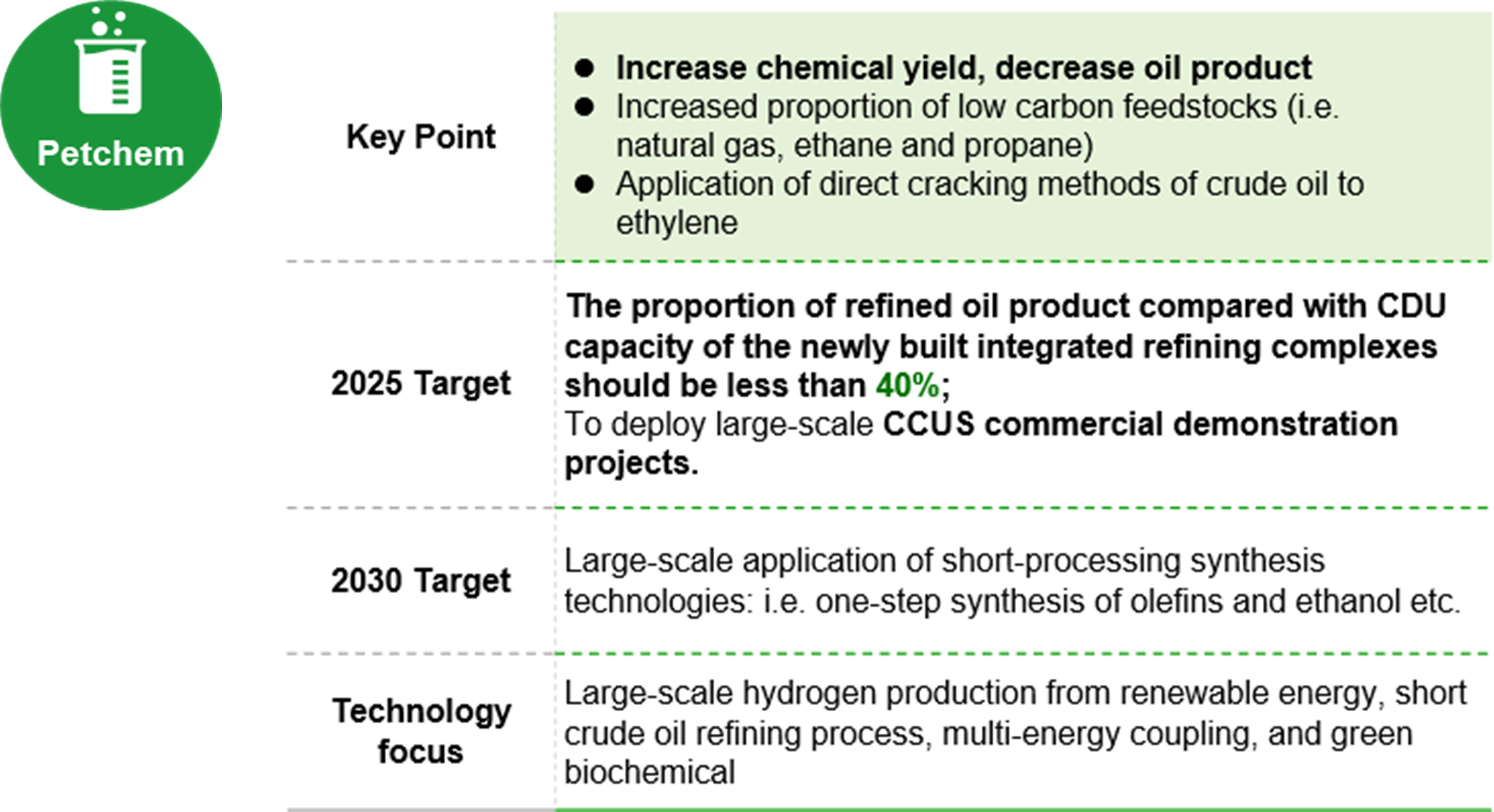

Petrochemical: Specific Cap on Oil Product Yield for the First Time

"The Plan" freshly initiated a specific target to cap the oil product yield of newly approved refining complexes by 40%, a significant decline from China's majority of matured refineries.

New refining complexes commenced in recent years have already curbed down oil product yields due to their downstream demand for chemical products.

NOC refineries also actively transform their refining yield to more chemical products, responding to the trend of peak oil consumption.

(Refer to analysis in "Chinese NOCs To Double Petrochemical Project Investment" from "China Policy Perspective" April 2022 Issue. )

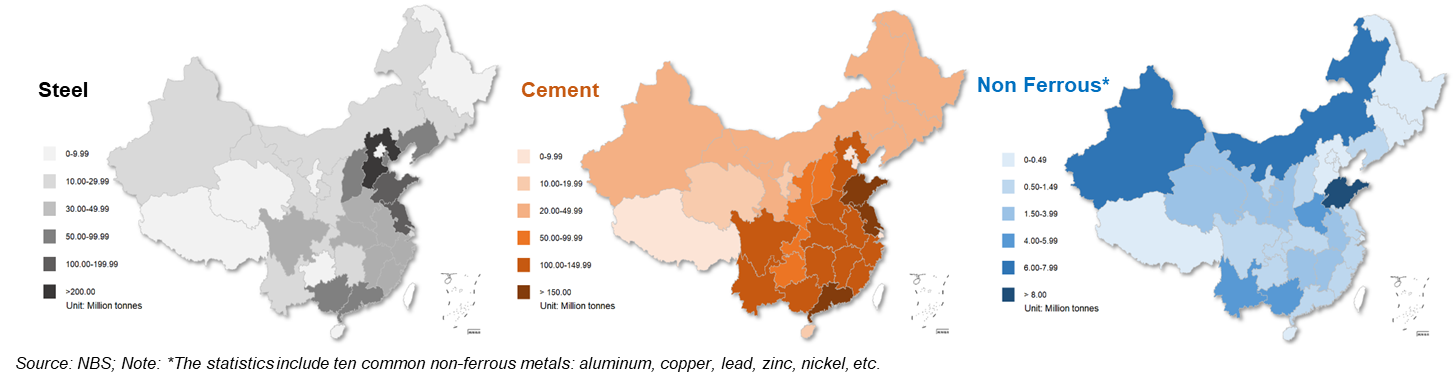

Steel, Tignum and Non-ferrous Industries: Capacity Replacement and Fuel Alternative

Written by the GL Consulting team (Mysteel's consultancy arm on energy transition):

Edited by Nickey Fu: nickeyfu@mysteel.com