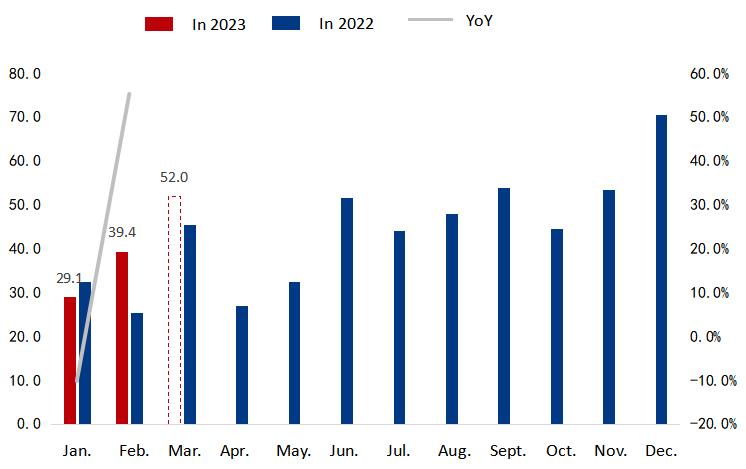

According to the compulsory traffic insurance registration data, China saw 394,000 new energy passenger vehicles insured in February this year, up by a large 55.28% year on year mainly due to a low base last year when the 2022 Chinese New Year holiday fell in February. Negating the impact of the Chinese New Year holiday, the combined new energy passenger vehicles insured over January-February reached 685,000 units, jumping by 18.5% year on year from last year's 578,000 units.

By vehicle brand, in the first two months of this year, BYD had 257,400 units of new energy passenger vehicles insured in China, bringing its market share to 37.58%; while Tesla saw 61,300 units insured, logging a market share of 8.95%. And the insured volume of the top 5 best-selling new energy passenger vehicle models totaled 439,900 units, with its market share rising to 64.22%.

According to the statistics, leading electric car makers could effectively boost car sales via price cuts, and they may further reduce NEV prices on lower battery costs given the sharp drop in lithium carbonate prices. It is expected that the insured volume of Chinese new energy passenger vehicles may rise to 520,000 units in March.

Figure 1-1: Insurance registrations of new energy passenger vehicles in China (Unit: '0000 units)

Sources: Compulsory traffic insurance and Mysteel

Although China's passenger vehicle sales decreased by 19.8% year on year over January-February due to macro factors, the NEV portion still grew 18.5% compared with last year, though the pace slowed. The penetration rate of new energy passenger vehicles increased to 34.5% over March 6-12, a sustaining rise after the phase-out of NEV subsidies indicating that NEVs have a greater endogenous growth driver compared with traditional fossil-fueled vehicles.

Growing consumer acceptance is seen as a major driving force behind the NEV market, along with its improved product competitiveness. The recent price cuts in fossil-fueled cars, however, have cast a shadow on the expectation for NEV sales in the first half of this year. Nevertheless, according to Mysteel, the price reduction for conventional fossil-fueled cars would simply encourage consumers to buy cars ahead of schedule rather than cutting into the NEV market.

Figure 1-2: China's weekly NEV penetration rate based on collected data of compulsory traffic insurance

Sources: Compulsory traffic insurance and Mysteel

The rivalry amongst new energy car makers is getting more fierce, as more new NEV models have been launched this year. According to the monthly insurance registrations in China, the market share of the top 10 brands in terms of insured volume reached 79.51% in January and 77.7% in February respectively. In a market dominated by a cluster of leading NEV automakers, these leading automakers will gradually gain control over the pricing power of the entire industry, and squeeze profit margins of automotive accessory manufacturers and material factories in the upstream.

Table 1-1: Top 10 new energy passenger vehicle brands in insured volume (Unit: units)

|

Brand |

In Feb. |

Market share |

In Jan. |

Market share |

|

BYD |

139,490 |

35.36% |

117,906 |

40.53% |

|

Tesla |

34,082 |

8.64% |

27,224 |

9.36% |

|

Wuling Motors |

31,608 |

8.01% |

18,956 |

6.52% |

|

Aion |

28,778 |

7.30% |

15,481 |

5.32% |

|

Changan Auto |

18,627 |

4.72% |

15,202 |

5.23% |

|

Li Auto |

16,998 |

4.31% |

10,078 |

3.46% |

|

Nio |

11,908 |

3.02% |

8,074 |

2.78% |

|

Geely Auto |

8,981 |

2.28% |

7,313 |

2.51% |

|

Hozon Auto |

8,558 |

2.17% |

5,633 |

1.94% |

|

Volkswagen |

7,708 |

1.95% |

5,459 |

1.88% |

|

Top 10 bands in total |

306,738 |

77.77% |

231,326 |

79.51% |

|

NEV in total |

394,440 |

100.00% |

290,938 |

100.00% |

Sources: Compulsory traffic insurance and Mysteel

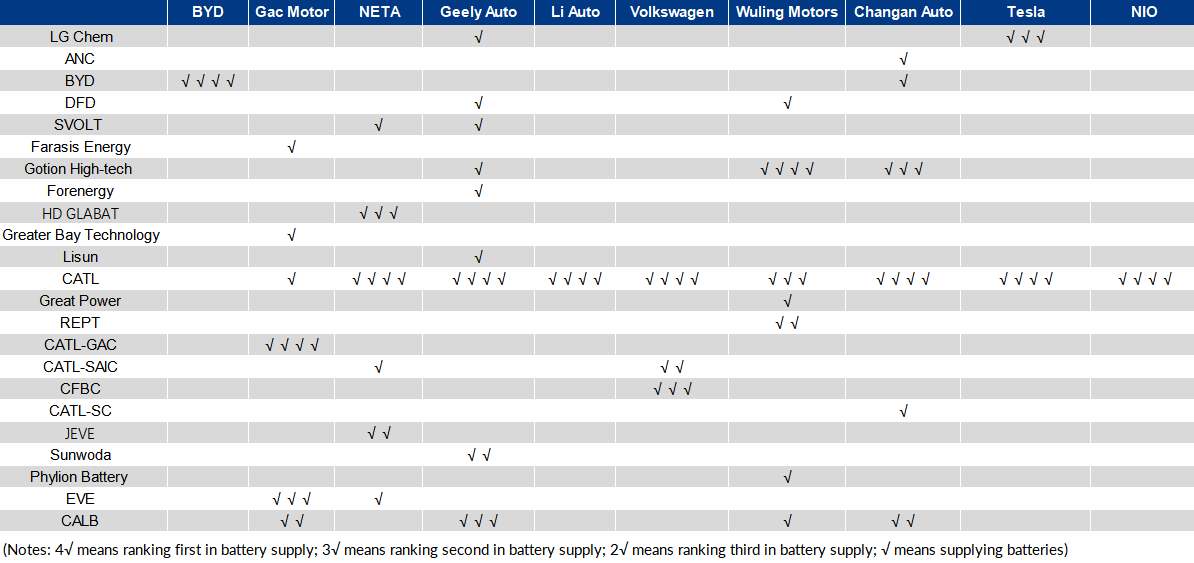

Major battery suppliers for the top 10 car brands in terms of NEV sales in February include CATL, BYD, CALB, and SVOLT Energy. Of these, CATL and BYD have a combined installed capacity of 17.1 GWh, accounting for 77.95% of the total market.

Table 1-2: Battery suppliers for the top 10 new energy passenger vehicle brands

Sources: Compulsory traffic insurance and Mysteel

Against the backdrop of a sharp decline in downstream demand for power batteries to a year-on-year growth of 18.5% over January-February this year from the 80.31% surge for the whole of 2022, CATL, the world's largest electric vehicle battery maker, proposed a "lithium-ion rebate program" to secure leading NEV automakers' needs for batteries. This program will make it more difficult for small- and medium-sized battery plants to receive orders, and small- and medium-sized cathode material plants will also see fewer orders and lower their operating rates, which will finally have an impact on the retail pricing of raw materials in the market. That's why a pessimistic sentiment is spreading in the new energy sector at present.

The industrial development cycle shows that China's new energy sector has developed from rapid expansion into its mature stage which tends toward oligopolies. For enterprises engaged in the new energy sector, cost advantages will be regarded as their core competitiveness and a new pricing system for raw materials is likely to emerge in the future.

Written by Mysteel Nonferrous Metal & New Energy Research Center

Edited by Ruby Zhang, zhangjiajing@mysteel.com; Alyssa Ren, rentingting@mysteel.com