Lithium hydroxide (LiOH) is an important inorganic compound, typically appearing as a white crystalline powder. It is strongly alkaline, easily soluble in water, and slightly soluble in ethanol. As a critical raw material for lithium compounds, lithium hydroxide plays an irreplaceable role in the field of lithium-ion batteries, particularly in the production of high-nickel ternary cathode materials.

Compared to lithium carbonate, lithium hydroxide has a lower melting point (471°C for monohydrate lithium hydroxide versus 720°C for lithium carbonate). During the sintering process, the lower melting point allows lithium hydroxide to mix more uniformly and thoroughly with ternary precursors, thereby reducing surface lithium residue and effectively enhancing the material's specific discharge capacity.

Additionally, lithium hydroxide can achieve stable material performance at lower sintering temperatures, helping to reduce cation mixing and further improve cycling stability. In contrast, lithium carbonate typically requires sintering at temperatures above 900°C, making it difficult to meet the lithium source requirements for high-nickel ternary materials.

In the production of medium and low-nickel ternary materials (such as NCM 523), the more cost-effective battery-grade lithium carbonate is often used as the lithium source due to relatively lower purity requirements for lithium sources. However, for materials like NCM 622, lithium hydroxide not only delivers more ideal electrochemical performance but is also the preferred choice for overseas cathode material manufacturers.

I. Production Processes of Lithium Hydroxide

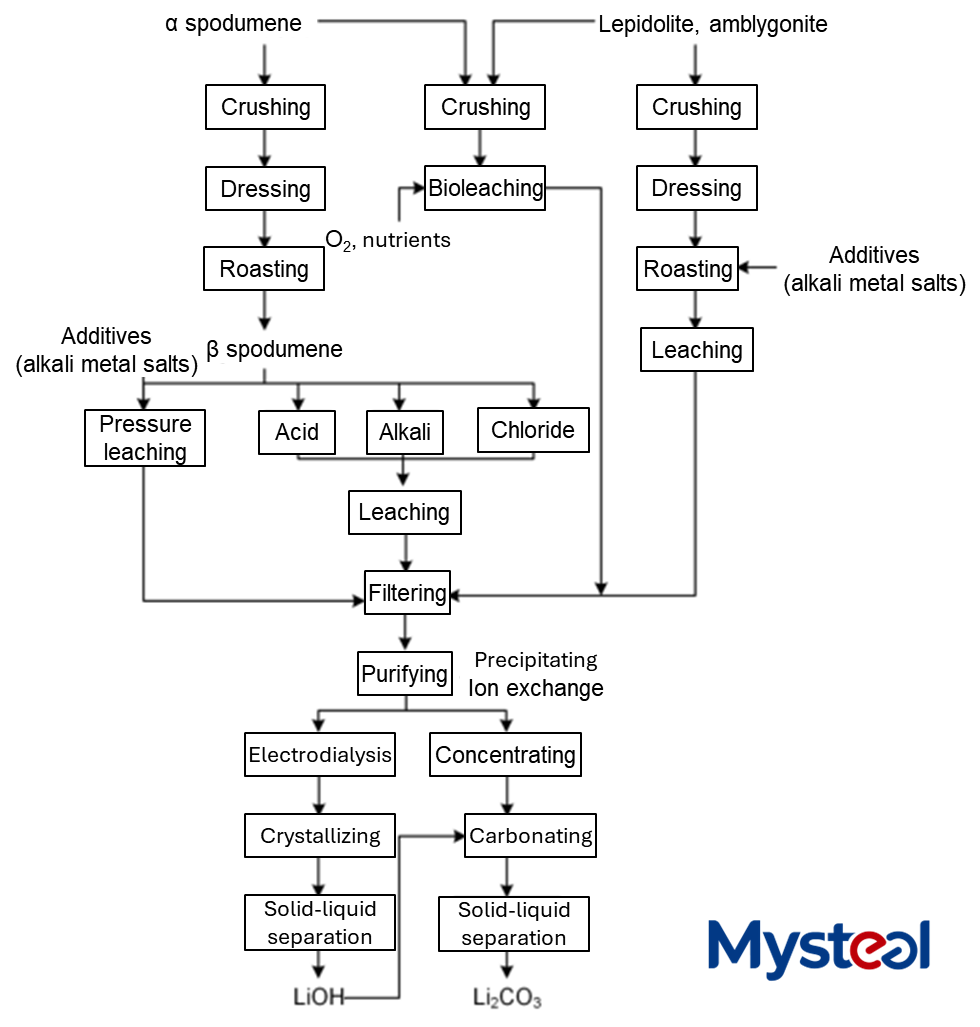

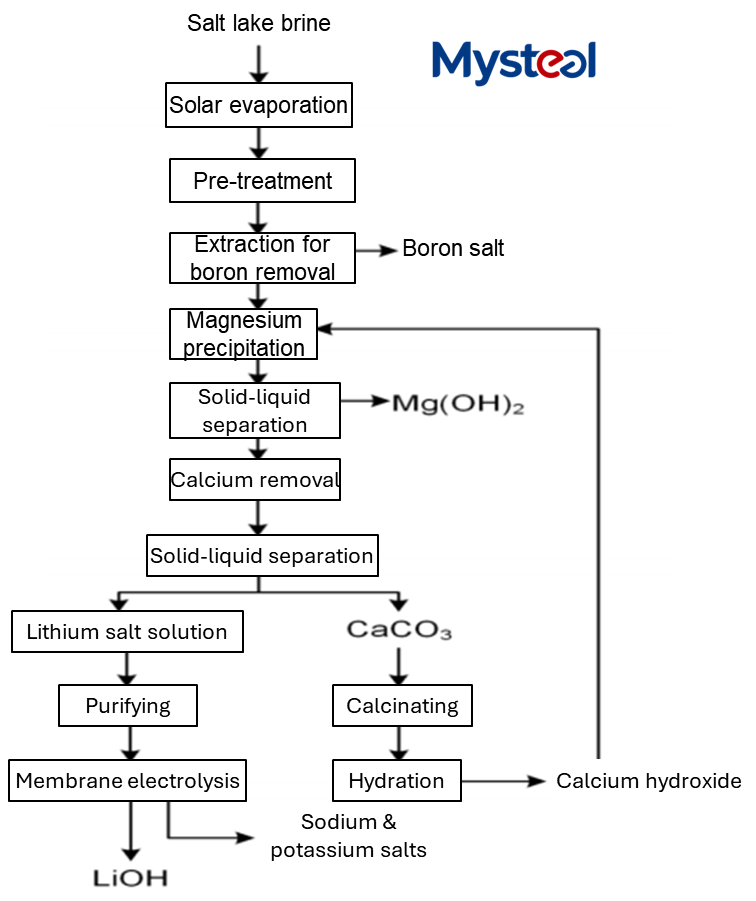

There are currently three prevailing routes for extracting lithium from lithium ores, including acid, alkali, and chlorination roasting methods, which are shown in the image below.

For spodumene, it requires high-temperature roasting to transform the mineral phase into the more reactive ß-spodumene; while lepidolite, rich in valuable metal components such as rubidium and cesium, can achieve higher extraction rates of lithium, rubidium, and cesium by adding alkali metal salt additives during roasting.

The cost of producing lithium from brine is generally lower than from pegmatites. However, due to the significantly lower lithium content in domestic salt lakes compared to those in South America and other regions, as well as the complexity of impurities, the lithium extraction process is more challenging. It is only in recent years when domestic salt lake lithium extraction has become more economically viable and promising for investment, with the substantial rise in lithium prices and breakthroughs in lithium extraction technologies such as lithium-ion sieve adsorption and electrochemical lithium extraction.

II. Global Lithium Hydroxide Capacity Distribution

China is an important hub for global lithium hydroxide production, accounting for 77.9% of the world's total capacity by 2024. China's lithium hydroxide capacity consists of smelting and causticization, with a share of 75% and 25% respectively.

In contrast, overseas capacity is more dispersed, mainly located in South America and Australia. Overseas resource countries typically prefer exporting lithium concentrates or lithium carbonate, while the deep processing of lithium hydroxide is mostly in China.

III. China's Lithium Hydroxide Production

According to Mysteel's data, the lithium hydroxide production by major Chinese manufacturers totaled approximately 259,700 tonnes in 2024. Starting in the second half of 2024, the lithium hydroxide demand weakened, prompting some smelters to focus on lithium carbonate production, leading to a continuous decline in lithium hydroxide output.

In January 2025, the production of lithium hydroxide stood at around 16,300 tonnes, a month-on-month decrease of 18.3%. Domestic lithium hydroxide smelters kept their operating rates at a low level, with some experiencing reduced orders. Additionally, a major smelter in Sichuan Province underwent a full-line maintenance in January, resulting in a significant drop in production.

In February 2025, China's lithium hydroxide production is estimated at 13,700 tonnes, a month-on-month decrease of 15.6% due to extended turnaround of some refineries and lackluster demand in the ternary battery sector.

IV. China's Lithium Hydroxide Operating Rates

At the beginning of 2024, the lithium hydroxide smelters' operating rates were low due to the impact of the Chinese New Year holiday. In the second quarter, the smelters' operating rates increased as lithium hydroxide prices rebounded amidst rallying lithium carbonate prices and a slight recovery in downstream demand. Starting the second half, the lithium hydroxide operating rates faced continuous pressure from reduced orders and shift to lithium carbonate.

At the beginning of 2025, the operating rates went down further after a major smelter in Sichuan underwent full-line maintenance, in addition to reducing orders and companies taking CNY holiday.

Looking ahead, the release of new capacity is likely to lift the operating rates, but the short-term operating rates are unlikely to improve should the demand stay muted.

V. Outlook

The price trend of lithium hydroxide is largely subject to the recovery of high-nickel ternary battery demand and changes in lithium ore supply. The lithium hydroxide prices may rebound if high-nickel ternary battery demand recovers beyond expectations or lithium ore supply tightens. However, it seems that the current focus is still on the balance between lithium carbonate and lithium hydroxide capacity allocation, as well as how to optimize the overall utilization efficiency of lithium resources while meeting the demand for high-nickel ternary cathode materials.

Written by Aggie Hu, huchenying@mysteel.com