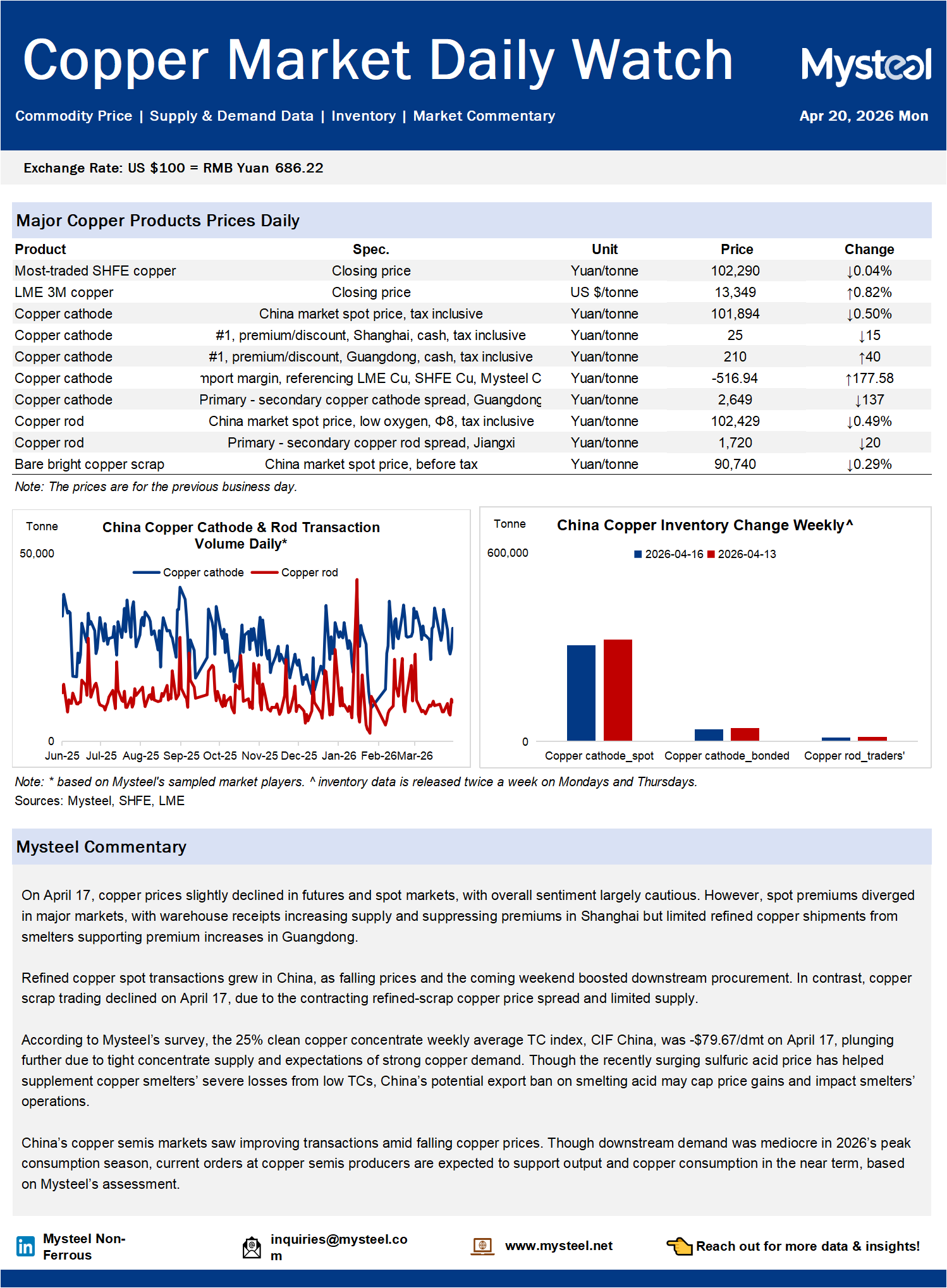

On April 17, copper prices slightly declined in futures and spot markets, with overall sentiment largely cautious. However, spot premiums diverged in major markets, with warehouse receipts increasing supply and suppressing premiums in Shanghai but limited refined copper shipments from smelters supporting premium increases in Guangdong. Refined copper spot transactions grew in China, as falling prices and the coming weekend boosted downstream procurement. In contrast, copper scrap trading declined on April 17, due to the contracting refined-scrap copper price spread and limited supply. According to Mysteel's survey, the 25% clean copper concentrate weekly average TC index, CIF China, was -$79.67/dmt on April 17, plunging further due to tight concentrate supply and expectations of strong copper demand. Though the recently surging sulfuric acid price has helped supplement copper smelters' severe losses from low TCs, China's potential export ban on smelting acid may cap price gains and impact smelters' operations. China's copper semis markets saw improving transactions amid falling copper prices. Though downstream demand was mediocre in 2026's peak consumption season, current orders at copper semis producers are expected to support output and copper consumption in the near term, based on Mysteel's assessment.

Don't miss Mysteel's Q2 2026 Copper Market FREE Webinar! Check the link below to learn more, and register to secure your spots:

Q2 2026 Copper: Price Volatility, Raw Material Tightness, and What's Next?