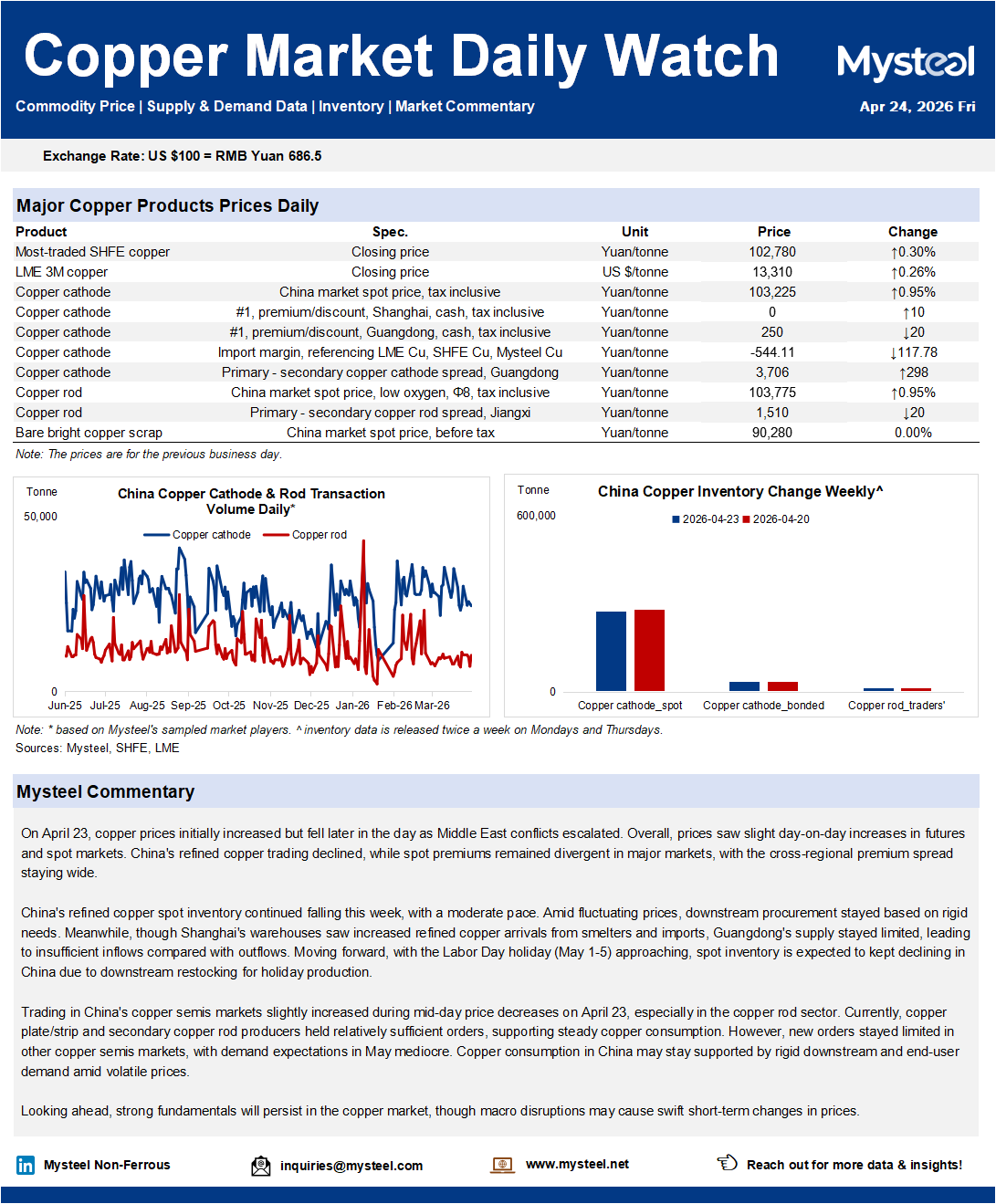

On April 23, copper prices initially increased but fell later in the day as Middle East conflicts escalated. Overall, prices saw slight day-on-day increases in futures and spot markets. China's refined copper trading declined, while spot premiums remained divergent in major markets, with the cross-regional premium spread staying wide.

China's refined copper spot inventory continued falling this week, with a moderate pace. Amid fluctuating prices, downstream procurement stayed based on rigid needs. Meanwhile, though Shanghai's warehouses saw increased refined copper arrivals from smelters and imports, Guangdong's supply stayed limited, leading to insufficient inflows compared with outflows. Moving forward, with the Labor Day holiday (May 1-5) approaching, spot inventory is expected to kept declining in China due to downstream restocking for holiday production.

Trading in China's copper semis markets slightly increased during mid-day price decreases on April 23, especially in the copper rod sector. Currently, copper plate/strip and secondary copper rod producers held relatively sufficient orders, supporting steady copper consumption. However, new orders stayed limited in other copper semis markets, with demand expectations in May mediocre. Copper consumption in China may stay supported by rigid downstream and end-user demand amid volatile prices.

Looking ahead, strong fundamentals will persist in the copper market, though macro disruptions may cause swift short-term changes in prices.

Don't miss Mysteel's Q2 2026 Copper Market FREE Webinar! Check the link below to learn more, and register to secure your spots:

Q2 2026 Copper: Price Volatility, Raw Material Tightness, and What's Next?