UAE's OPEC+ Exit: Is the Era of 'Great Coordination' in Oil Supply Over?

01 Long-Term Divergence: The 'Irreconcilable' Clash Between Capacity Investment and National Strategy

The chronic friction between the UAE and OPEC's core members (especially Saudi Arabia) is rooted in the fundamental conflict between its massive capacity investments and the production cut constraints of OPEC+.

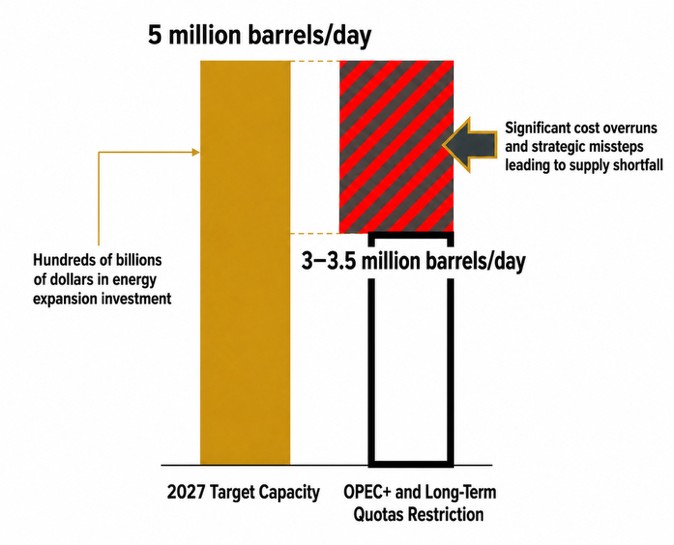

In recent years, the UAE has poured tens of billions of dollars into expanding its oil and gas capacity, aiming to boost crude production capacity to 5 million barrels per day by 2027. However, under the collective output cut framework of OPEC+, its production has long been capped at 3 to 3.5 million bpd, leaving a vast amount of converted spare capacity unable to be into actual revenue and strategic leverage.

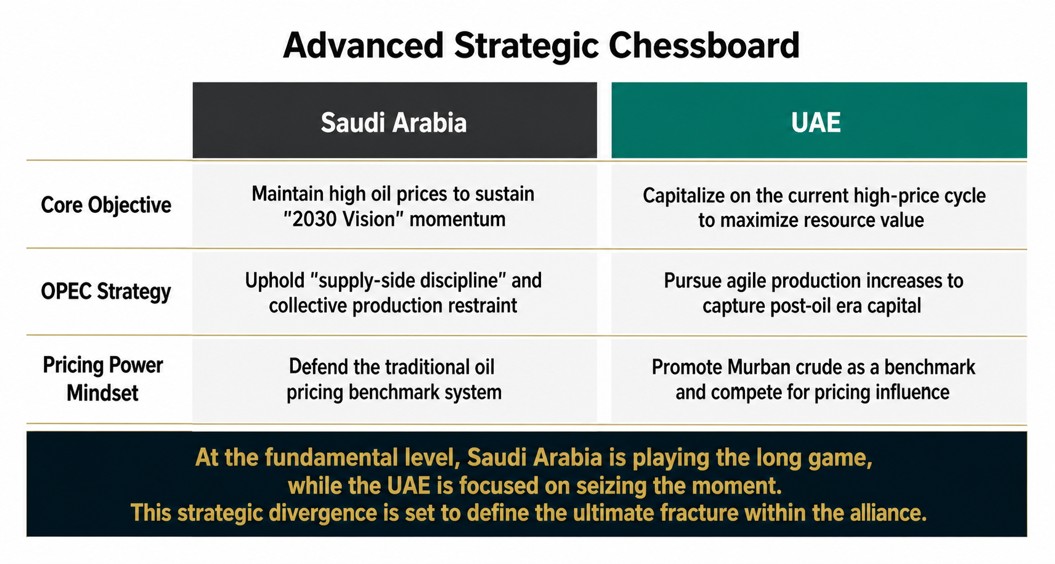

A deeper underlying cause lies in the diametrically opposed national development strategies:

Saudi Arabia-led OPEC+ strategy aims to maintain elevated oil prices through "supply-side management," buying time and funding for its "Vision 2030" transition.

The UAE's "economic diversification" strategy is far more aggressive. Its logic is: to seize the current high-prosperity cycle in the oil and gas sector to achieve "maximum resource monetization," amassing substantial capital for the post-oil era. Concurrently, the UAE is strongly promoting its own Murban crude futures to vie for pricing power in the Asia-Pacific market, which requires a flexible production policy for support. The production cut agreement has become a "stumbling block" to its national strategy.

02 The Strait Crisis: Removing the 'Final Hurdle' to Withdrawal

Rumors of the UAE intending to exit OPEC have surfaced multiple times since 2021, but were all officially denied. Previously, two major concerns held it back: first, the fear that unilateral production hikes would trigger a price war, cannibalizing its own fiscal revenue; second, the apprehension of damaging diplomatic relations with Gulf allies like Saudi Arabia and the United States.

However, the outbreak of the Strait of Hormuz crisis fundamentally altered the risk calculation equation.

- Evaporation of Oil Price Concerns: With shipping through the strait currently obstructed, approximately 15 million bpd of Persian Gulf crude exports face the risk of disruption. The market's core contradiction has shifted from "fear of surplus" to "fear of shortage." At this juncture, increasing production will not depress oil prices; instead, it can fill the massive supply gap, stabilize the market, and win international acclaim (especially from crude importing nations).

- Reconstruction of Security Concerns: The crisis exposed the vulnerabilities of relying on a single security pillar (the US). Through this crisis, the UAE has further solidified its resolve to build diversified security channels and strengthen ties with non-traditional partners. The weight of diplomatic risks has significantly diminished in the face of national survival and development imperatives.

03 The Eastern Journey: The 'Final Confirmation' of Strategic Resolve

The UAE Crown Prince's recent high-profile "Eastern Journey" served as the definitive validation for this strategic layout. Judging from the comprehensive, strategic cooperation agreements reached between the two sides, the UAE has clearly secured crucial "certainty" and "confidence endorsement" regarding energy security, investment guarantees, and political support. This provided the critical geopolitical backing for its immediate announcement to exit OPEC+ upon returning home. This trip signifies a historical recalibration of the UAE's diplomatic and energy strategic focus.

Oil Price Impact: Short-Term Cooling and Long-Term Paradigm Shift

In the short term, the UAE's exit acts as a "cooling agent" and sentiment "hedging buffer" against extreme oil prices.

- Psychological Shock: The news itself directly fractured the market's faith in the OPEC+ "production cut to support prices" narrative, triggering a sharp short-term plunge in oil prices.

- Flexible Gap Filling: The UAE possesses nearly 2 million bpd of spare capacity. Its production increase can effectively alleviate the physical supply shortage caused by the strait blockade.

- Pragmatic Blockade Breakthrough: There are indications that UAE oil tankers are attempting to break through the "dual blockade" to supply the market directly. This "pragmatic solo" model outside the OPEC framework will provide invaluable elasticity to the global supply chain.

In the long term, this marks a "paradigm shift" in the global crude oil supply side.

- Substantive Disintegration of the OPEC+ Agreement: The departure of a core producing nation has dealt a heavy blow to the organization's internal unity and discipline. The restrains on global crude supply have been loosened, making the model of regulating oil prices through collective action difficult to sustain.

If you are also pondering a series of critical questions following the UAE's exit:

- Will the OPEC+ production cut alliance disintegrate entirely, or initiate a new round of "shadow price wars"?

- After the short-term "gap filling," how will global crude trade flows be reconfigured?

- How will the evolution of the Middle East geopolitical landscape affect long-term pricing benchmarks and contract models?

- Facing the transition from "coordination" to "competition" on the supply side, how should Chinese refiners and traders adjust their procurement strategies and hedging logic?

You will find that the real challenge is never just knowing the event itself, but rather, in the early stages of a paradigm shift, how to cut through the noise and make strategic forecasts one step ahead of the market.

Changes driven collectively by national strategic shifts, geopolitical alliance restructuring, and supply chain elasticity demands will never be a one-off impact, but will be accompanied by fluctuations of "gameplay-testing-rebalancing," continuously reshaping industry rules.

This is precisely the core focus we continually hone: using the perspective of a "China market decipherer" to deconstruct grand structural shifts into trackable signals, assessable impacts, and executable decisions. We are dedicated to helping decision-makers see the underlying threads amidst turbulence and find the path forward before divergences emerge.

For decision-makers navigating this "turbulent time" and seeking to understand the market signals behind these grand shifts in national strategy, alliance structures, and supply chain resilience, GL CONSULTING acts as your CHINA DECODER.

For structured, forward-looking analysis, reach out for a sample of our China Energy Policy Perspective report.

Class 1-equivalent met coke (CDQ) prices: China's major cities

Aug 06, 2026 17:38

Met coke portside prices: Tianjin port

Aug 06, 2026 17:37

Class 1 met coke prices: China's major cities

Aug 06, 2026 17:37

Met coke prices: Linfen

Aug 06, 2026 17:35

Semi coke prices: Shenmu

Aug 06, 2026 17:31