As the industry widely expects inventories to keep drawing down through May and June, China's domestic lithium carbonate prices have been on a steady upward trajectory entering May, reaching a new high for the year and briefly touching the key resistance of Yuan 210,000/tonne. The limit of this rally will likely hinge on when downstream demand starts to push back.

In detail, China's lithium carbonate prices have risen continuously since late April, supported by stronger downstream production schedules and firm lithium ore spot prices. Yet spot trading has stayed limited, with the ongoing price hike curbing downstream appetite.

On the supply side, China's lithium carbonate is likely to fall 3.9% month-on-month (MoM) at around 99,500 tonnes in May, based on the production scheduling of Mysteel's sampled converters, while the April production has already missed expectations and dropped 1.1% MoM.

The May lithium carbonate production is expected to be shaped once again by cuts in spodumene-based production lines, where low raw material inventories have forced some converters to lower their schedules, while a few have arranged routine maintenance. Salt lake producers have increased the production modestly, but their overall contribution remains small. Lepidolite operations, meanwhile, have maintained steady operating rates.

Overseas, Imports: Chilean customs data show April lithium carbonate exports to China reached 22,956 tonnes, rising 21.3% MoM and 47.7% YoY. Lithium sulfate exports to China stood at 12,100 tonnes, contracting 26.8% MoM. Recent increases in Chilean shipments, partly due to higher salt lake output and inventory releases, suggest Chinese imports will remain high over the next two months.

On the demand end, China's lithium iron phosphate cathode production is expected to rise further to 498,800 tonnes, a monthly increase of 4.3%. The cathode plants' orderbooks have remained satisfactory, in addition to some new capacity in ramp-up. Future output will depend on new capacity progress and the supply stability of key raw materials such as iron phosphate.

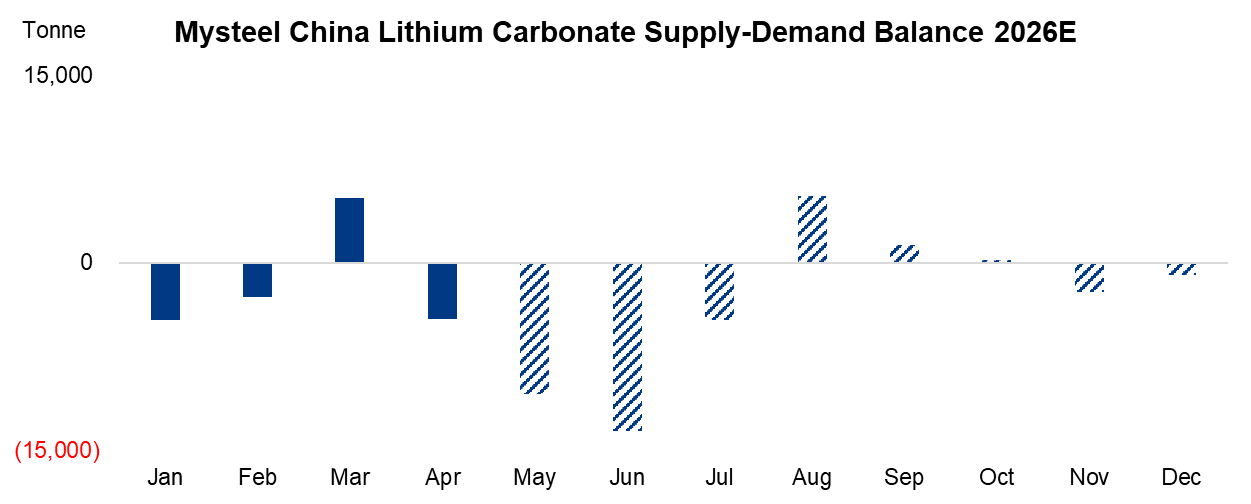

Taken together, a significant inventory drawdown is expected in May, with a potential inventory drawdown of 10,457 tonnes. While monthly carbonate imports are expected to remain above 30,000 tonnes, tighter ore supply will reduce some converters' operating rates, lowering total supply compared to April.

Source: Mysteel

On the inventory front, from mid-April to early May, weak basis prompted the traders to deliver against futures, driving total lithium carbonate warehouse receipts from around 27,000 tonnes to near 46,000 tonnes. The rapid and large accumulation has raised concerns that rising deliverable volumes may pressure front-month futures prices.

The traders also reported temporary inventory accumulation. Based on Mysteel's survey of 43 sampled traders, the marketable lithium carbonate inventory rose 3,610 tonnes from the previous session and recorded 42,260 tonnes in the week ending May 8 primarily because the downstream sales stayed slow amidst while the converters actively made shipment when the lithium prices were high.

Looking ahead, the lithium carbonate market will likely see continued inventory drawdown over the next two months when tight spot lithium ore supply is unlikely to ease in May-June, and demand growth is already outpacing monthly supply growth. In addition, the monthly average lithium carbonate prices are expected to rise gradually until downstream demand shows negative feedback.

In the medium term, we maintain the view that lithium prices will remain firm through 2026 on the backdrop of ongoing lithium ore supply disruptions, combined with new LFP and cell capacity scheduled to come online in the second half of the year.

Written by Aggie Hu, huchenying@mysteel.com