Hog prices remain capped by surplus supply and soft demand

Contrary to expectations of a continued price rally given before Labor Day holiday, the post-holiday hog market fell short and remained soft. According to Mysteel's assessment, the national average slaughter price of DLY hogs stood at Yuan 9.58/kg on May 14, flat from the previous day. Market sentiment has gradually turned pessimistic, pointing to strong upward resistance.

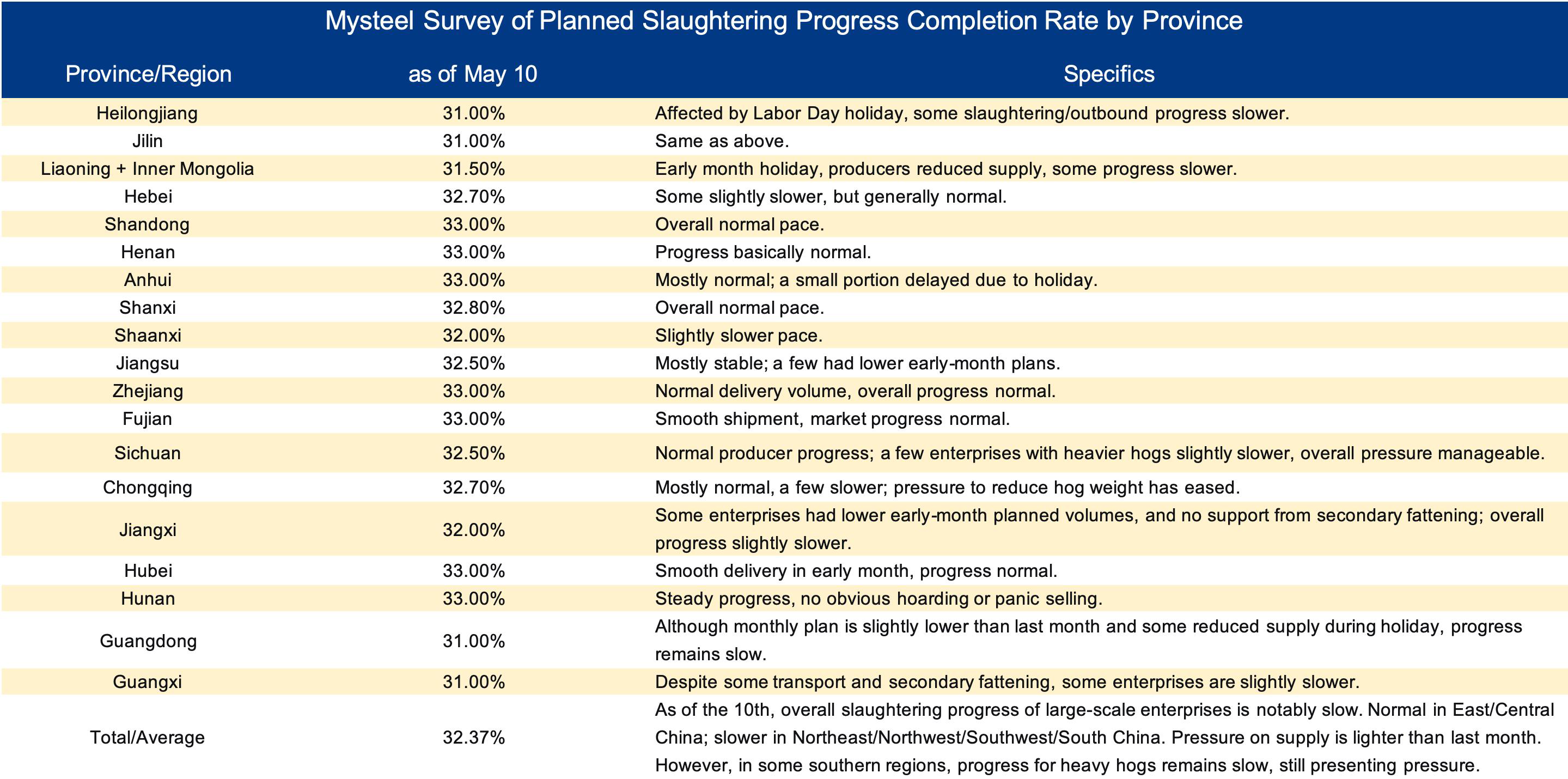

data source: Mysteel

Although large-scale farming enterprises have reduced their planned slaughter volumes for May compared with April, the supply pressure has yet to be meaningfully alleviated. Mysteel's survey data show that planned slaughter volumes of key provincial farming enterprises in May actually decreased by 3.53% month-on-month. Among the 18 monitored provinces and cities, most posted declines of varying degrees, with only a few recorded slight month-on-month increases.

However, the terminal demand turned soft after prices rebounded, leaving short-term supply pressure still high. Meanwhile, national live hog slaughter in the first quarter rose 2.8% year-on-year, and the sow herd at the end of the quarter remained at elevated levels, exerting sustained pressure on any price rebound.

Weak demand is the core factor restraining hog price rebounds. On a year-on-year basis, pork consumption has increased slightly, but this represents only a modest recovery from a low base, driven largely by lower prices that have spurred consumption.

During the Labor Day holiday, catering consumption saw a short-lived surge, temporarily lifting slaughter volumes. After the holiday, the market quickly returned to the consumption off-season, with slaughterhouse orders decreasing, and fresh pork sales slowing markedly. Rising temperatures have dampened household consumption willingness, while restaurant and canteen demand has receded seasonally. The phase of demand contraction has directly suppressed the potential for price rebounds.

On the other hand, both smallholders and secondary-fattening operations have increased their willingness to sell when the profit margins for farmers holding fat pigs have been squeezed as recent price spread between standard-weight and fat-weight pigs has been narrowing.

The concentrated release of heavy pigs has intensified market supply pressure. Amid persistent industry losses, hog farmers face cash flow pressures. Confronted with an inverted standard-to-fat price spread, they are more inclined to sell fat hogs for cash, leading to an increase in fat pig supply in the market.

At the same time, earlier fat pig hoarding is being released in a concentrated manner. While the slaughterhouses are purchasing only for essential needs, they are inclined to drive prices down, further reinforcing the weak price trend.

The supportive effect of policy measures such as government pork reserve purchases is gradually weakening. Market sensitivity to such measures has declined, and their role in supporting sentiment continues to fade. Although central and local governments have continued to launch frozen pork reserve purchases to stabilize the prices, the scale of these purchases has been limited relative to the overall market, making it difficult to fundamentally alter the supply-demand balance.

After multiple rounds of reserve purchases, the market's reaction to policy stimulus has become muted, the marginal boost to market sentiment is diminishing, and the measures cannot effectively reverse pessimistic market expectations. In addition, the presence of low-priced transactions put downward pressure on market prices, further weakening the effectiveness of policy support.

More importantly, the core contradiction of oversupply remains fundamentally unchanged.

At the end of March 2026, the national sow herd stood at 39.04 million head, down month-on-month for nine consecutive months, yet still above the normal level of 39.0 million head and a long way from the regulatory target of 36.5 million head.

The combination of slow herd reduction and rising farming efficiency (PSY among leading enterprises generally exceeding 24 head) has partially offset the impact of falling sow numbers. Consequently, commercial pig is expected to remain oversupplied in the near term, with the lag effect of capacity cuts sustaining supply pressure and offering no fundamental support for hog prices.

To sum up, the live hog market is at a crucial bottom-firming stage. Price trends are expected to remain broadly stable, with movement likely confined to a narrow range, that is, the upward resistance is notably stronger. And a near-term price breakout remains unlikely under the combined weight of oversupply, seasonal demand weakness, fading policy effects, and sluggish capacity reduction, until capacity reduction meets expectations and demand shows a substantial recovery.

Galvanized steel pipe prices: Shenyang

Jul 03, 2026 13:50

Construction steel procurement prices: Tangshan

Jul 03, 2026 13:46

Construction steel prices: Tangshan

Jul 03, 2026 13:45

Construction steel prices: Qinhuangdao

Jul 03, 2026 13:45

Galvanized square pipe prices: Nanchang

Jul 03, 2026 13:38