Indonesia's new commodities mandate drives palm oil higher, palm oil's contango structure persist

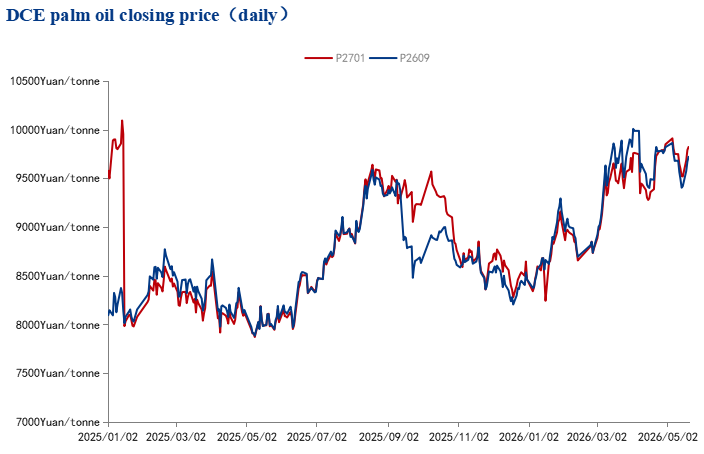

Palm oil prices surged significantly this week, with the benchmark futures contract hitting an intraday high of Yuan 9,845 per tonne.

The rally unfolded in three distinct phases. On Monday, palm oil broke from the previous week's downtrend, climbing from Yuan 9,460 /tonne to Yuan 9,532/tonne. This initial rise was primarily driven by higher crude oil prices. Following the U.S. president's visit to China, U.S. attention shifted back to the Middle East, where renewed expectations of a U.S.-Iran war pushed WTI crude oil back to $100 per barrel.

The next two phases saw additional support from palm-oil-specific bullish news. On Tuesday, market rumors emerged that Indonesia was preparing to establish a new state-linked export agency to centrally manage exports of specific commodities, including coal, crude palm oil, and minerals. On May 19, prices jumped nearly 150 points during the afternoon session.

Then, on Wednesday, Indonesian President Prabowo Subianto formally announced the implementation details and effective date of the policy. The president declared that export rights for strategic natural resources-such as coal and palm oil, on a dynamically adjustable list-would be transferred to state-owned enterprises (BUMN). Private companies will now be required to export through designated state-owned agents, with a transition period running until December 31, 2026. On May 20, prices rose again from Yuan 9,630/tonne to Yuan 9,845/tonne in the afternoon. The market reacted strongly to the news in the short term. This article briefly analyzes the policy's short- and medium-to-long-term impacts and the subsequent price outlook for palm oil.

As the world's largest palm oil producer, Indonesia consistently accounts for 55–60% of global production and over 60% of global exports, holding a dominant position in the supply chain. The policy effectively tightens Indonesia's export regime, potentially shifting palm oil pricing from market-based to policy-driven, making prices more susceptible to policy changes. In the short term, attention should be paid to potential reversals in Indonesia's export policy-any changes in implementation details, transition arrangements, or export pricing mechanisms could cause significant volatility in market sentiment. Additionally, the actions of Indonesian trading firms during the transition period warrant close observation: whether they accelerate selling at high prices or gradually transfer export businesses and contracts to state-owned enterprises could affect short-term exports.

Regarding immediate impacts, the policy's larger effects are on medium-to-long-term prices and global trade flows. Once the new export system is fully operational, global palm oil supply elasticity and price dynamics may face a new landscape. This is already reflected in near-term versus far-term prices. After the announcement, market sentiment quickly flared up but then retreated, with the DCE P2609 contract pulling back more sharply than the P2701 contract. Analyzing palm oil's contango structure and future trend requires considering other factors.

First, geopolitical tensions continue to influence crude oil prices, which in turn affect biodiesel demand and ultimately support palm oil demand and prices.

Second, weather and expectations of far-term production cuts persist: the potential threat of El Niño-typically bringing dry weather to Southeast Asia-continues to loom over palm oil supply prospects. Moreover, major producing countries are raising biodiesel blending mandates: Indonesia will launch B50 on July 1, and Malaysia has announced it will begin producing B15 biodiesel (15% palm oil content) starting in June to lower diesel prices. A supply-demand synergy could be seen in the second and third quarters of next year.

Given these factors, forward-month palm oil prices have stronger support than near-term prices. The benchmark palm oil futures contract is expected to trade in the range of Yuan 9,300–9,900/tonne, with forward-month contract prices having greater upside potential.

Iron ore concentrates procurement prices: Shandong major mills

May 22, 2026 20:55

Mysteel Iron Ore Index

May 22, 2026 19:06

Imported iron ore prices: China's major cities

May 22, 2026 18:23

Iron ore portside prices: Lanqiao Port

May 22, 2026 18:16

Iron ore portside prices: Caofeidian port

May 22, 2026 18:15