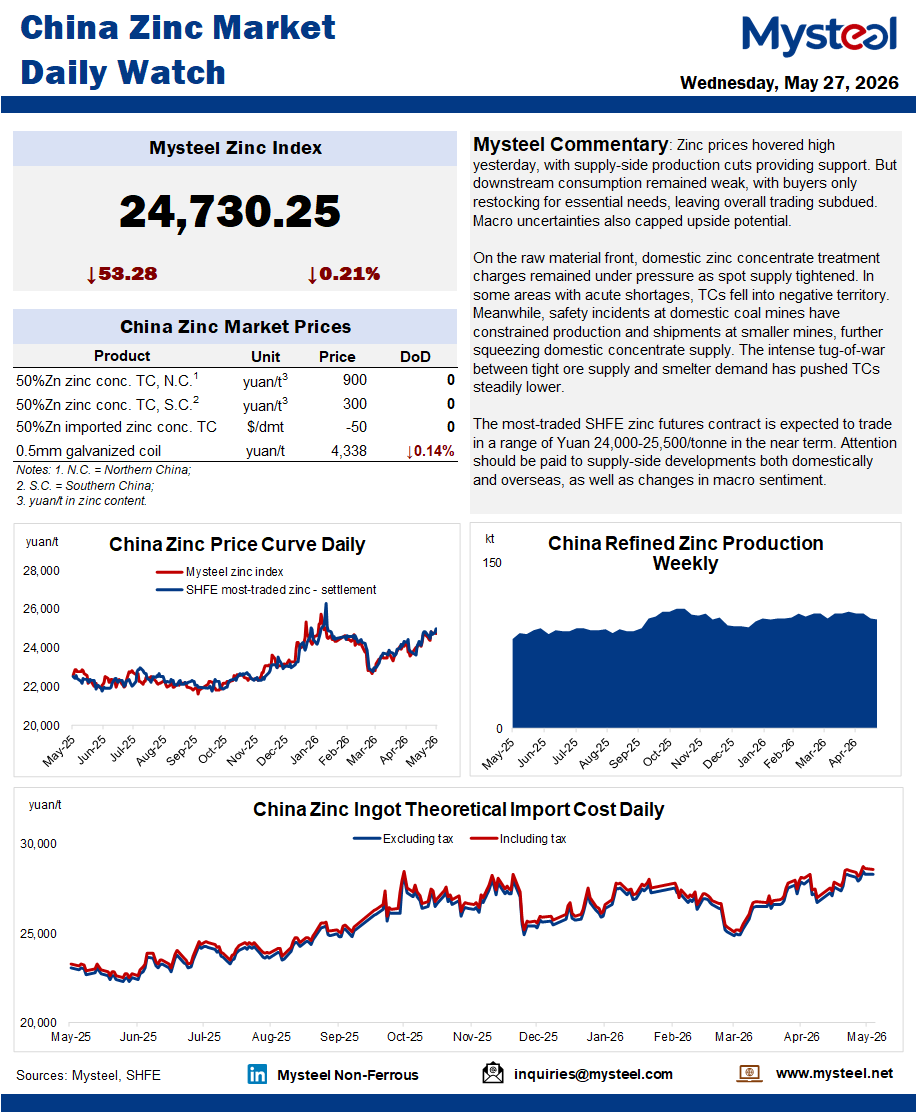

Zinc prices hovered high yesterday, with supply-side production cuts providing support. But downstream consumption remained weak, with buyers only restocking for essential needs, leaving overall trading subdued. Macro uncertainties also capped upside potential.

On the raw material front, domestic zinc concentrate treatment charges remained under pressure as spot supply tightened. In some areas with acute shortages, TCs fell into negative territory. Meanwhile, safety incidents at domestic coal mines have constrained production and shipments at smaller mines, further squeezing domestic concentrate supply. The intense tug-of-war between tight ore supply and smelter demand has pushed TCs steadily lower.

The most-traded SHFE zinc futures contract is expected to trade in a range of Yuan 24,000-25,500/tonne in the near term. Attention should be paid to supply-side developments both domestically and overseas, as well as changes in macro sentiment.