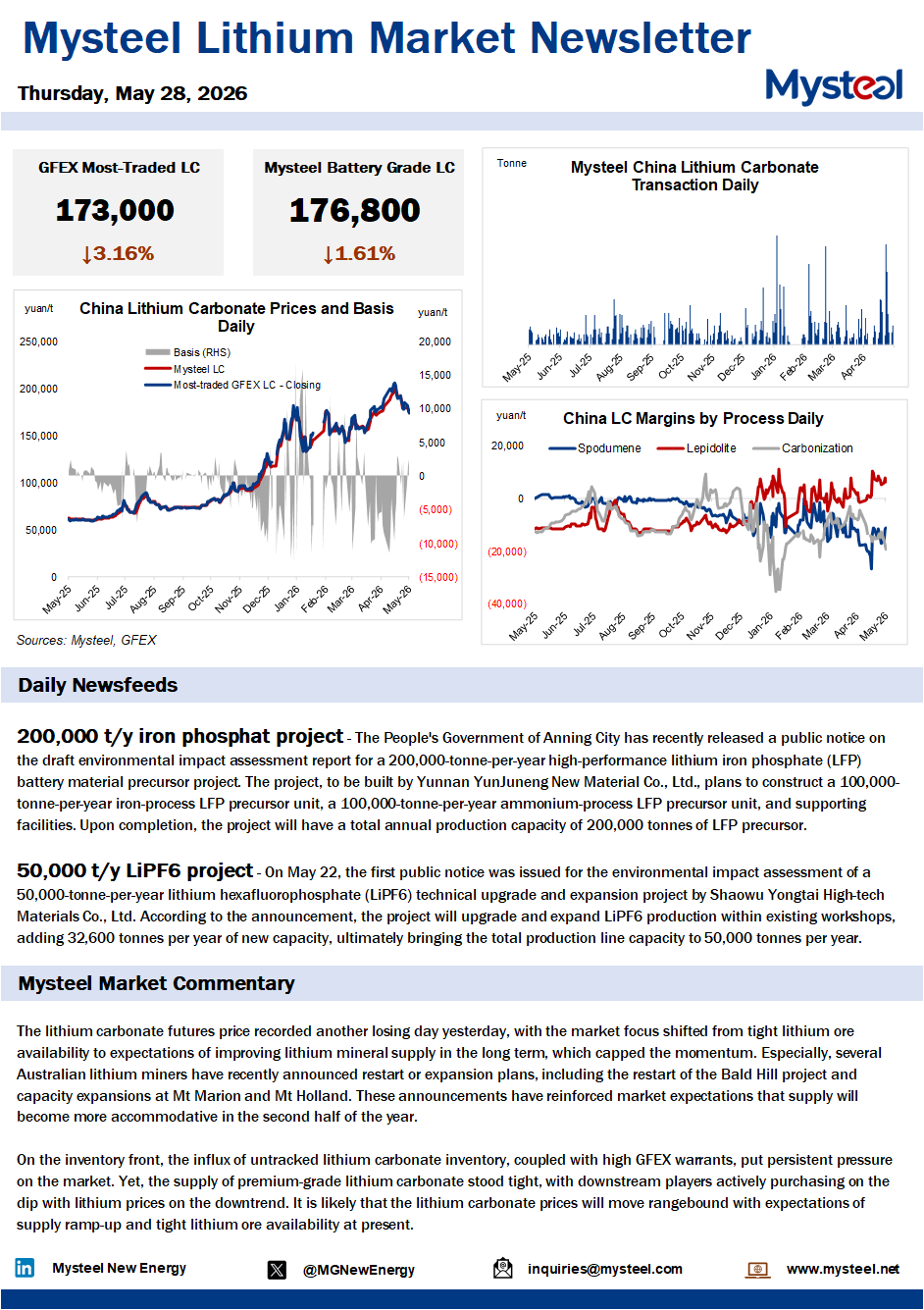

The lithium carbonate futures price recorded another losing day yesterday, with the market focus shifted from tight lithium ore availability to expectations of improving lithium mineral supply in the long term, which capped the momentum. Especially, several Australian lithium miners have recently announced restart or expansion plans, including the restart of the Bald Hill project and capacity expansions at Mt Marion and Mt Holland. These announcements have reinforced market expectations that supply will become more accommodative in the second half of the year.

On the inventory front, the influx of untracked lithium carbonate inventory, coupled with high GFEX warrants, put persistent pressure on the market. Yet, the supply of premium-grade lithium carbonate stood tight, with downstream players actively purchasing on the dip with lithium prices on the downtrend. It is likely that the lithium carbonate prices will move rangebound with expectations of supply ramp-up and tight lithium ore availability at present.