Two years after China first introduced reverse invoicing to address invoicing bottlenecks in metal scrap sector, the competitive landscape of the country's recycled copper industry is once again being reshaped, this time by a RMB 5 million annual cap. Many recycled copper traders say the limit for reverse invoicing is grossly inadequate, as high copper prices can exhaust the quota within just one or two months.

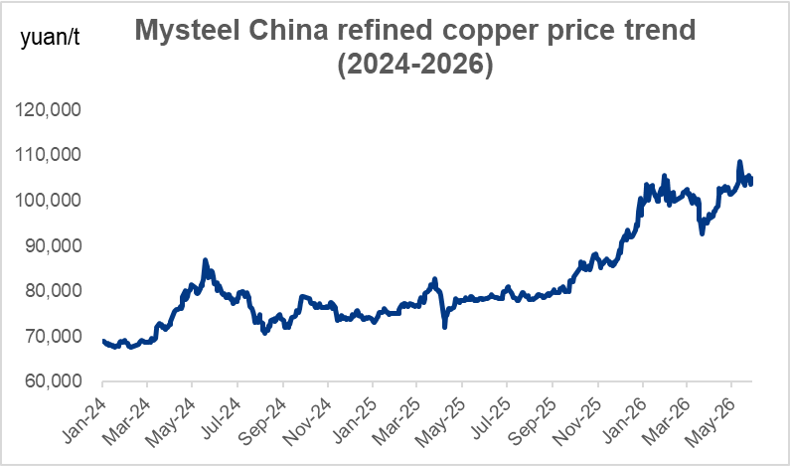

According to Mysteel's assessment, China's refined copper prices surged nearly 45% since the reverse invoicing system and invoicing cap was first introduced. For high-value non-ferrous metals like copper, a structural contradiction exists between "high commodity value" and "low credit limits," revealing a disconnect between the policy's intent and industrial reality.

Source: Mysteel

I. The Launch of the Reverse Invoicing Policy

In traditional renewable resource recycling, when recyclers purchase scrap copper and aluminum from fragmented individual sellers, such as dismantlers, waste pickers, and small-scale traders, these individuals are typically unable to issue Value-Added Tax (VAT) invoices themselves. This leaves recyclers lacking the "first invoice," preventing them from deducting VAT input tax or pre-tax cost expensing.

To address this point, the State Taxation Administration issued Announcement No. 5 of 2024 in April 2024. It permits qualified resource recycling enterprises to "reverse issue" invoices to individual sellers of scrap products. Under this mechanism, the recycling enterprise issues VAT general or special invoices on behalf of the upstream individual seller and handles the declaration and payment of related taxes. The announcement explicitly stipulates that the cumulative sales amount for which an individual seller benefits from reverse invoicing must not exceed RMB 5 million (ex-tax) over any rolling 12-month period. Once this limit is exceeded, recyclers must cease reverse invoicing and guide the seller to register as a business entity to issue invoices independently. This 5 million RMB cap mirrors the VAT threshold for small-scale taxpayers, designed to distinguish between occasional personal disposal and continuous commercial operations.

As reverse invoicing targets specific natural persons, tax law requires recyclers to collect the real-name ID information of sellers upon first transaction and obtain explicit written or electronic consent for tax declaration agency services. Enterprises must also maintain acquisition ledgers for inspection. The purpose is to lock in seller identity, ensure one-to-one correspondence between invoices and actual transactors, and prevent tax-related violations such as impersonation or income splitting by using others' identities. Consequently, many individual suppliers are reluctant to provide ID cards, fearing they will be flagged for subsequent personal income tax declarations or audits by the tax system.

II. Market Impact of the Reverse Invoicing Regime

Among major non-ferrous metals, scrap copper has been hit hardest by the reverse invoicing limits. High copper prices mean the 5 million RMB quota is easily maxed out. According to MySteel research, the 5 million RMB cap per entity, with some clients willing to issue only up to 2.1 million RMB, combined with a scarcity of suppliers willing to provide ID information, has further complicated policy enforcement.

A more critical shift is occurring in transaction models. The implementation details of reverse invoicing rules, combined with recent special tax inspections targeting fraudulent VAT invoicing in the renewable resources sector, have made downstream copper smelters wary. Most copper plants have stopped accepting reverse invoices altogether to avoid being implicated in upstream audits and increasingly prefers invoiced scrap copper, hindering transaction flow.

This shift has directly pushed up invoice point costs. According to Mysteel's tracking, demand for invoices for copper scrap has surged significantly, driving the invoice point rate persistently higher to the range of 8.5% to 9.5%, or even 10% in the first quarter of 2026. This marks a notable increase compared to historical levels, further squeezing margins for recycled copper traders.

During the first quarter of 2026, China's domestic secondary copper supply stood at only 686,200 tonnes, a year-on-year decrease of 21.64%. Concurrently, secondary metal processing enterprises have increased imports, with scrap copper imports reaching 400,300 tonnes from January to February, up 4.64% year-on-year. Imported scrap is filling the domestic gap, establishing a clear trend of structural substitution.

III. Conclusion

In the short-term, it is inevitable that compliance costs rise due to reverse invoicing. Long-term success, however, will depend on an enterprises ability to transform compliance capabilities into core supply chain management strengths, determining their survival in this round of industry consolidation.

Written by Regina Wang, wangjiaqie@mysteel.com

Edited by Aggie Hu, huchenying@mysteel.com