Soybean: The DCE No.1 soybean contract traded higher on concerns over soil moisture deficit in Northeast China, acreage cut expectations, and high state auction prices, though gains were capped by weak demand in off-season, import substitution, and bulls profit-taking. On the spot side, sellers in Northeast China held back supplies, with 39.5% protein beans at Yuan 2.38-2.42/jin, while pre-holiday (Dragon Boat Festival) buying by tofu processors has started but remains modest.

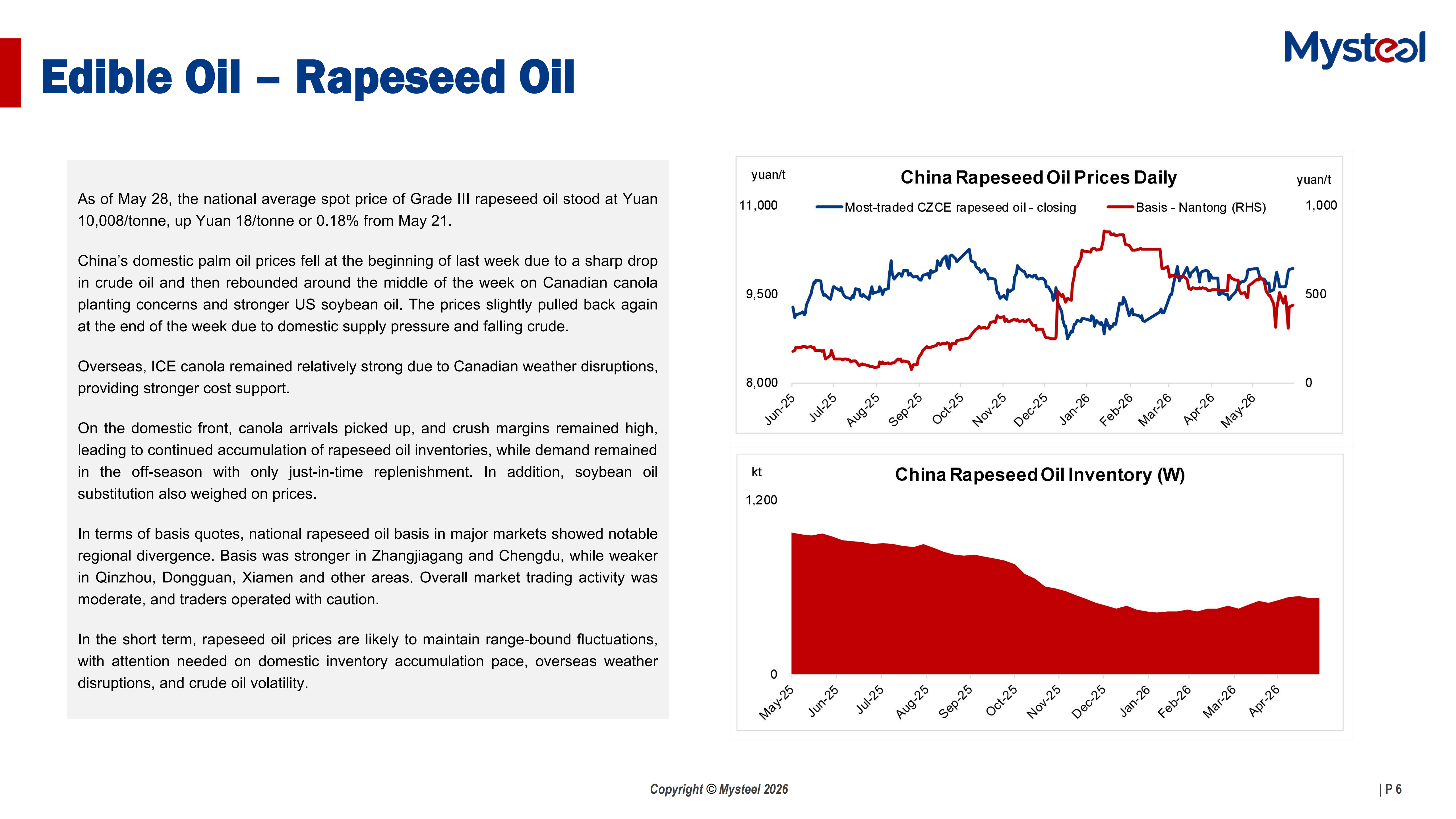

Edible Oil: The domestic edible oils market saw strong support from overseas market, where prices were supported by US biofuel policies and Indonesia's palm oil export mandate. Domestically, large soybean arrivals and rising palm oil stocks kept prices under pressure.

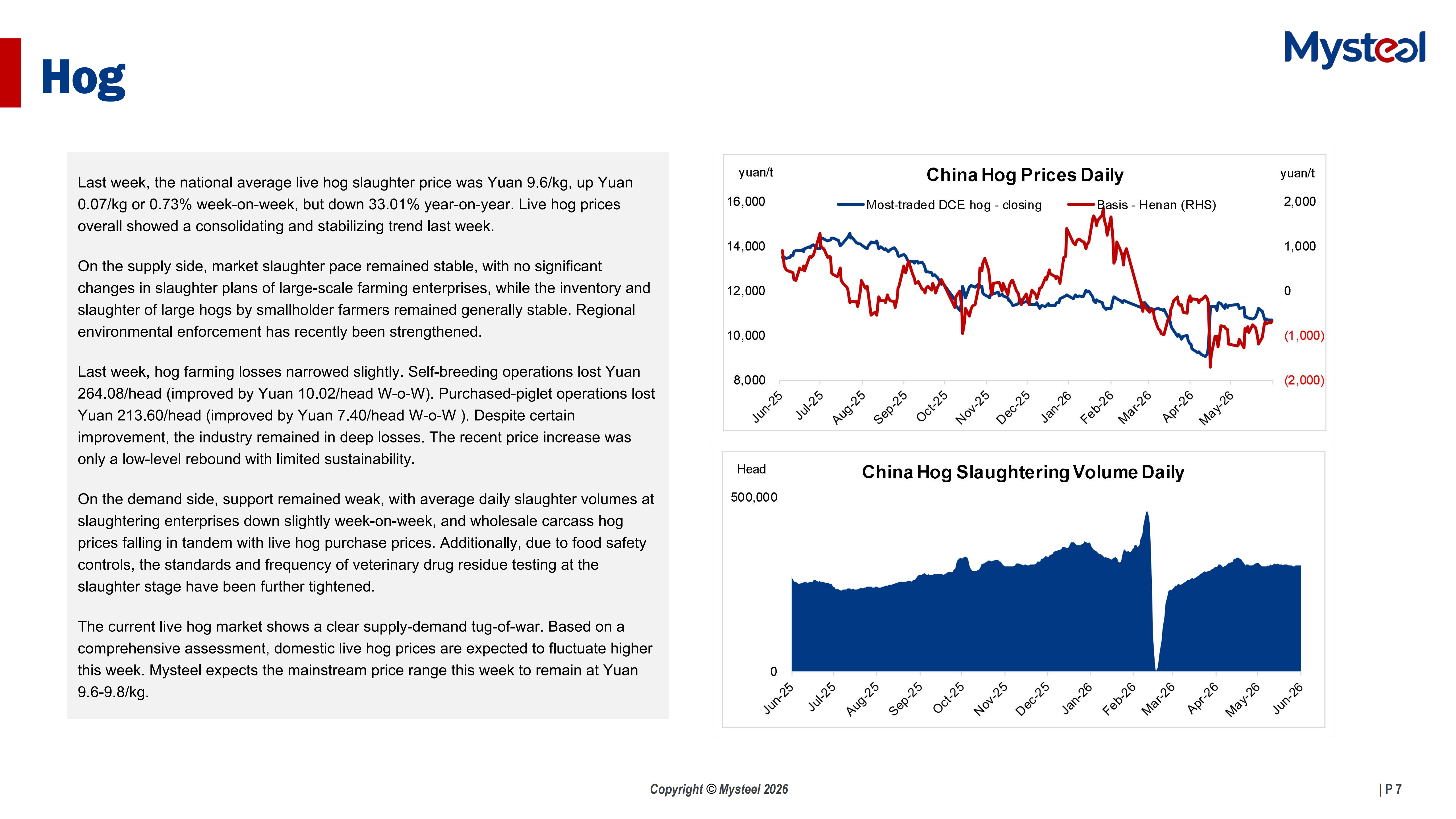

Hog: Hog prices stabilized and slightly moved up to Yuan 9.6/kg, but remained 33% below last year, with supply stable and tighter environmental enforcement. Farming losses slightly narrowed, but the industry is still deep in the red, demand is weak, and the recent rebound has limited sustainability. Yet, a small upside move is still expected this week.

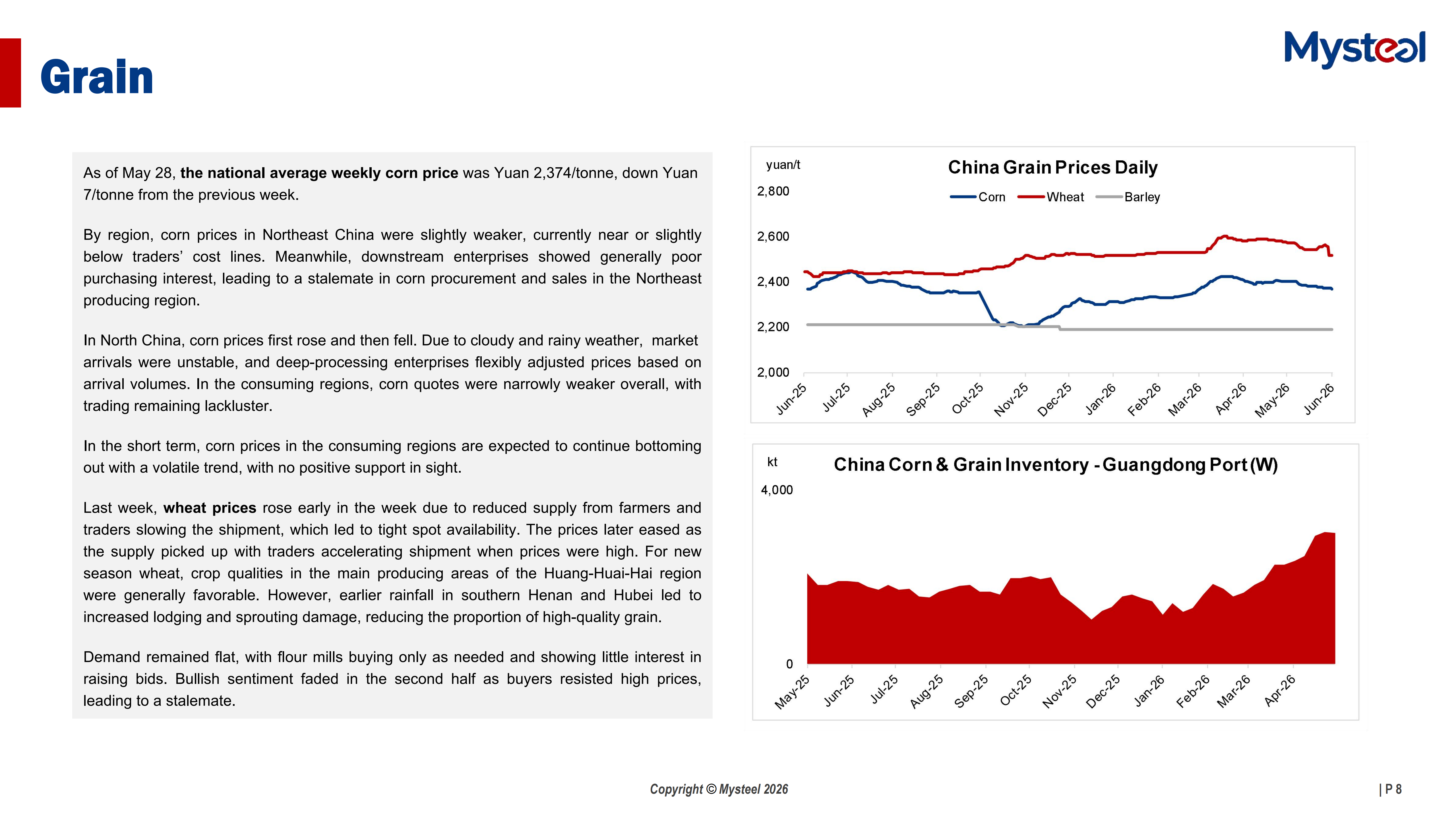

Grain: The national corn average price pulled back to Yuan 2,374/tonne, down Yuan 7/tonne. In detail, prices in Northeast China were near traders' cost lines, while those in North China rose first then fell on unstable arrivals. In consumer regions, trading remained slow and the market is expected to stay weak with no near-term support.

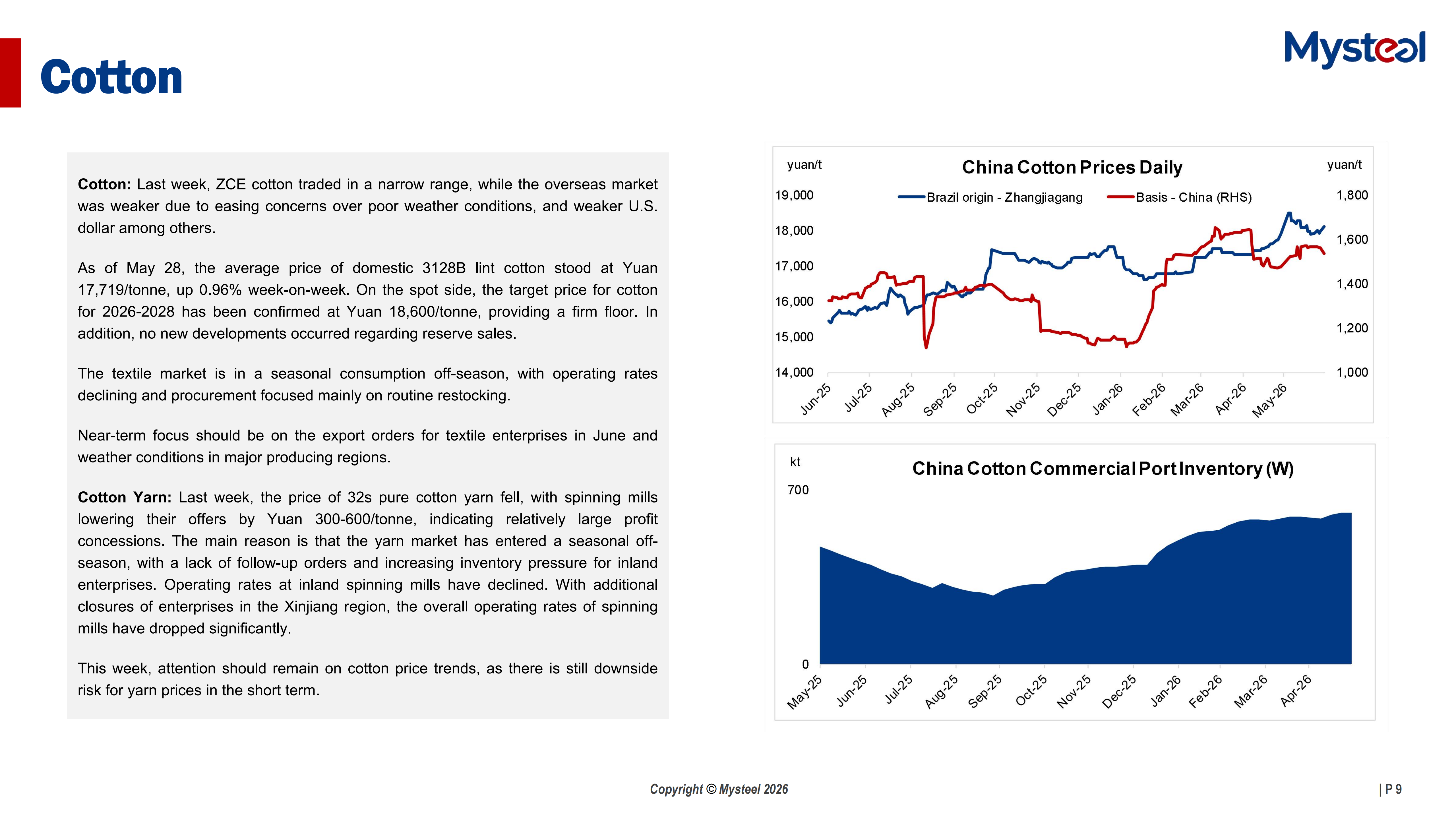

Cotton: ZCE cotton price traded in a narrow range last week while overseas markets were softer, with the newly confirmed 2026-2028 target price of Yuan 18,600/tonne providing a floor. The textile sector is in a seasonal slowdown, with operating rates falling and buying limited to routine restocking.