Since late 2025, the widening copper-aluminum price gap has renewed market interest in replacing copper with aluminum. Rising raw material costs have prompted manufacturers to accelerate the search for lower-cost alternatives, particularly in copper-intensive sectors such as power grids and air conditioning. While higher copper prices have strengthened the economic case for substitution, adoption varies across end-use sectors and remains constrained by technical requirements, industry standards and production capacity. Overall, aluminum substitution is still in the early stage of structural replacement, and is unlikely to materially alter copper's supply-demand balance in the foreseeable future.

Data Source: SHFE, Mysteel

Power grid: substitution confined to specific applications with copper dominating

Within the power grid sector, aluminum substitution occurs to varying degrees across four segments: transmission, distribution, new energy generation, and transformation equipment.

In the transmission sector, aluminum's penetration in high-voltage overhead lines is nearly saturated, as aluminum conductors already account for over 90% of new lines, indicating peak penetration. Future demand growth in this segment will mainly come from expanding ultra-high-voltage projects rather than replacing existing copper applications.

Regarding distribution, medium-voltage networks (10kV and above) rigidly require copper, whereas low-voltage networks (1kV and below) constitute the core battleground for aluminum substitution. Aluminum alloy cables already account for 45% of State Grid procurement in 2025 and are expected to exceed 50% during the 15th Five-Year Plan period (2026-2030). However, the existing installed base penetration remains extremely low. Mysteel estimates the volume of aluminum-for-copper substitution in 1kV low-voltage distribution at around 80,000 tonnes for 2025, indicating that a meaningful impact will take years to become visible.

On the new energy generation side, photovoltaic direct-current combiner cables and alternating-current low-voltage cables represent the primary applications for aluminum alloy cables. Downstream companies report that aluminum alloy cables already cover approximately 60% of these applications, although copper-core cables remain dominant for inter-module connections and control communication wiring that require high heat resistance.

As for transformation equipment, aluminum winding face narrow application scenarios due to physical shortcomings in conductivity and heat resistance. The core power supply system remains copper-wound, making it difficult to generate large-scale copper displacement demand.

Overall, aluminum substitution in the power grid sector is a targeted effort limited to niche applications rather than a broad shift away from copper. Over the medium to long term, copper is expected to remain the primary conductor, with aluminum only as supplements.

Air conditioning: strong economic incentive but slow commercialization

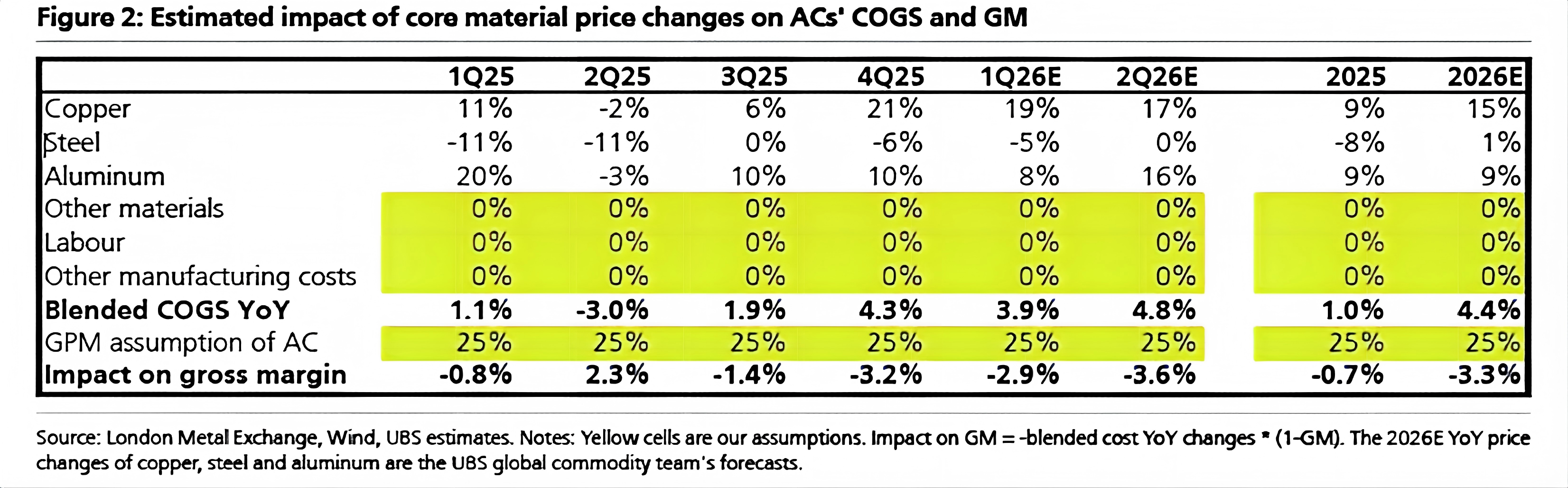

In the air-conditioning sector, driven by rising raw material costs, primarily copper, the comprehensive cost increased by about 4-5% year on year in Q4 2025 and the first half of 2026, with gross margins shrinking by 3-4 percentage points, according to United Bank of Switzerland (UBS)'s estimates. Given that the industry's net margin typically ranges from 3% to 5%, this cost shock has hit the breakeven line for most manufacturers, creating urgency to implement aluminum-for-copper substitution.

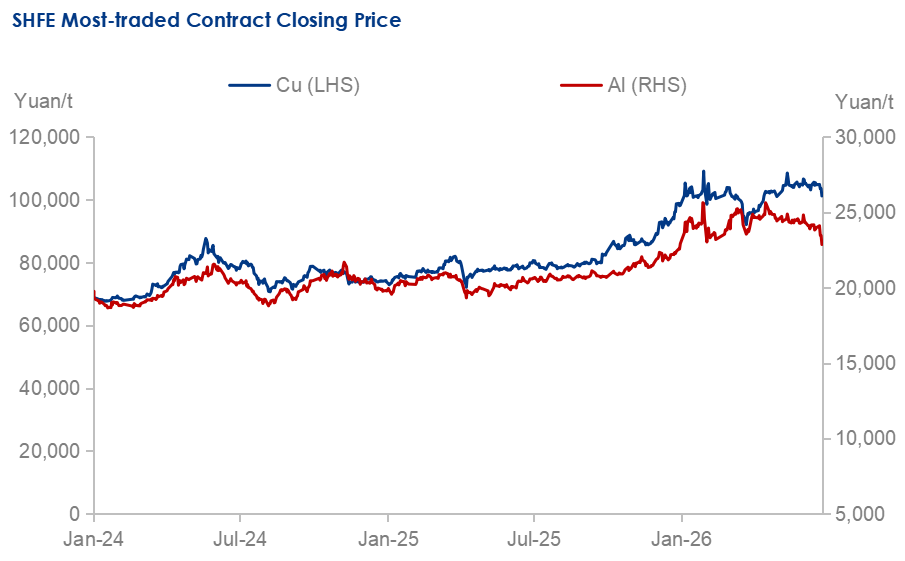

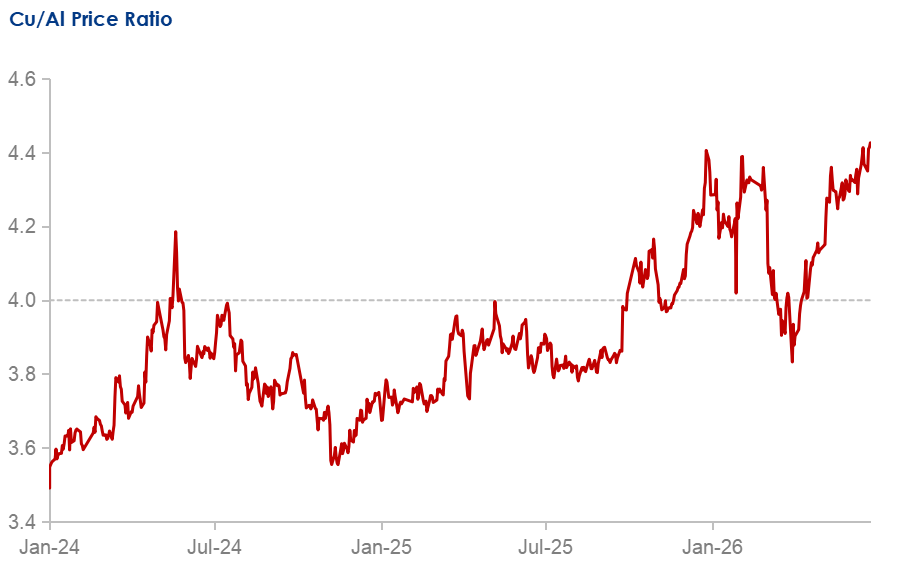

According to industry practice, when the copper-aluminum price ratio exceeds 3.5, the economic viability of substituting aluminum for copper begins to emerge. Once the ratio stabilizes above 4.0, substitution can deliver cost savings of approximately Yuan 105/unit, prompting upstream tube processors and downstream air-conditioner manufacturers to transform production lines and develop aluminum components. According to Mysteel, as of 25 June 2026, China's copper-aluminum price ratio had surged to 4.43, well above the historical average and central range.

Data Source: Mysteel

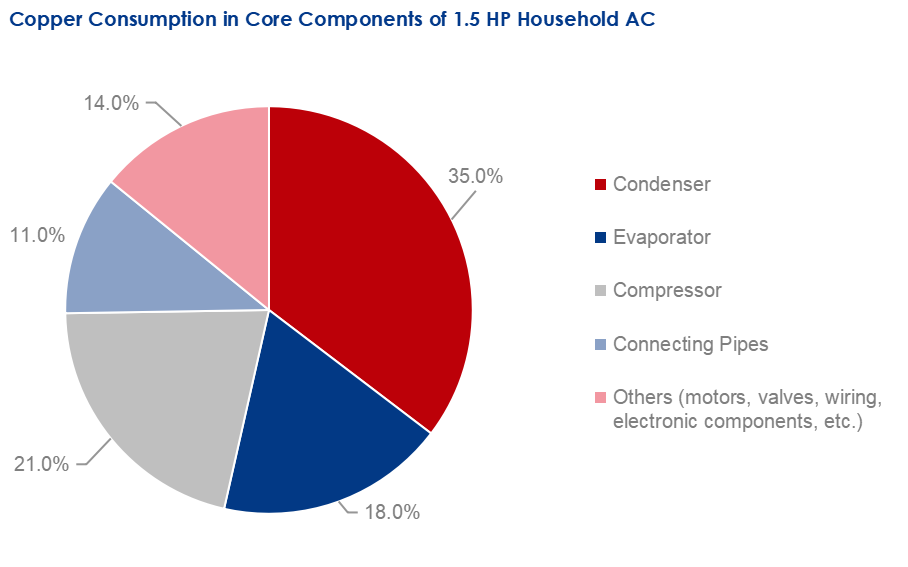

Based on Mysteel's measurements, a standard 1.5-horsepower split household air conditioner contains 7-12 kg of copper, with copper accounting for 25-29% of total material costs, and the heat exchanger (condenser and evaporator) represents 53% of the unit's total copper consumption. Advances in aluminum tube-fin designs, microchannel flat tubes, and anti-corrosion coatings have largely addressed aluminum's performance limitations, positioning heat exchangers as the most promising area for future substitution. Globally, aluminum heat exchangers have achieved penetration rates of around 40-50% among manufacturers in the U.S. and Japan. In contrast, China's market remains in the pilot stage, with large-scale adoption still below 10%.

Data Source: Mysteel

At present, aluminum-for-copper substitution in the air-conditioning industry follows a dual-material approach, with copper and aluminum coexisting and overseas manufacturers leading commercialization. Large-scale adoption in China is primarily hindered by aluminum's performance limitations, low domestic consumer acceptance, and insufficient upstream aluminum tube capacity. As a result, substitution is largely confined to low-end products and selected export markets, while high-end models remain predominantly all-copper.

Looking ahead, the development of aluminum-for-copper substitution in China's air-conditioning industry is expected to follow a gradual path rather than a rapid transformation, with limited impact on the copper market.

Between 2025 and 2027, the penetration rate of aluminum-for-copper substitution is expected to rise only to around 15-20%, as the construction of new production lines take time. An annual copper consumption reduction is estimated at 40,000-70,000 tonnes, less than 0.4% of China's annual copper consumption in 2025, with negligible impact on market fundamentals.

As production capacity expands and supporting technologies mature, substitution could accelerate during 2028-2030, although the reduction in copper demand would still be insufficient to offset consumption growth from electrification, renewable energy and AI-related infrastructure. By 2030, the penetration rate of aluminum heat exchangers in China's domestic complete units could reach 30-40%. This phase corresponds to an expected annual copper consumption reduction of 170,000-290,000 tonnes.

Even by 2035, when penetration may approach 50-60%, the corresponding reduction in copper demand is expected to account for only around 1.5-2.2% of China's annual copper consumption.

Conclusion

In summary, aluminum-for-copper substitution is emerging as an important structural trend, but its impact on copper demand is likely to remain gradual and manageable. In the power grid sector, substitution has largely been confined to niche applications, while in air conditioning, despite strong cost incentives under the current copper-aluminum price ratio, widespread adoption will depend on continued improvements in technology, consumer acceptance, and production capacity. Consequently, aluminum is expected to complement rather than replace copper over the coming decade. While substitution may gradually weigh on copper demand after 2028, the scale is unlikely to offset incremental consumption driven by electrification, renewable energy, and AI-related infrastructure, leaving the long-term fundamentals of the copper market largely intact.

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com