Copper prices continued increasing in futures and spot markets on June 29, as the falling U.S. dollar index supported prices. The U.S. Department of Commerce is required to submit an updated report on the U.S. copper market to President Trump by June 30, 2026, for his assessment of whether adjustments to Section 232 tariffs are necessary. However, no clear timeline has been set for when the tariff decision will be announced, leaving significant market uncertainty at present.

China's refined copper spot trading declined on June 29 due to persistently rising copper prices, sluggish downstream demand amid the demand off-season, and the month-end and half-year-end settlement tightening funds. Spot premiums generally dropped across major markets in China, staying at low levels.

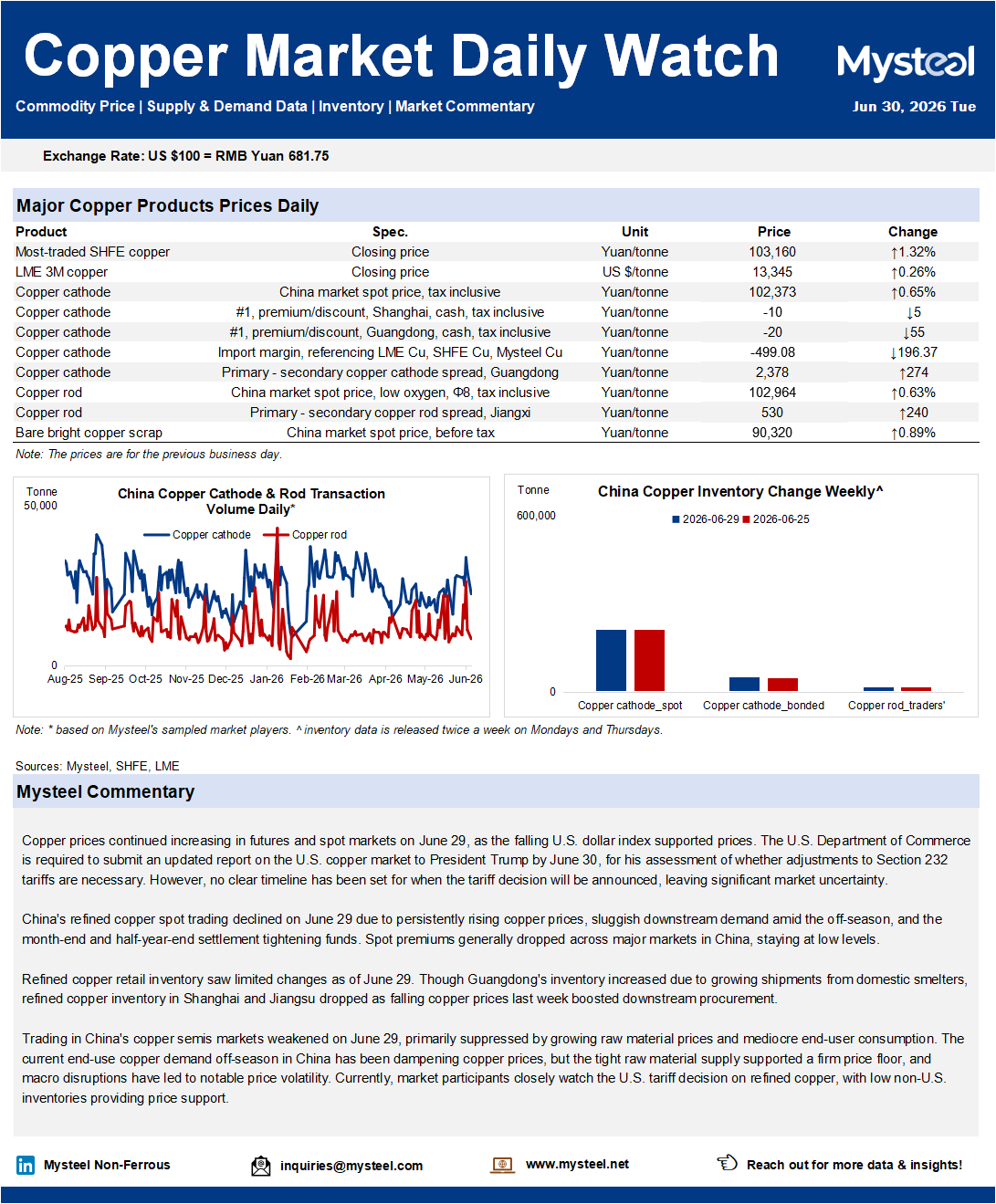

Refined copper retail inventory saw limited changes as of June 29. Though Guangdong's inventory increased due to growing shipments from domestic smelters, refined copper inventory in Shanghai and Jiangsu dropped as falling copper prices last week boosted downstream procurement.

Trading in China's copper semis markets weakened on June 29, primarily suppressed by growing raw material prices and mediocre end-user consumption. The current end-use copper demand off-season in China has been dampening copper prices, but the tight raw material supply supported a firm price floor, and macro disruptions have led to notable price volatility. Currently, market participants closely watch the U.S. tariff decision on refined copper, with low non-U.S. inventories providing price support.