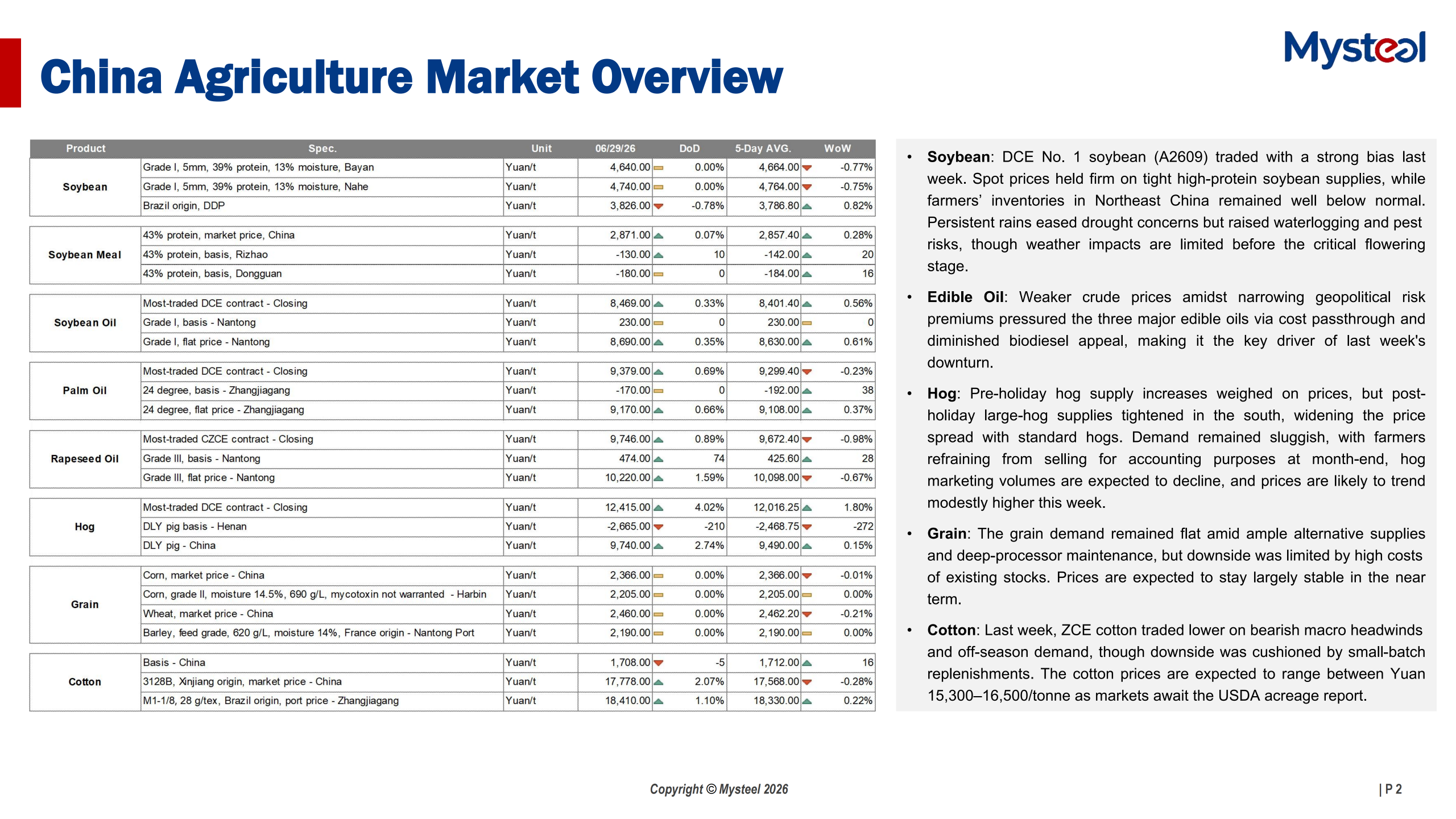

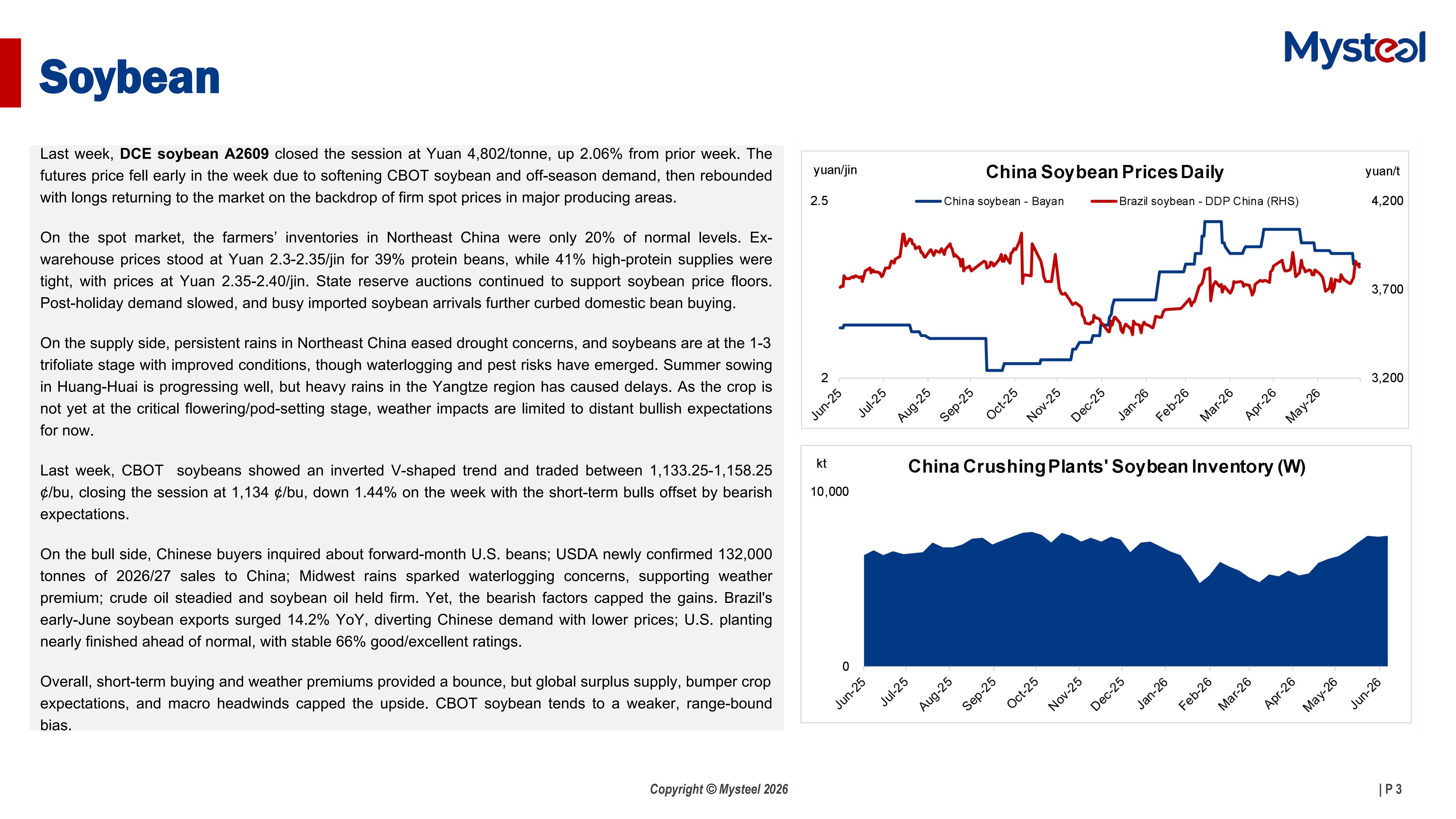

Soybean: DCE No. 1 soybean (A2609) traded with a strong bias last week. Spot prices held firm on tight high-protein soybean supplies, while farmers' inventories in Northeast China remained well below normal. Persistent rains eased drought concerns but raised waterlogging and pest risks, though weather impacts are limited before the critical flowering stage.

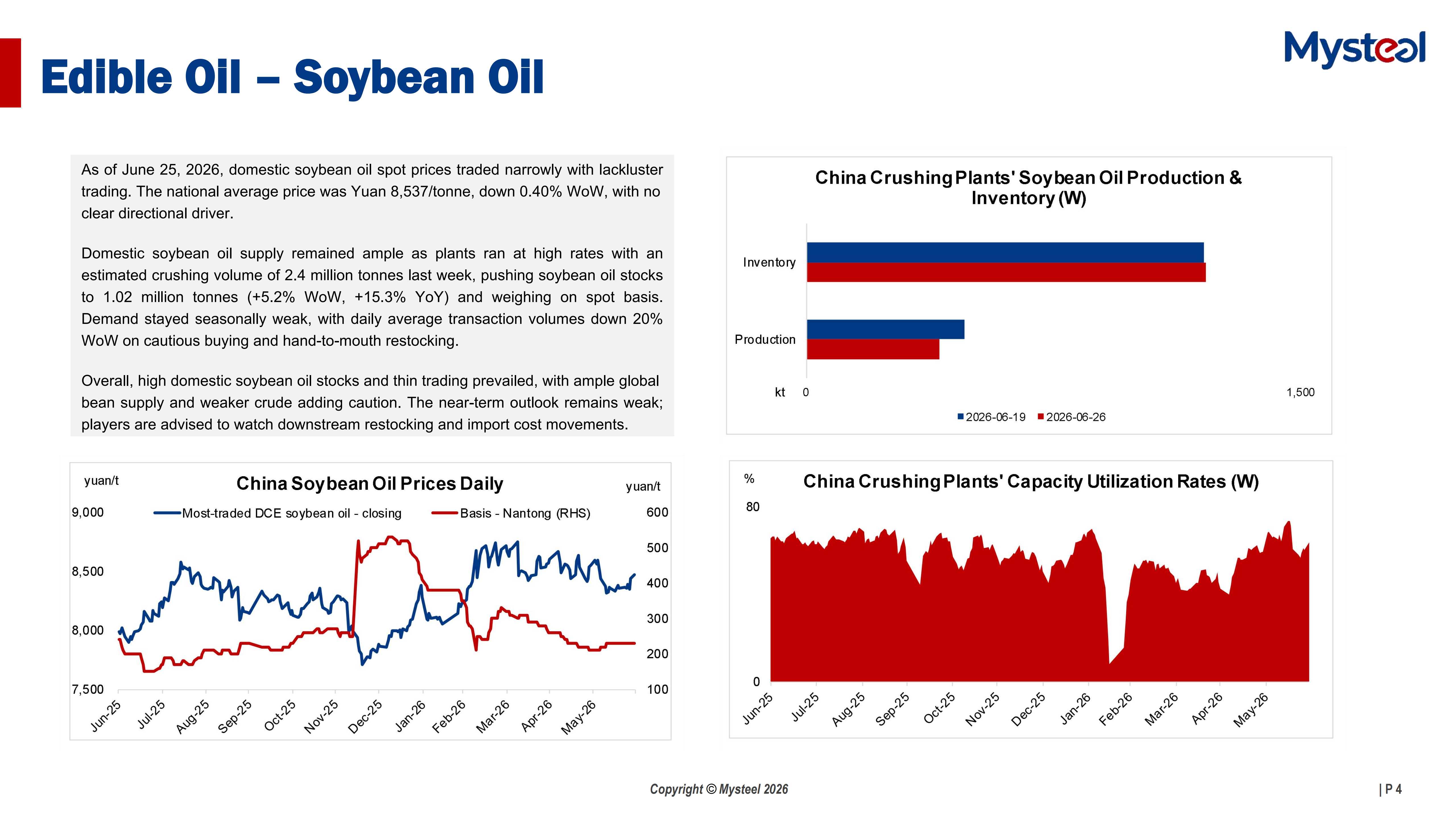

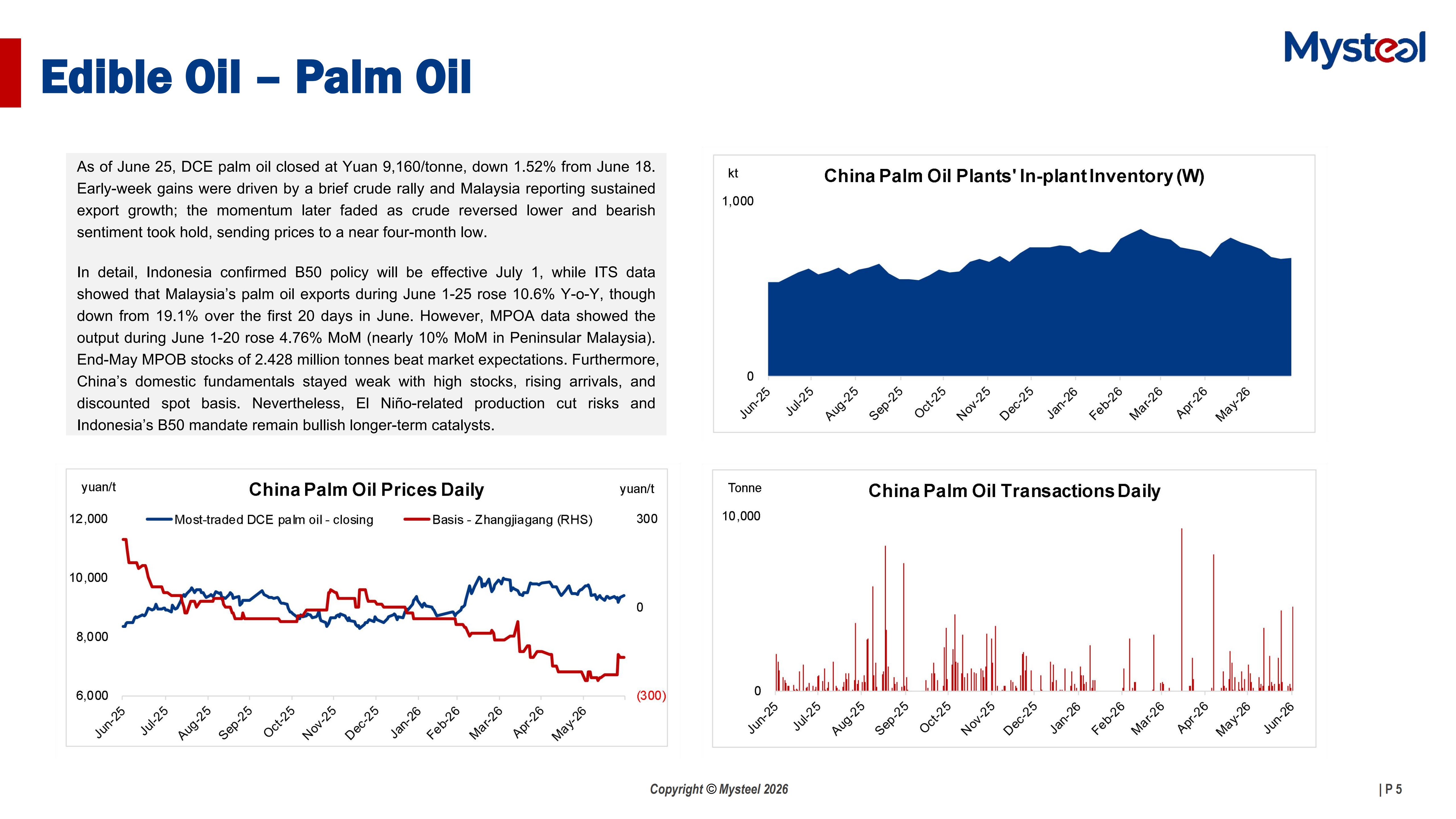

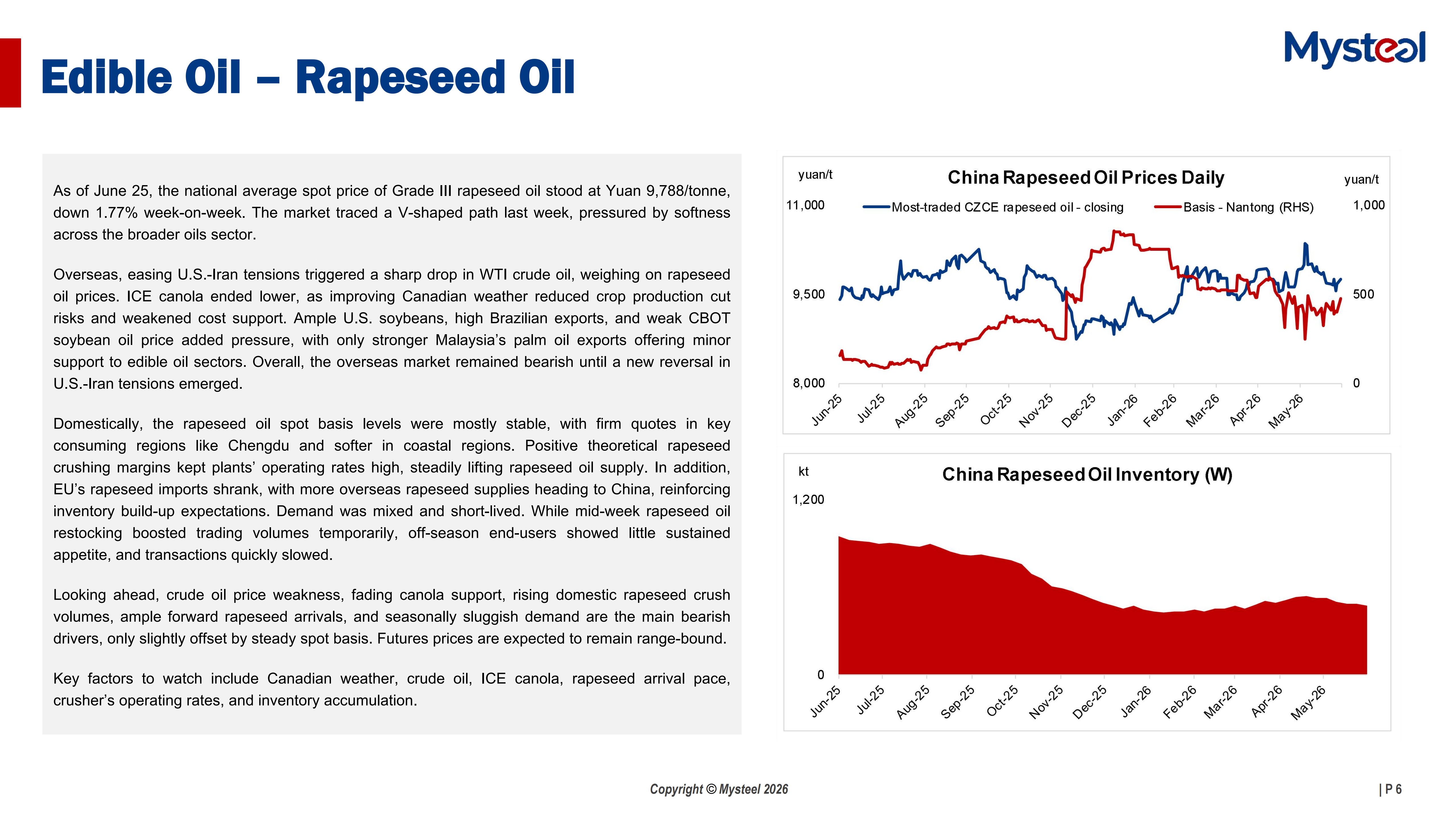

Edible Oil: Weaker crude prices amidst narrowing geopolitical risk premiums pressured the three major edible oils via cost passthrough and diminished biodiesel appeal, making it the key driver of last week's downturn.

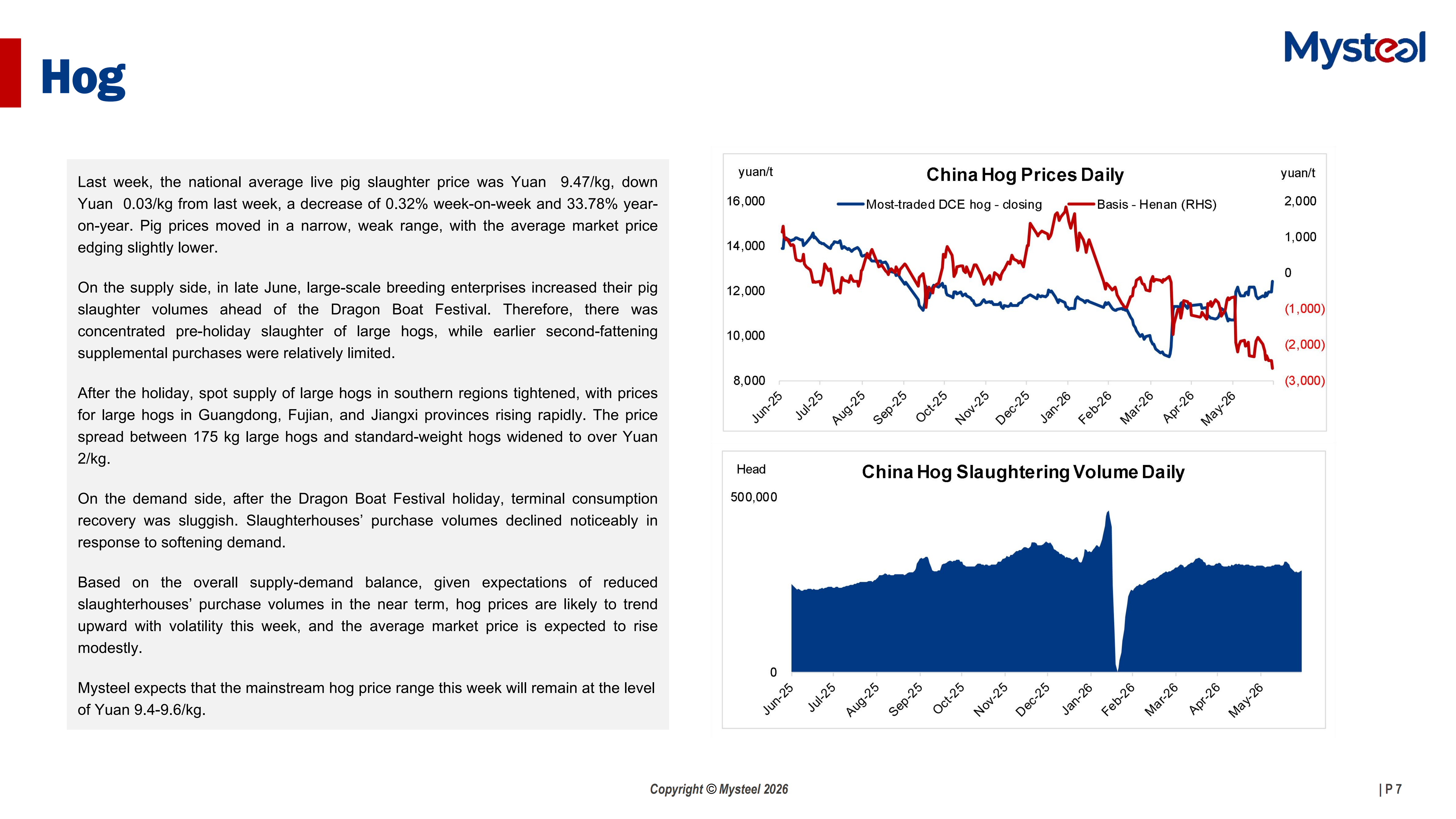

Hog: Pre-holiday hog supply increases weighed on prices, but post-holiday large-hog supplies tightened in the south, widening the price spread with standard hogs. Demand remained sluggish, with farmers refraining from selling for accounting purposes at month-end, hog marketing volumes are expected to decline, and prices are likely to trend modestly higher this week.

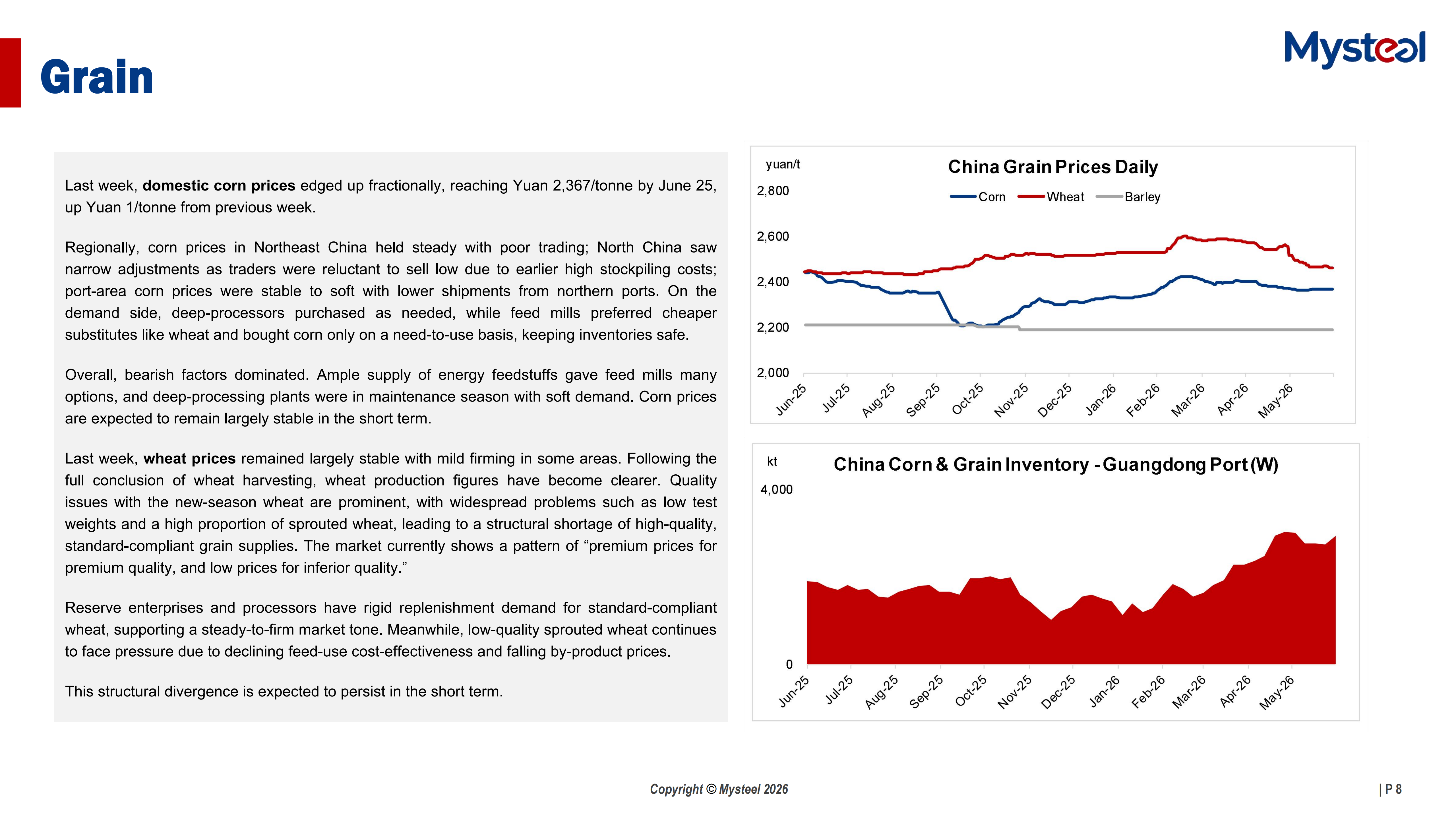

Grain: The grain demand remained flat amid ample alternative supplies and deep-processor maintenance, but downside was limited by high costs of existing stocks. Prices are expected to stay largely stable in the near term.

Cotton: Last week, ZCE cotton traded lower on bearish macro headwinds and off-season demand, though downside was cushioned by small-batch replenishments. The cotton prices are expected to range between Yuan 15,300–16,500/tonne as markets await the USDA acreage report.