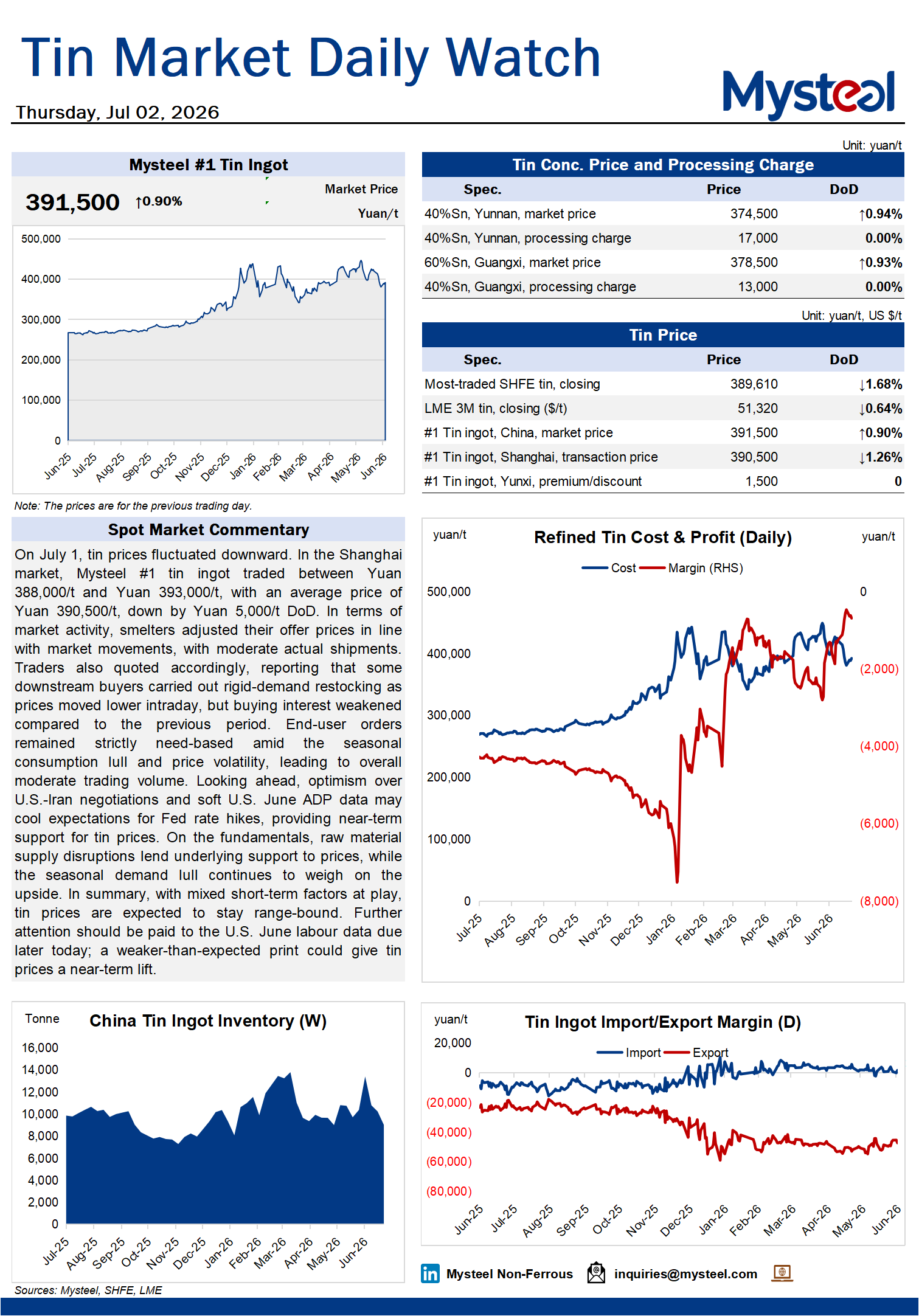

On July 1, tin prices fluctuated downward. In the Shanghai market, Mysteel #1 tin ingot traded between Yuan 388,000/t and Yuan 393,000/t, with an average price of Yuan 390,500/t, down by Yuan 5,000/t DoD. In terms of market activity, smelters adjusted their offer prices in line with market movements, with moderate actual shipments. Traders also quoted accordingly, reporting that some downstream buyers carried out rigid-demand restocking as prices moved lower intraday, but buying interest weakened compared to the previous period. End-user orders remained strictly need-based amid the seasonal consumption lull and price volatility, leading to overall moderate trading volume. Looking ahead, optimism over U.S.-Iran negotiations and soft U.S. June ADP data may cool expectations for Fed rate hikes, providing near-term support for tin prices. On the fundamentals, raw material supply disruptions lend underlying support to prices, while the seasonal demand lull continues to weigh on the upside. In summary, with mixed short-term factors at play, tin prices are expected to stay range-bound. Further attention should be paid to the U.S. June labour data due later today; a weaker-than-expected print could give tin prices a near-term lift.