On June 29, 2026, the Shanghai Futures Exchange (SHFE) issued an announcement approving the registration of the "HUAYOU" brand electrolytic nickel (electro-winning process, Ni99.96) produced by Quzhou Huayou Cobalt New Material Co., Ltd. for Phase III, with a registered production capacity of 50,000 tonnes per year, at the standard price. Effective from the date of the announcement, the product was eligible for physical delivery against SHFE nickel futures contracts.

With this approval, the total registered refined nickel capacity of Quzhou Huayou on the SHFE reached 86,000 tonnes per year (Phase I: 6,000 tonnes, Phase II: 30,000 tonnes, Phase III: 50,000 tonnes). Combined with Guangxi Huayou's registered capacity of 30,000 tonnes per year, Huayou Cobalt's total registered capacity on the SHFE reached 116,000 tonnes per year.

I. Review of SHFE nickel deliverable brands

In recent years, SHFE's deliverable nickel brands have expanded from a handful of domestic brands such as Jinchuan, Jien, and Bofeng, together with imported Russian nickel, to include multiple brands such as Huayou (with facilities in several locations), GEM, and CNGR. In April 2026, the SHFE also approved the registration of two brands produced by Chinese-invested enterprises in Indonesia (PTENICO and DX-zwdx), marking the official opening of China's futures delivery channel for Indonesian nickel products. The diversification of deliverable brands helped improve market liquidity and reduce the risk of concentration in a single brand.

II. Current status of refined nickel capacity and production in China

According to Mysteel's survey of 22 sampled enterprises in China, refined nickel production in May 2026 stood at 33,800 tonnes, with June output estimated at 33,500 tonnes. Current equipment capacity across domestic nickel enterprises was 52,100 tonnes per month, with a capacity utilisation rate of 64.82%.

Source: Mysteel

By enterprise, the established producer Jinchuan Group still accounted for the bulk of domestic refined nickel production. Brands that had already obtained registration, including Huayou, CNGR, and GEM, continued to maintain production schedules, although raw material supply was tight, leading to varying degrees of production cuts across enterprises of all sizes. In addition, newly commissioned producers such as Weiming Shengqing, Hanrui Cobalt, and Zhejiang Jutai were still in the process of ramping up production and were also applying for delivery qualifications.

In the second half of the year, three more enterprises planned to bring electro-deposited nickel capacity online: the Guangdong-based new energy company Meizhida, Greatpower Guangxi, and Cash Jinqiao, which had relocated from Yantai to Lianyungang.

In addition, refined nickel projects in Indonesia had also commenced production one after another. Despite tight raw material supply, the PTENICO and DX-zwdx projects, both of which held delivery qualifications on both the SHFE and LME, were able to secure as ample raw material supply as possible.

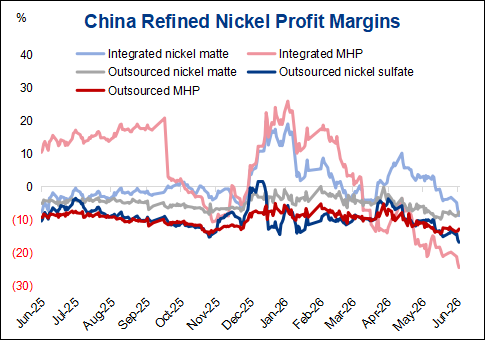

From the perspective of production profitability, due to tight supply and high prices of raw and auxiliary materials (nickel ore, sulfur, etc.), current refined nickel production was loss-making on a spot basis, regardless of whether producers used externally sourced feedstocks or integrated production. Producers were striving to maintain operations by combining different feedstocks, selling by-products, and hedging.

Source: Mysteel

III. Global nickel inventories approaching historic highs

According to Mysteel data as of June 26, refined nickel inventories at 27 warehouses in China stood at 119,100 tonnes, of which warrant stocks accounted for 97,100 tonnes, spot inventory 18,700 tonnes, and bonded zone inventory 3,300 tonnes. LME nickel inventories were also at high levels, with LME registered warrant stocks at 274,800 tonnes and non-registered warrants at 95,900 tonnes. Total observable global inventories were approaching 500,000 tonnes.

Persistent inventory accumulation remained the core factor weighing on nickel prices. The latest Huayou registration was unlikely to cause a sharp increase in warrant stocks in the short term, as remaining capacity at mainstream domestic delivery warehouses was already limited. In addition, Quzhou Huayou had not been producing at full capacity in recent months due to tight raw material supply, with monthly production remaining around 1,000 tonnes.

In terms of trends, Chinese nickel inventories showed a pattern of accumulation followed by decline over the past month. On June 12, the 27-warehouse inventory rose 4.59% week-on-week; in the week of June 22, inventory fell 1.48% to 120,600 tonnes; and in the final week of June, it fell another 1.25% to 119,100 tonnes. Although inventories had drawn down for two consecutive weeks, the absolute level remained high, and effective spot buying interest was absent during price declines.

IV. Summary and outlook

With the registration of Phase III of Quzhou Huayou's 50,000-tonne capacity, the total registered refined nickel capacity of Chinese-invested enterprises on the SHFE had exceeded 200,000 tonnes per year, including brands produced in Indonesia. At the same time, Weiming Shengqing (capacity 50,000 tonnes/year) and Zhejiang Jutai (capacity 35,000 tonnes/year) were actively applying for SHFE delivery qualifications. As more domestic nickel capacity was brought online, deliverable resources for nickel futures were expected to become increasingly ample.

From a supply-demand perspective, China's refined nickel capacity utilisation rate remained at only about 64%, far from full capacity. However, high inventories remained stuck at elevated levels, with global inventories approaching 500,000 tonnes, and consumption pressures persisted. The registration of Huayou Phase III represented an "expansion of deliverable brands" rather than an "incremental output" increase -- the actual deliverable volume would depend on each enterprise's production scheduling. In the short term, warrant pressure was limited. Over the medium to longer term, as refined nickel output from enterprises gradually increased, deliverable resources on SHFE nickel futures would become more abundant, and the correlation between domestic and overseas markets was expected to strengthen. China's influence in the global nickel pricing system would continue to rise.

Written by Cora Ji, jiruyan@mysteel.com