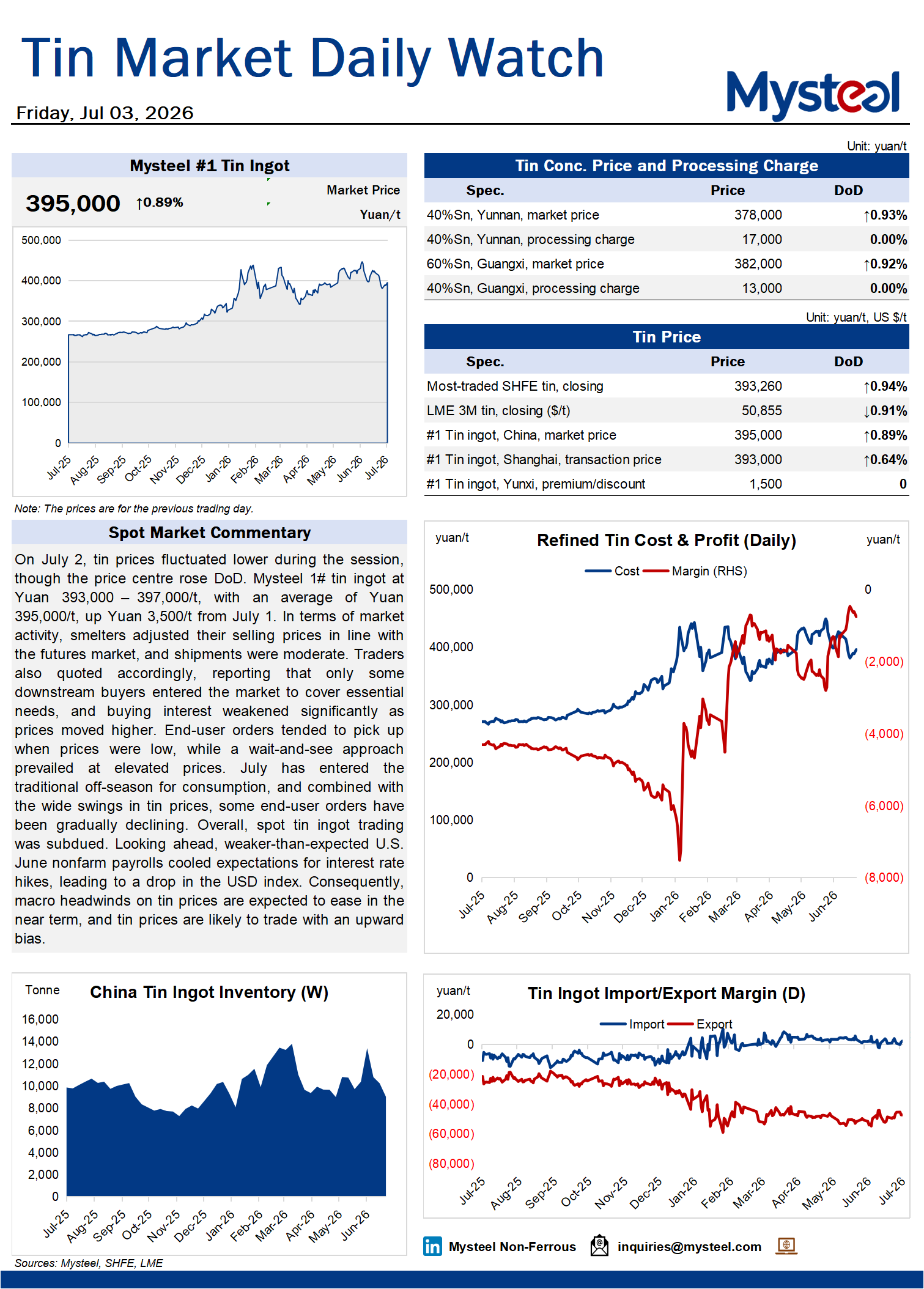

On July 2, tin prices fluctuated lower during the session, though the price centre rose DoD. Mysteel 1# tin ingot at Yuan 393,000–397,000/t, with an average of Yuan 395,000/t, up Yuan 3,500/t from July 1. In terms of market activity, smelters adjusted their selling prices in line with the futures market, and shipments were moderate. Traders also quoted accordingly, reporting that only some downstream buyers entered the market to cover essential needs, and buying interest weakened significantly as prices moved higher. End-user orders tended to pick up when prices were low, while a wait-and-see approach prevailed at elevated prices. July has entered the traditional off-season for consumption, and combined with the wide swings in tin prices, some end-user orders have been gradually declining. Overall, spot tin ingot trading was subdued. Looking ahead, weaker-than-expected U.S. June nonfarm payrolls cooled expectations for interest rate hikes, leading to a drop in the USD index. Consequently, macro headwinds on tin prices are expected to ease in the near term, and tin prices are likely to trade with an upward bias.