In the first half (H1) of 2026, China's copper concentrate market faced unprecedented tightness, with treatment and refining charges (TC/RCs) plunging deeply negative. The collapse in TC/RCs is not merely a temporary market disturbance, but reflects a deeper structural imbalance between sluggish global mine supply growth and continued expansion of copper smelting capacity. It has begun spreading downstream, reshaping smelter profitability, accelerating reliance on by-product revenues, and forcing production adjustments that could eventually constrain subsequent refined copper supply in China.

TC/RC: Record plunge pushes smelters to lean on by-product profits

The decline in copper concentrate TC/RCs reached historic levels in H1 2026, breaking the market's previous perception of a TC floor. In the 2026 annual copper concentrate long-term contract negotiations, the benchmark TC/RC was set at $0/dmt and 0¢/lb for the first time, far below levels for smelters to maintain profits. Meanwhile, spot TC/RCs stayed deeply negative, worsening smelters' losses. The monthly average TC for 25% clean copper concentrate tracked by Mysteel fell from -$46.78/dmt in January to -$120.03/dmt in June, and further dropped to -$127.2/dmt in early July, representing a total decline of over $70/dmt within six months.

Data Source: Mysteel

Though the persistence of deeply negative TC/RCs was primarily supported by tight copper concentrate supply, strong smelting by-product revenues, particularly sulfuric acid, also made contributions. As the industry has entered a new profit structure where core smelting operations run at a loss, while by-product revenues support overall smelting profitability, copper concentrate traders tended to further lower TC/RCs to share such profits.

Data Source: Mysteel

Supply: Global mine supply disruptions lead to China's concentrate tightness

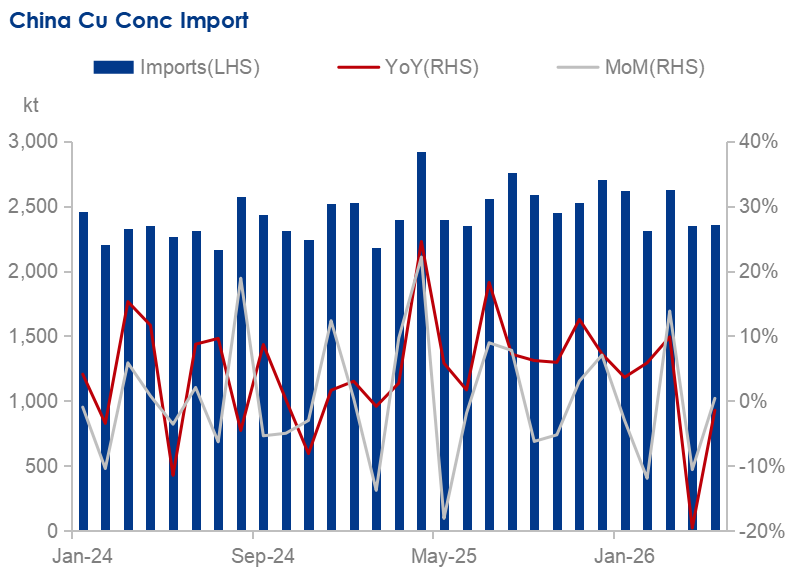

China's copper concentrate market remains highly dependent on overseas supply, with imports accounting for around 80% of consumption. Therefore, the current shortage is essentially a reflection of tightening global mine supply. From January to May 2026, China's cumulative imports of copper ore and concentrate reached 12.28 million tonnes, down by 1.2% year on year, marking the first year-on-year decline in the past five years, according to China's General Administration of Customs (GACC). The decline was not caused by weaker domestic demand, but by reduced availability of global supply.

Overall, copper concentrate output reductions in major producing countries were the core drag on global supply. Chile, the world's top copper concentrate producer, reported May output of only 423,623 tonnes, down by 12.9% year on year, while its cumulative output in the first five months of 2026 reached 2.0374 million tonnes, 8.83% lower than the same period in 2025. In its May forecast, Chile's National Copper Corporation (Cochilco) projected that the country's 2026 full-year copper production would fall 2% year on year to 5.3 million tonnes, constrained by persistently declining ore grades, scheduled equipment maintenance and weak performance at the start of the year.

Meanwhile, Indonesia's Grasberg mine, a leading global source of high-grade copper concentrate, suffered a sharp output decline following an underground accident in September 2025. Mine owner Freeport-McMoRan reported a 24% year-on-year decline in copper concentrate output in Q1 2026 and lowered its 2026 production guidance to 1,451,000 tonnes, compared with 1,535,000 tonnes of actual output in 2025.

Additionally, Ivanhoe lowered the 2026 production target for its Kamoa-Kakula mine from 380,000-420,000 tonnes to 290,000-330,000 tonnes due to the prioritization of underground development work and slower-than-expected ramp-up. Other miners including Anglo American, Glencore and Southern Copper also revised down their production expectations, citing constraints such as declining ore grades, tailings facility limits and water supply shortages.

The International Copper Study Group (ICSG) also revised down its 2026 global copper mine supply growth forecast to 1.6% from 2.3% previously, leaving limited room for additional concentrate availability.

Disruptions on mine operations also reshaped China's import structure. According to GACC, from January to May, China's copper concentrate imports from Chile and Peru declined by 5.31% and 4.43% year on year, respectively, while imports from Mongolia increased by 30.33% as smelters sought alternative sources.

At the same time, rising pyrite imports into China provided another indication of copper concentrate tightness. China's pyrite imports reached approximately 677,100 tonnes during the first five months of 2026, up by 32.8% year on year, as smelters turned to alternative sulfur-bearing materials to maintain operations and reduce reliance on expensive copper concentrate.

Data Source: Mysteel, GACC

Demand: Profit decline slows smelter output growth

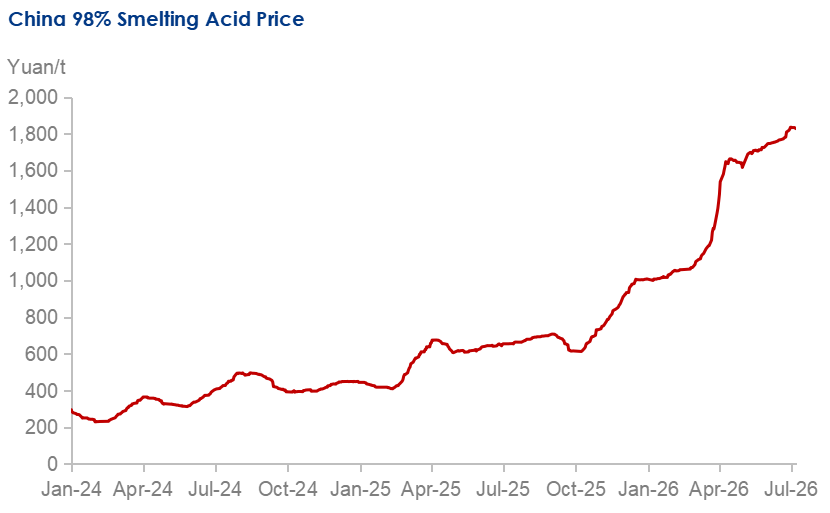

The unprecedented collapse in TC/RCs indicates that copper smelting has entered a phase where the traditional profit model based on TCs has broken down. Since copper smelting generates around 3-4 tonnes of sulfuric acid per tonne of refined copper produced, strong acid prices have temporarily offset losses from negative TC/RCs. Domestic smelting acid prices tracked by Mysteel rose from Yuan 1,015/tonne at the beginning of 2026 to Yuan 1,768/tonne in June, up by 74.14%, and remained elevated at Yuan 1,828/tonne as of July 9. Consequently, smelters are no longer earning returns from producing copper and must increasingly rely on sulfuric acid, precious metals and other by-products to maintain profitability.

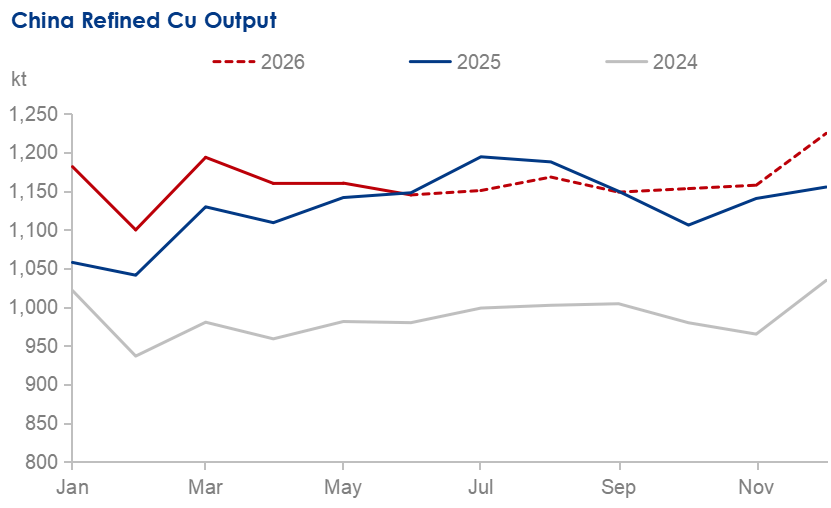

Refined copper output growth dropped in China. According to Mysteel's survey of 60 major refined copper producers, China produced 6.9408 million tonnes of refined copper in H1 2026, up 4.73% year on year, significantly lower than the 12.3% growth recorded in 2025. However, the adjustment has been uneven across the industry. Large smelters with stronger long-term contract coverage and better by-product recovery systems maintained relatively stable production. In contrast, small and medium-sized smelters with greater exposure to spot concentrate purchases faced mounting pressure, with capacity utilization among smelters whose monthly capacity stay below 100,000 tonnes declining by 13.07 percentage points year on year. Consequently, overall maintenance also increased in H1 2026. Mysteel's data showed that smelter maintenance in Q2 2026 affected around 179,000 tonnes of refined copper output, 89,000 tonnes more than the same period in 2025.

Data Source: Mysteel

Nevertheless, the slowdown in refined copper output growth does not represent an actual decline in copper concentrate demand. Copper consumption remains supported by growth in end-use areas including power grid investment, new energy vehicles, lithium battery copper foil and high-end AI-related copper foil demand. As a result, smelters' demand for concentrate remains fundamentally resilient.

Outlook: Concentrate tightness to persist and impact refined copper output

Looking ahead to H2 2026, the tight balance in China's copper concentrate market is unlikely to see a fundamental reversal, and the key question will be whether smelters can continue absorbing negative TC/RCs without triggering broader production adjustments.

On the supply side, global mine growth will remain limited, constrained by falling output at existing mines, slower-than-expected capacity recovery, limited new projects and delays in commissioning. Chile's copper concentrate production is not expected to return to stronger growth until 2027, while Grasberg is unlikely to fully recover capacity before early 2028. Consequently, China's copper concentrate imports are also unlikely to maintain strong growth in H2, despite the recent increase in port inventory, which mainly reflects temporarily slower procurement from smelters rather than a genuine improvement in supply.

On the demand side, refined copper output growth may slow further in China as smelters conduct concentrated maintenance from June to August. However, once maintenance ends, smelters are expected to return to the market for restocking, intensifying competition for limited concentrate supply. Mysteel estimates that the tightest raw material conditions may emerge between September and October, likely leading to a projected year-on-year growth of only around 1% in China's refined copper output for the full second half of 2026. Fluctuations in sulfuric acid and other by-product prices will become a key variable influencing smelters' production decisions. A sharp decline in sulfuric acid prices could quickly erode smelters' overall profitability and potentially trigger larger-scale proactive production cuts.

Overall, China's copper concentrate TC/RCs are expected to remain volatile at deeply negative levels throughout H2 2026, with limited potential for a sustained recovery. The market will continue to be defined by strong mining-side pricing power and increasingly fragile smelter economics. Therefore, the biggest market risk in H2 2026 is the possibility that the concentrate shortage may begin to impact refined copper supply growth in China.

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com