China's prebaked anode market navigated a turbulent first half of 2026, pivoting from a cost-driven slump to a geopolitical rally. While output climbed 8.34% YoY and demand stayed firm, prices ultimately tracked the erratic swings in petroleum coke and coal tar pitch. With new capacity set to ramp up against a backdrop of high aluminum operating rates, the market is poised for a balanced yet fluctuating second half, projected to trade within a range of Yuan 5,100–5,800/tonne

Review of prebaked anode price trends

In the first half of 2026, domestic prebaked anode prices exhibited an overall oscillating trend characterized by an initial decline, followed by a rally, and then a pullback. In June, the procurement price for prebaked anodes at major Shandong-based aluminum enterprises stood at Yuan 5,653/tonne, up Yuan 229/tonne from December 2025.

At the beginning of the year, raw material prices plummeted consecutively, leading to a collapse in cost-side support; consequently, anode prices fell continuously throughout Q1, with a cumulative drop of Yuan 250/tonne.

Entering March, turmoil in the Middle East geopolitical landscape triggered a sharp surge in international oil prices due to heightened supply risks. This drove widespread increases in crude oil and chemical product prices. Petroleum coke, as a by-product of crude oil refining, experienced significant price volatility in a short period due to supply chain transmission effects. Bolstered by strong cost-side support, prebaked anode prices finally rebounded at the start of Q2. In April, prices rose again for the first time in three months, surging by Yuan 300/tonne month-on-month. The market maintained its upward trajectory through May.

However, in June, influenced by declining feedstock prices during the settlement cycle, cost support weakened. The prebaked anode market quickly shifted from rising to falling, retreating slightly by Yuan 21/tonne to settle at Yuan 5,653/tonne.

Review of prebaked anode fundamentals

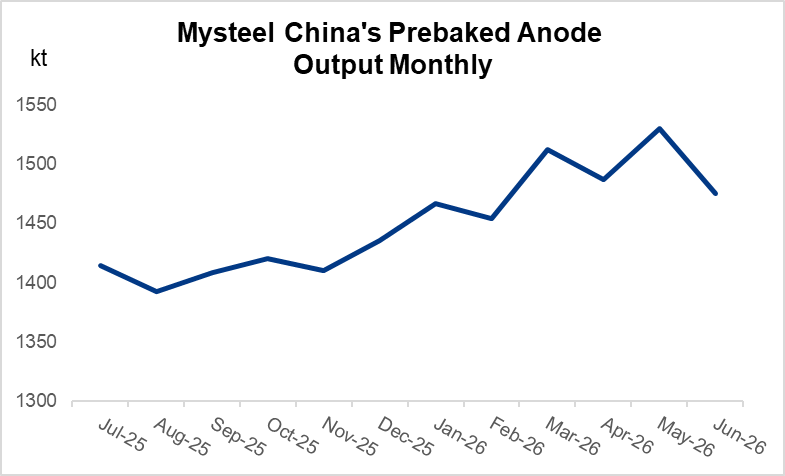

In H1 2026, the domestic prebaked anode industry maintained stable production with sufficient supply, as manufacturers primarily focused on fulfilling orders. Multiple new and upgraded capacity expansions were commissioned in Shandong, Henan, Inner Mongolia, Guangxi, and Yunnan, leading to a notable increase in output. While some enterprises in Northwest and Southwest China conducted scheduled production line upgrades, and certain regions faced output pressure due to environmental regulations, national production still rose significantly.

According to Mysteel's survey, China produced 12.47 million tonnes of prebaked anodes between January and June 2026, an increase of 8.34% year-on-year. Downstream aluminum smelters progressed steadily with new startups and restarts, maintaining high operating rates. Concurrently, overseas anode orders continued to rise, resulting in overall demand surpassing that of the previous year.

Source:Mysteel

Against the backdrop of growing supply and robust downstream demand, fluctuations in production costs remained the primary driver of anode pricing.

In Q1 of 2026, supply-demand imbalances in the raw materials market eroded cost support, leading to consecutive monthly price declines. Early in the quarter, some captive anode plants continued winter peak-load shifting production schedules. In North China, anode producers experienced slight reductions in operating loads during heavy pollution weather alerts, causing minor output contractions. Downstream, aluminum operating capacity remained relatively stable, with weekly output showing a steady, slight increase. Rising aluminum prices expanded profit margins, ensuring normal procurement rhythms for anodes.

On the export front, China exported 652,000 tonnes of prebaked anodes in Q1, up 11.89% YoY. Export destinations remained largely consistent, primarily Malaysia, Indonesia, the UAE, Canada, Norway, and Russia. Notably, exports to Indonesia surged, driven by the commissioning of new and planned smelting projects in the region, which boosted local anode consumption.

Cost-wise, the average price for 3B petroleum coke in mainstream regions was Yuan 3,092.71/tonne in Q1 (up Yuan 36.32/tonne from Q4 2025), while coal tar pitch averaged Yuan 4,866.95/tonne (up Yuan 951.38/tonne QoQ).

In Q2 of 2026, domestic demand remained stable, while the raw materials market fluctuated, causing anode prices to rise before falling. Prices continued their upward trend into April, climbing Yuan 300/tonne MoM. This was primarily attributed to Middle East geopolitical risks sustaining tight crude oil supplies. Declining capacity utilization rates at domestic delayed coking units led to tighter supply and stronger cost support. Procurement of standard and low-sulfur coke accelerated, pushing medium-sulfur coke averages sharply higher. Consequently, anode prices rose for two consecutive months, accumulating a gain of Yuan 500/tonne. Subsequently, weakening trading activity in the petroleum coke market driven by shifts in downstream buying patterns led to price declines. By June, anode prices retreated slightly amid positive market sentiment.

During the quarter, domestic aluminum capacity swaps and technical upgrades progressed steadily, with monthly output continuing to inch upward. Sustained high profitability in the aluminum sector encouraged stable, high-volume production, supporting healthy anode consumption.

Exports remained robust, with 437,100 tonnes shipped in April and May alone, a 23.19% YoY increase. Supported by domestic restarts, new capacity and strong overseas orders, the anode market demonstrated vigorous production and sales.

Cost analysis shows the average price for 3B petroleum coke in Q2 reached Yuan 3,475.57/tonne (up Yuan 382.86/tonne QoQ), while coal tar pitch averaged Yuan 5,009.2/ton (up Yuan 142.07/ton QoQ).

Overall, production levels varied periodically, with minor monthly output fluctuations. Early-year output dipped due to heating season restrictions and environmental policies in Shandong, Henan, Shanxi, and Xinjiang. However, as the heating season concluded, prices recovered, and downstream demand improved, boosting both output and prices. Post-Lunar New Year, monthly anode production remained elevated. New and upgraded projects, such as those by Shandong Haiyun and Shandong Zhongkeruihai came online in H1, contributing to higher overall supply compared to the previous year.

Demand remained firm; since early 2026, aluminum operating capacity has trended upward. New startups and restarts in Inner Mongolia, Xinjiang, and Liaoning were completed in H1, lifting aluminum output. Other regions operated stably. Mysteel estimates H1 2026 aluminum output at 22.44 million tonnes (increased by 3.0% YoY). High operating rates of aluminum producers throughout the period sustained strong demand for prebaked anodes.

Outlook for the prebaked anode market in H2 2026

In July, in terms of raw materials, such as petroleum coke, domestic refineries will continue maintenance turn arounds, with monthly output projected at approximately 2.2 million tonnes. As refineries resume normal operations in Q3, domestic supply is expected to be relatively ample. However, uncertainty persists regarding downstream producers' cost pressures and the pace of demand recovery. High port inventories and traders' eagerness to destock will likely cap price gains for domestic coke.

Supply-demand dynamics will remain the dominant price driver. Petroleum coke prices are forecast to oscillate with a slight upward bias in Q3, with low-sulfur coke remaining volatile at high levels and unlikely to see sharp corrections.

In terms of coal tar pitch, in H2 2026, the high-temperature coal tar market faces mixed bullish and bearish factors, likely keeping prices range-bound around the mid-level. Cost support for coal tar pitch remains intact. While demand is expected to improve, new deep-processing units are scheduled to come online domestically. This makes resolving supply-demand contradictions difficult, leaving the market lacking sustained unilateral drivers. Coal tar pitch is thus expected to trade within a range in H2.

In H1, on supply side, anode prices rose more often than they fell, stimulated by rising raw material costs. However, four months saw prices in decline. Due to the lag effect of anode pricing and production cycles, producer profitability faced mild constraints. Some smaller enterprises, pressured by costs and order flow, switched product lines or exited the market.

Looking ahead, new capacities are poised to come online in H2, including projects in Xinjiang (Chenfeng, 200 kt/y), Guangxi (Qiangqiang, 600 kt/y), and Inner Mongolia (Ruixing, 300 kt/y). Several baking furnace upgrade projects in Shandong, Gansu, and Xinjiang are also slated for completion.

Overall, installed capacity will continue expanding, and industry concentration will further increase. With most enterprises holding solid annual orders and new project outputs ramping up, prebaked anode production is expected to remain at high levels through H2 2026.

On demand side, domestic aluminum operating rates are currently high. Capacity changes in H2 will primarily involve swaps. Full-year 2026 domestic aluminum output is projected at approximately 45.4 million tonnes (increased 2.3% YoY), supporting robust domestic anode demand.

Overseas demand is also expected to strengthen. Key export destinations, Malaysia, Indonesia, Norway, the UAE, Russia, and Canada, will remain central. Ongoing aluminum capacity expansions in Southeast Asia, coupled with anticipated improvements in tight ocean freight capacity, should sustain high levels of overseas procurement for Chinese prebaked anodes in H2.

As new projects continue releasing volume, the oversupply situation in the prebaked anode market will likely intensify. While rigid demand from the domestic aluminum sector provides a floor, price volatility will remain heavily dependent on raw material markets. It is forecast that mainstream prebaked anode prices in China will fluctuate within a range of Yuan 5,100–5,800/tonne in the second half of 2026.

Conclusion

In summary, the prebaked anode market in H1 2026 was highly sensitive to feedstock volatility, recovering from early weakness to a mid-year rally driven by geopolitical factors. Despite robust demand from domestic smelters and strong export growth, margins remained tight due to pricing lags.

Looking ahead to H2 2026, new capacity expansions are expected to increase supply, but this will be balanced by steady downstream demand. With raw material costs likely to trade sideways, prebaked anode prices are forecast to stabilize within a range of Yuan 5,100–5,800/tonne.

Written by Regina WANG

wangjiaqie@mysteel.com