FEATURE-3: What is for iron ore in ‘20 after dramatic ’19

Will the history repeat itself or will now be the turn for the Chinese steel mills to be at the centre of the stage for 2020?

China’s steel market to be in a lull until the virus is under control

So far in 2020, however, the most unpredictable has remained to be the demand from the Chinese steel mills and probably the rest of the world, as no one knows when the COVID-19 will be under control.

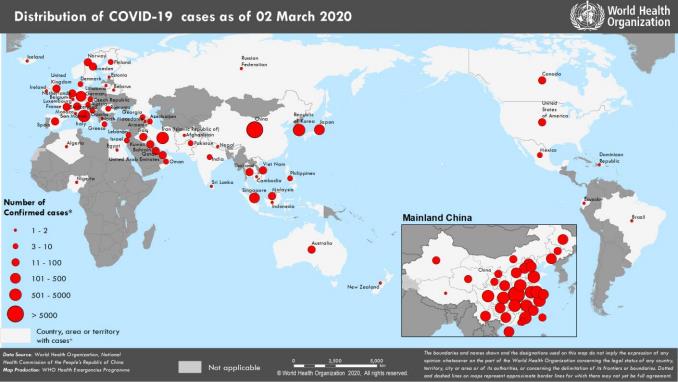

The virus hit China in late January in all of its 31 provinces, autonomous regions, and special administrative zone, and until March 2, it had attacked 65 countries including China, and confirmed cases totaled 88,948 including 80,174 in China, and the rest of the world 8,774 cases. The virus had caused 2,915 deaths in China and 128 deaths outside China, according to the latest sharing by the World Health Organization.

Map of countries, territories or areas with reported confirmed COVID-19 cases as of March 2 2020

Source: WHO

Source: WHO

China, in the past over one month of battling against the disease, had basically put its economy on hold other than requesting all the enterprises working in the essential fields including medical supplies such as masks and protective suits and daily necessities such as food processing and crucial infrastructure projects to return to work since the start of the February.

The stall in China’s economy saw the country’s Purchasing Managers' Index (PMI) for the manufacturing industry slumped to 35.7 for February from the 50 for January, and the impact may not end here, as the China Iron & Steel Association just warned of possible steel price declines for some time in March, though there may be chances for them to bottom out in late March when the domestic demand picks up.

Hubei, where Wuhan, the epicentre of the virus is located, is still in the middle of the heated battle against the COVID-19, and the province, with 8-9% of China’s auto market share and many auto spare parts factories are located, is by no means to restart many of local plants yet, though China Baowu Steel Group’s steel mills are operating to ascertain any urgent needs for steel locally.

“China’s steel output will very likely post a year-on-year decline in the first quarter, though steel mills will try to make up for the losses for the rest of the year (when the virus is under control),” a Beijing-based steel analyst commented, explaining, “2020 is the year for China to conclude its 13th Five-Year Planning Period (2016-2020) and to upgrade itself to a well-off society, and steel industry will remain a core contributor to accomplish the mission.”

Under all the circumstances, China may very likely face a rather abundant if not excess supply in iron ore, which will exert some pressure on iron ore prices, though the balance may vary from time to time, he shared the market view.

The global iron ore price, amid the tweaks in the demand and supply scenarios in China as well as possible a further slow-down in global economy because of the virus outbreak, seems unlikely to repeat its 2019 price volatility in 2020, though it may need to brace itself for price declines somewhere for the next 10 months.

Written by Victoria Zou, zyongjia@mysteel.com

Edited by Hongmei Li, li.hongmei@mysteel.com