BLOG: China’s steel prices end 2020 on a high note

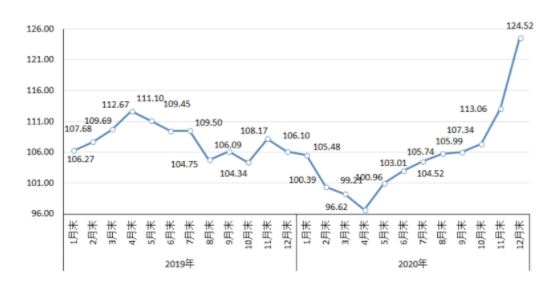

China’s composite steel pricing index (CSPI), compiled by the China Iron & Steel Association (CISA), shot up to 124.52, or a two-year high at least, and its 2020 average was at 105.57, or down 2.41 basis points on year,

CISA’s CSPI by month over 2019-2020 (source: CISA)

The breakdown of the CSPI for 2020, though, has shown a very interesting phenomenon in that the long steel pricing index, though seemingly at the centre of the stage most of the time last year, was beat hard by the flat steel pricing index in the last month of 2020 and thus in the whole-year performance.

For the whole 2020, the long steel pricing index averaged 109.76, or down 4.21 basis points on year, while the flat steel pricing index just inched down 0.61 basis point on year to 103.63, according to the CISA sharing on January 19.

By the end of December, the winners of the eight major steel products under CISA’s monitoring were all flat steel products including plate, hot-rolled coil (HRC), cold-rolled coil (CRC), and galvanized steel with their prices up Yuan 476-827/tonne ($73.7-128/t) on month against the Yuan 182-229/t on-month gains for rebar and wire rod.

As for the yearly average price movement for 202 among the eight products, HRC and CRC were the winners, as the former almost levelled with 2019 with a Yuan 1/t gain and the latter up Yuan 164/t or 3.76% on year, while the others all posted on-year losses.

All the achievements in China’s steel prices, nevertheless, were hard, as they were in the context of surges in the prices of all the steelmaking raw materials, and for December alone, metallurgical coke price gained the most by Yuan 231/t on month and scrap the runner-up with an on-month increase of Yuan 141/t, which was rather surprising too, as for most of 2020, the market had been intensely watching the iron ore price movements.

Moreover, December is not a steel consumption peak in China most of the years though the year 2020 was by no means “normal” or “traditional”. Even so, China’s domestic steel prices especially for flats would not have outperformed longs if just because of the domestic demand.

The robust recovery in the global steel market had played a crucial role, Mysteel Global noted, and this has also been confirmed by the data from CISA, as last December, the global flat steel pricing index gained 35.2% on year or 13.6% on month, both being much higher than the gains in the long steel pricing index by 24.2 percentage points and 6.6 percentage points respectively.

The Chinese steel mills have indeed by challenged by the rising raw material costs especially since the latter half of 2020, but the exceptionally strong rebound in domestic steel demand and afterwards in the global steel demand especially for flats have to some extent eased the pressure, Mysteel Global noted.

Written by Hongmei Li, li.hongmei@mysteel.com