MYSTEEL: Little growth in China iron ore demand in August

Source: Mysteel

Aug 04, 2022 15:00

The report points out that the production cuts observed by most mills recently had prevented them from losing more money on their finished steel sales and that during the period, their costs for raw materials had declined substantially, especially those of merchant coke.

Domestic steel prices have rebounded of late, Mysteel notes, and these two factors together had given some mills confidence to lift their production. In parallel, market pundits expect domestic steel demand to gradually pick up in the months ahead.

As of August 3, China's national price of HRB400E 20mm dia rebar had strengthened to Yuan 4,300/tonne including the 13% VAT, compared with the previous low of Yuan 3,964/t on July 15.

Meanwhile, after five rounds of cuts in steelmakers' coke procurement prices since late June, as of August 3 China's national composite coke price had slumped to Yuan 2,381.8/t including the 13% VAT, compared to the previous high of Yuan 3,484.3/t on June 17, according to Mysteel's assessment.

Consequently, if steelmakers gradually ramp up their production as anticipated, iron ore demand would remain firm or even increase in the near future, the report suggested.

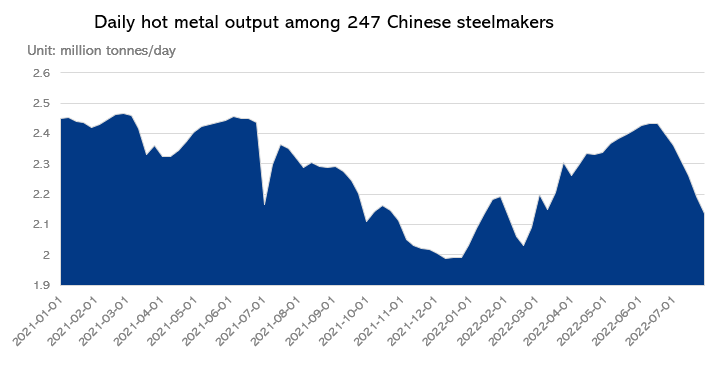

According to Mysteel's data, over July 22-28, daily hot metal output among the 247 steelmakers regularly monitored had dipped to an average of 2.14 million tonnes/day, the lowest since late February.

Source: Mysteel

Regarding iron ore supply, Mysteel predicts that availability of imported iron ore at Chinese ports will tighten this month, given the reduction in shipments in July, especially from miners in Australia and those in some non-mainstream countries.

Last month, Mysteel's data indicated that the total global iron ore shipments to all destinations had declined to 131 million tonnes, down 2.57 million tonnes on month.

However, during August domestic iron ore production is expected to rise further as many miners will need to lift their production in the months ahead to fulfill their annual production guidance.

Under this scenario, Mysteel still highlights the possibility of an oversupply in the country's iron ore market, which will see the total inventories at China's ports continue to climb during the month. The increment might be lower than last month, however.

Mysteel's latest data showed that the total inventory of imported iron ore at China's 45 ports surveyed weekly increased to a two-month high of 135.3 million tonnes by July 28, or up 9.09 million tonnes from the volume on June 30.

Source: Mysteel

Mysteel's report suggests that for the iron ore market in August overall, the focus will still be on demand, and that during the first half month, iron ore prices might gain some support from ore restocking among steelmakers beefing up output.

However, should there be no consistent recovery in steel demand in the second half of the month and the mills' margins decline again, the steelmakers may choose to control their production once more. Should this be the case, iron ore prices might again come under pressure.

During July, iron ore prices headed further south, with Mysteel SEADEX 62% Australian Fines plunging to as low as $95.75/dmt CFR Qingdao on July 21 – the lowest since November 26, 2021. However, the improved market sentiment recently saw the index subsequently recover to $112.55/dmt as of August 3.

Written by Victoria Zou, zyongjia@mysteel.com

Edited by Zhenqi Yang, yangzhenqi@mysteel.com

You May Also Like

Price Curve

Daily Prices

Iron ore inland water freight charges: China

Jun 04, 2026 09:28

Iron ore portside prices: Dalian port

Jun 04, 2026 09:24

Iron ore portside prices: Zhanjiang port

Jun 04, 2026 09:20

Iron ore portside prices: Huanghua port

Jun 04, 2026 09:20