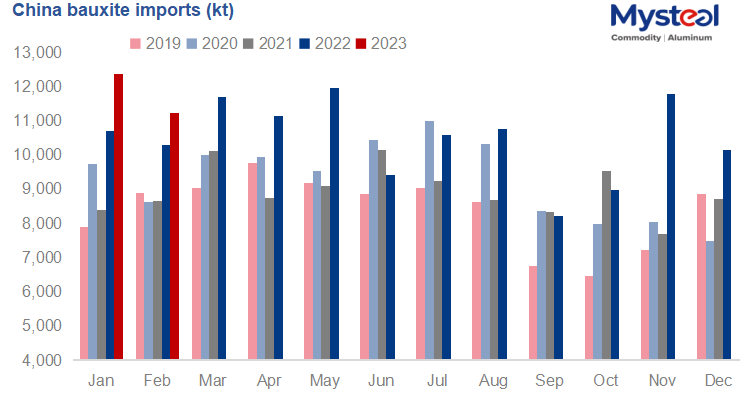

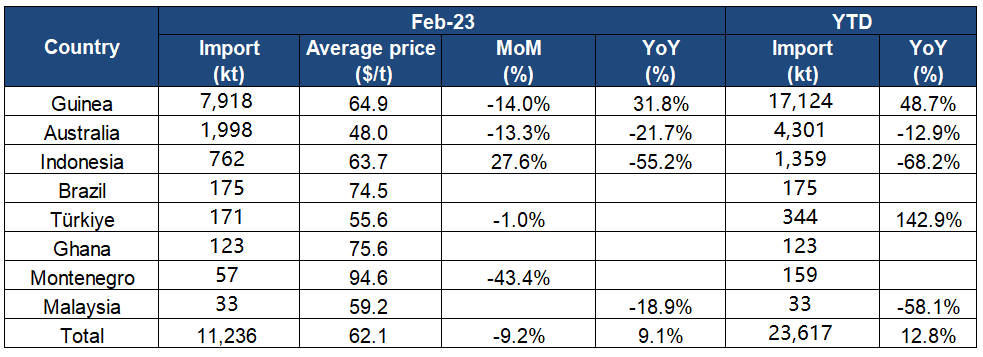

According to GACC, China imported 11.24 million tonnes of bauxite in Feb, down 9.2% on month, but up 9.1% on year. Bauxite imports from Guinea were 7.9 million tonnes in Feb, down 14% on month, and 31.8% higher than the same period of last year. Imports from Australia were down 13.3% on month to 2 million tonnes, and tonnages from Indonesia were up 27.6% on month to 762 kt.

Data: GACC

Total bauxite imports for the first two months were up 12.8% to 23.62 million tonnes. China saw a sharp increase in imports from non-mainstream sources. In the first two months, China imported 833 kt of bauxite from other sources, up 280% on year, including Turkey ( 344 kt), Montenegro (159 kt), Ghana( 123 kt), Malaysia( 33 kt), and Brazil (175 kt).

Data: GACC

Data: GACC

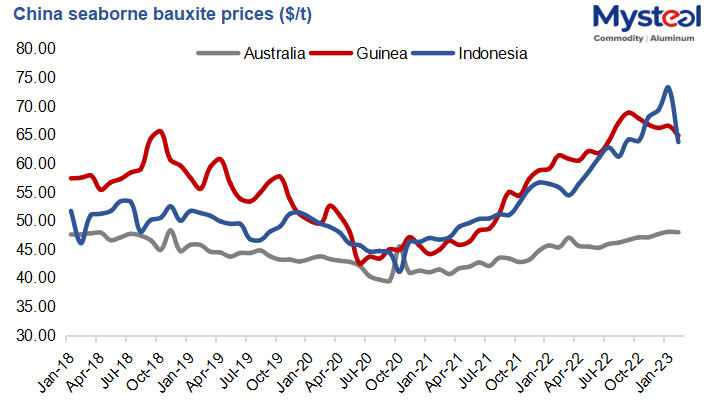

Seaborne bauxite prices declined in Feb driven by falling freight rates and thin margins of alumina producers. The average price for cargoes from Guinea was down to $ 64.9/t from Jan's $66.6/t, and the average price for bauxite from Indonesia was $63.7/t, lower than Jan's $73.2/t.

Data: GACC

In terms of supply, Australia bauxite supply will increase after Metro Mining (MMI) expands its capacity to 7 million tonnes per annum over the next 2 years. MMI has agreed offtake agreements for up to 5 Mt for 2023, and has signed a non-binding MOU with a third base load customer for offtake commencing in 2024 and ramping up in 2025 to 2 Mt per annum. The counterparty is Chifeng Qihui Aluminum Development Limited, a greenfield alumina project in Inner Mongolia, China. The project with a total refining capacity of 6.5 million tonnes/a is expected to be fully commissioned in 2025.

Guinea will remain the top bauxite supplier to China. However, the ramp-up of bauxite capacity and exports in that country will be affected by the uncertainty of mining and export policy and the construction of infrastructure in that country. Indonesia's export ban in mid-2023 has begun to have an impact on the supply structure. The shipments from non-mainstream sources have seen a sharp increase.

In terms of demand in China, in the near term, two brownfield alumina projects relying on seaborne bauxite are expected to be commissioned in late Q1 and early Q2. Guangxi Jinxin Chemical's expansion project with 1.2 MTPA capacity is expected to start production in late Q1 or early Q2. Shandong Lubei's 1MTPA expansion project is expected to be commissioned in Q2.

In the long run, China's demand for seaborne bauxite is expected to remain strong due to alumina capacity increase and the exit of Indonesia from the market. According to Mysteel's survey, China will likely see around 5 MTPA new alumina capacity to be commissioned in 2023, and has around 20 MTPA proposed alumina capacity, which will all rely on seaborne bauxite.

Written by Marina, yangli@mysteel.com