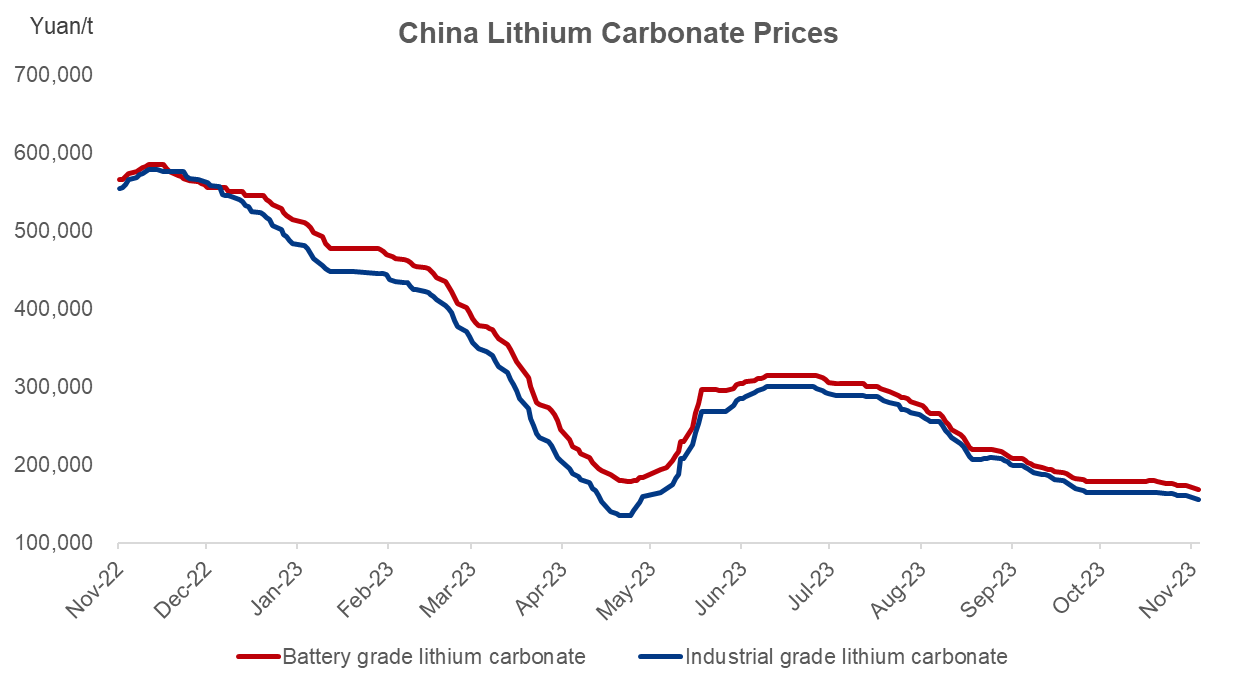

The prices of battery grade and industrial grade lithium carbonate showed a weekly drop of 2.89% and 2.81% respectively over October 30-November 3, and recorded Yuan 168,000/tonne and Yuan 156,000/t respectively last Friday November 3.

Figure 1-1. China Lithium Carbonate Prices

Source: Mysteel

Looking back on October, China's lithium carbonate prices moved rangebound and dropped slightly around the end of the month. The prices in the futures and spot market diverged significantly.

On the fundamentals, the smelters were slow in building raw material stocks and the production pace also slowed down. Instead, they took more tolling orders. In addition, high lithium ore prices forced the smelters to hold the lithium carbonate prices firm. However, with downstream players bearish towards the follow-up market, they purchased lithium carbonate merely on rigid demand.

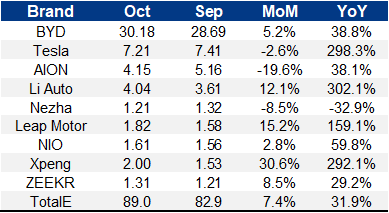

Regarding the end-market, Mysteel estimates that the total sales volume of new energy vehicles (NEVs) could add up to 890,000 units in October based on available data of key NEV brands, an increase of 7.4% from September.

Specially, BYD sold 301,800 vehicles in October, rising 5.2% month on month (MoM) and 38.8% year on year (YoY). The sales volume of Tesla fell 2.6% from September at 72,100 units. XPeng reported a monthly growth of 30.6% and an annual surge of 292.1%. Among them, XPeng's electric SUV registered a monthly sales of 8,741 units, ranking first among all SUV brands priced above Yuan 200,000.

Table 1-1. Sales of Key NEV Brands and Estimate

Source: NEV brands' official websites, Mysteel

The installed capacity of power batteries is estimated at 37.5 GWh in October, rising 3% from 36.4 GWh in September. The estimation is based on BYD's combined installed capacity of power batteries and energy storage batteries at 15.3 GWh in October, an increase of 7% MoM. In September, the energy storage segment slowed down featuring destocking and production reduction, in addition to reducing export orders in Europe and US.

On the raw material end, the production of LFP is projected to rise 1.84% MoM at 155,100 t in October, while that of ternary cathode materials fall 5.67% MoM at 49,900 t. Taken together, the consumption of lithium carbonate is estimated at 53,000-54,000 t (considering that some 6-series NMC uses lithium carbonate).

The production scheduling of LFP and ternary cathode materials is likely to fall 3% and 5% respectively MoM in November against an anticipated production cuts of 8% among battery cell factories, per Mysteel survey.

From the perspective of inventory, the smelters held two weeks of lithium carbonate inventory, while the LFP material factories' lithium carbonate inventory was less than two weeks. The finished products inventory of cathode active material (CAM) factories was between 0.5-1 month. The battery cell manufacturers held around three months of finished products inventory.

In other words, the lithium carbonate stocks held by smelters, CAM factories, and the traders were relatively low.

In addition, a salt lake company in Qinghai Province auctioned 500 t industrial grade lithium carbonate last week, with prices of Yuan 152,000-153,000/t, which were fractionally higher than the spot prices on the same day.

On the raw material end, the lithium ore inventory has been mounting. The lithium ore inventory at ports and in domestic warehouses recorded 146,000 t as of November 3, up 15,000 t from the previous week. The port inventory jumped amid constant arrivals of seaborne lithium ore, as well as downstream players refusing high-priced ore. On the other hand, the steady production ramp-up of spodumene in Xinjiang Province also contributed to the stock build-up.

Concerning lithium ore prices, some smelters have changed their ore settling method with mines from "M/M-1/Q-1" to "M+1". That is, falling lithium carbonate prices will pull down lithium ore prices, which subsequently weigh on lithium carbonate prices in the future.

At present, the upstream and downstream players are still in tug-of-war over the prices, but the battery cell manufacturers seem to have a greater say. First, the downstream players are not in a rush to purchase on expected oversupply on the raw material end next year. In addition, some listed smelters have slightly lowered their offers as they are to promote the sales ahead of the annual reporting period. Lastly, the battery cell factories still hold three months of finished products inventory, which is able to answer the end-market demand should the demand growth navigates normally.

In this case, lithium carbonate prices are expected to fall through November.

Written by Aggie Hu, huchenying@mysteel.com