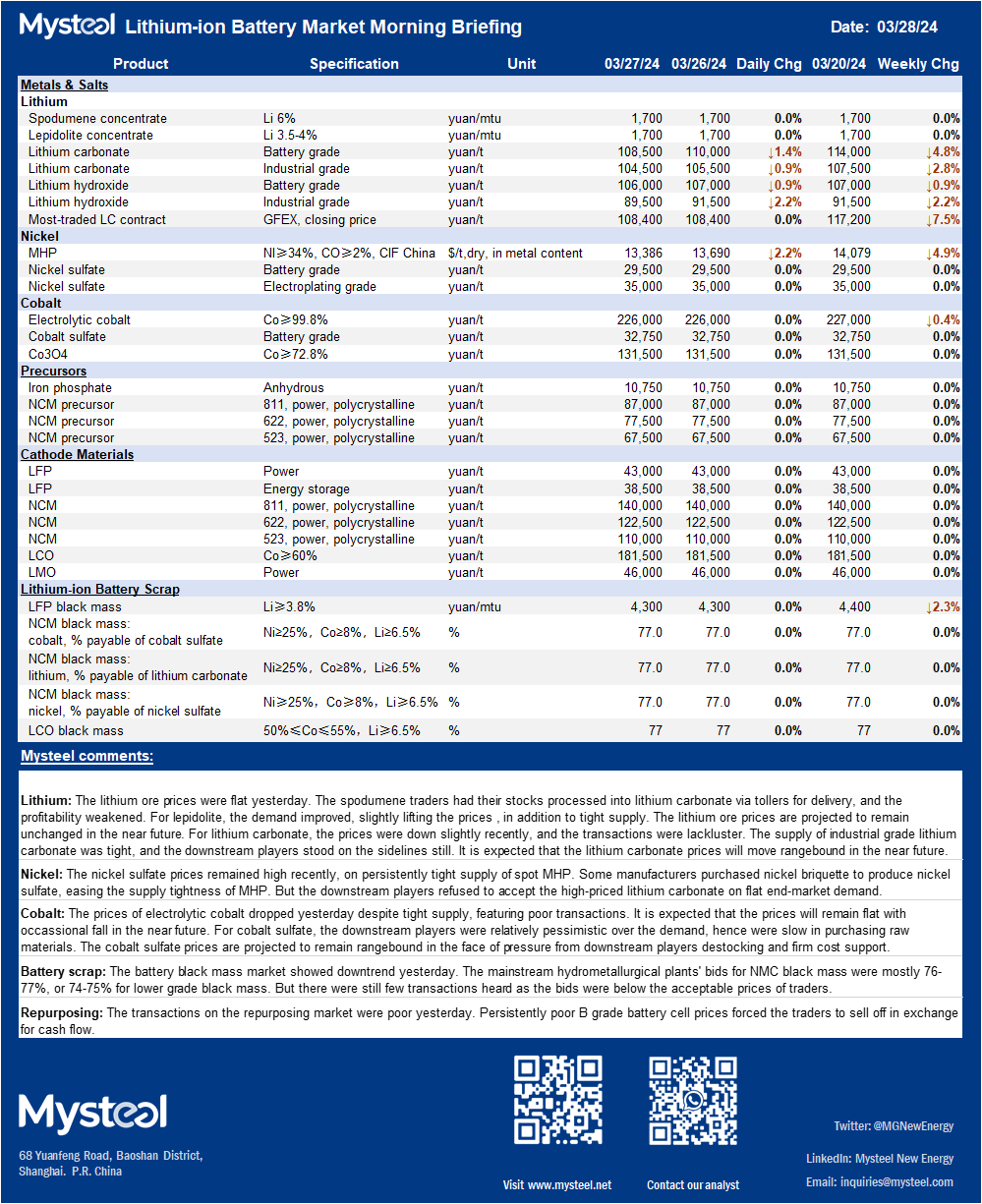

Lithium: The lithium ore prices were flat yesterday. The spodumene traders had their stocks processed into lithium carbonate via tollers for delivery, and the profitability weakened. For lepidolite, the demand improved, slightly lifting the prices , in addition to tight supply. The lithium ore prices are projected to remain unchanged in the near future. For lithium carbonate, the prices were down slightly recently, and the transactions were lackluster. The supply of industrial grade lithium carbonate was tight, and the downstream players stood on the sidelines still. It is expected that the lithium carbonate prices will move rangebound in the near future.

Nickel: The nickel sulfate prices remained high recently, on persistently tight supply of spot MHP. Some manufacturers purchased nickel briquette to produce nickel sulfate, easing the supply tightness of MHP. But the downstream players refused to accept the high-priced lithium carbonate on flat end-market demand.

Cobalt: The prices of electrolytic cobalt dropped yesterday despite tight supply, featuring poor transactions. It is expected that the prices will remain flat with occassional fall in the near future. For cobalt sulfate, the downstream players were relatively pessimistic over the demand, hence were slow in purchasing raw materials. The cobalt sulfate prices are projected to remain rangebound in the face of pressure from downstream players destocking and firm cost support.

Battery scrap: The battery black mass market showed downtrend yesterday. The mainstream hydrometallurgical plants' bids for NMC black mass were mostly 76-77%, or 74-75% for lower grade black mass. But there were still few transactions heard as the bids were below the acceptable prices of traders.

Repurposing: The transactions on the repurposing market were poor yesterday. Persistently poor B grade battery cell prices forced the traders to sell off in exchange for cash flow.