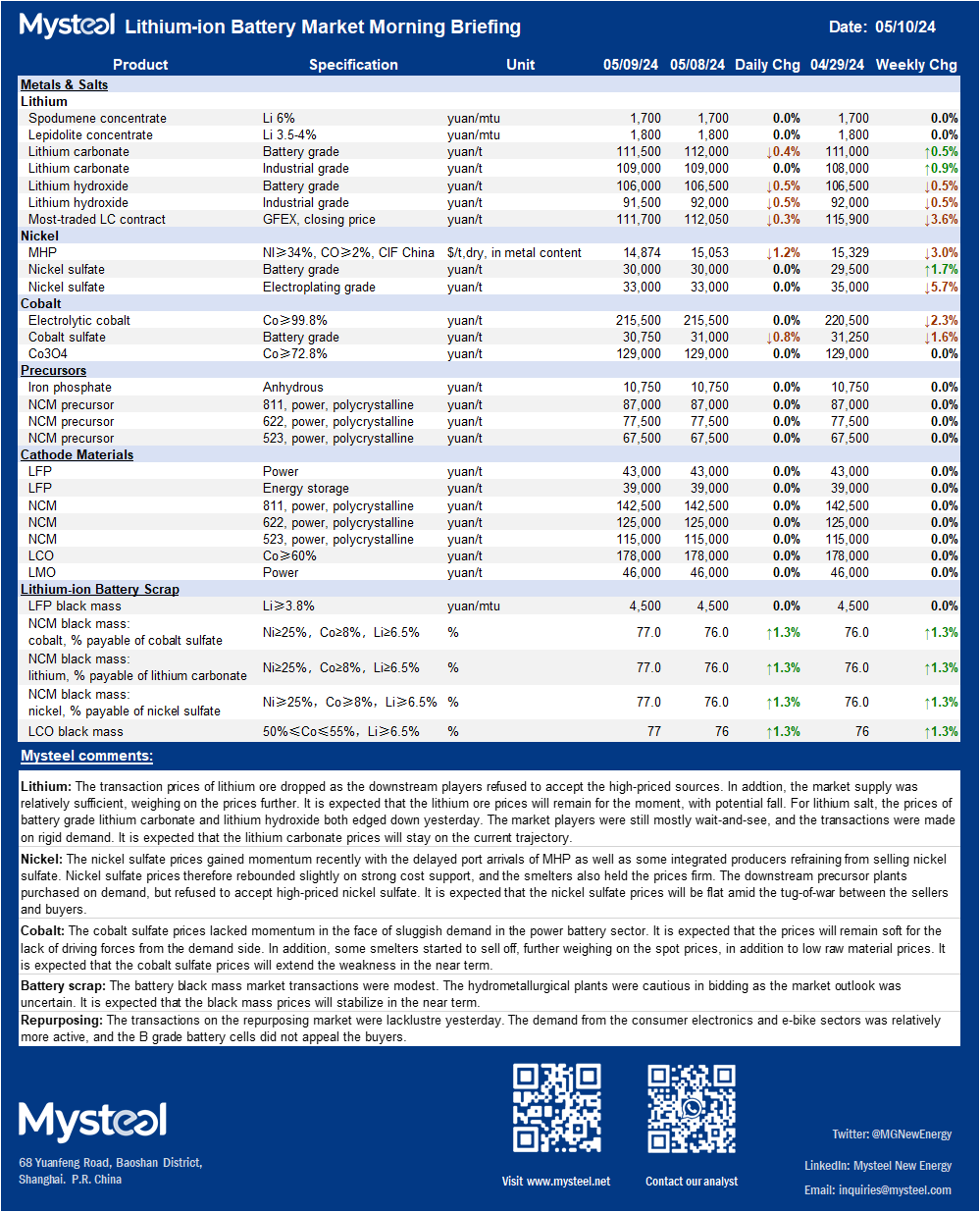

Lithium: The transaction prices of lithium ore dropped as the downstream players refused to accept the high-priced sources. In addtion, the market supply was relatively sufficient, weighing on the prices further. It is expected that the lithium ore prices will remain for the moment, with potential fall. For lithium salt, the prices of battery grade lithium carbonate and lithium hydroxide both edged down yesterday. The market players were still mostly wait-and-see, and the transactions were made on rigid demand. It is expected that the lithium carbonate prices will stay on the current trajectory.

Nickel: The nickel sulfate prices gained momentum recently with the delayed port arrivals of MHP as well as some integrated producers refraining from selling nickel sulfate. Nickel sulfate prices therefore rebounded slightly on strong cost support, and the smelters also held the prices firm. The downstream precursor plants purchased on demand, but refused to accept high-priced nickel sulfate. It is expected that the nickel sulfate prices will be flat amid the tug-of-war between the sellers and buyers.

Cobalt: The cobalt sulfate prices lacked momentum in the face of sluggish demand in the power battery sector. It is expected that the prices will remain soft for the lack of driving forces from the demand side. In addition, some smelters started to sell off, further weighing on the spot prices, in addition to low raw material prices. It is expected that the cobalt sulfate prices will extend the weakness in the near term.

Battery scrap: The battery black mass market transactions were modest. The hydrometallurgical plants were cautious in bidding as the market outlook was uncertain. It is expected that the black mass prices will stabilize in the near term.

Repurposing: The transactions on the repurposing market were lacklustre yesterday. The demand from the consumer electronics and e-bike sectors was relatively more active, and the B grade battery cells did not appeal the buyers.