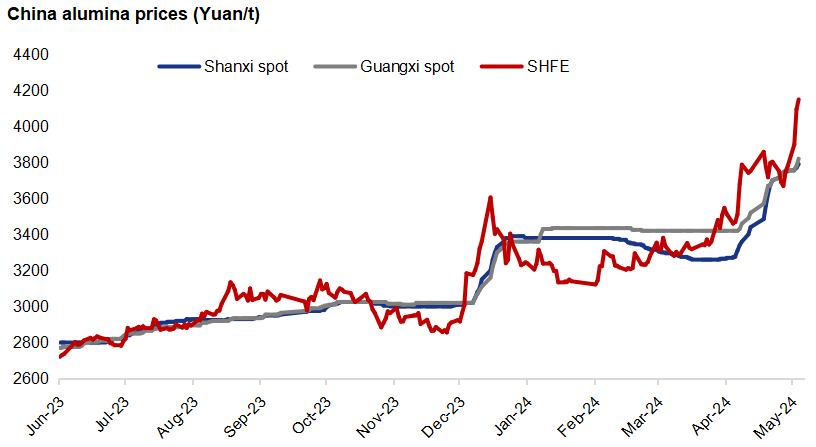

We observed a slowdown of the upward pace of China's alumina prices last week on the back of increasing alumina production in China and easing concerns over domestic bauxite supply. However, the market regained strong momentum after the news of Australian alumina supply disruptions.

Rio Tinto has declared force majeure on third-party contracts for alumina exports from its refineries in Queensland, Australia, due to restricted gas capacity levels at its operations. SHFE 2407 alumina contract hit the daily limit-up on April 21 boosted by the news.

Yarwun and QAL two alumina refineries have been operating at reduced capacity after a fire on a crucial gas pipeline in March. The total alumina installed capacity of these two refineries is 7.35MTPA, and alumina production was 1.57 million tonnes in Q1 2024. According to the pipeline operator's current estimation, the timing for gas flows to return to normal levels is in the second half of 2024. Apart from these two refineries, Alcoa's Kwinana alumina refinery is also reducing production and will be fully curtailed in Q3. The refinery with a total capacity of 2.2MTPA and has been operating at approximately 80 percent of its nameplate capacity since January 2023.

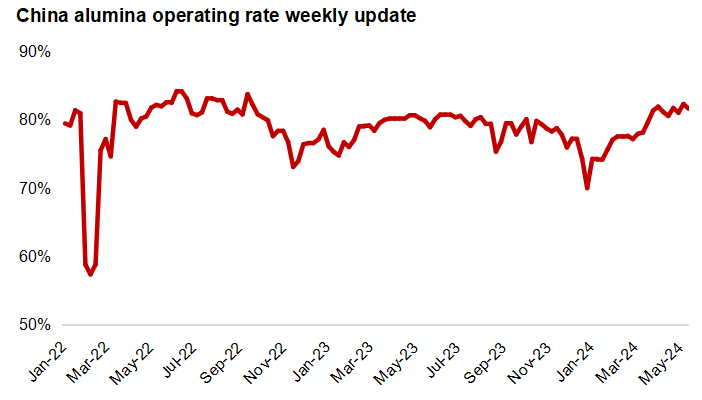

Alumina production in China keeps rising stimulated by high margins, which weakens the upward momentum of China's alumina prices. According to Mysteel's survey, alumina weekly operating rate has been standing above 80% for over a month, and some restarts will be seen in June.

Source: Mysteel

Meanwhile, we also saw a weakening support from the raw materials side. Bauxite supply issues in Shanxi and Henan have begun to ease after a few restarts. Besides, bauxite imports increased in April, reaching a new record high, which eased market concerns over seaborne bauxite supply, especially in Guinea.

However, rising demand, the expectations of a slow recovery of domestic bauxite supply and falling imports continue to provide support to the alumina market and keep alumina prices staying on an upward trajectory.

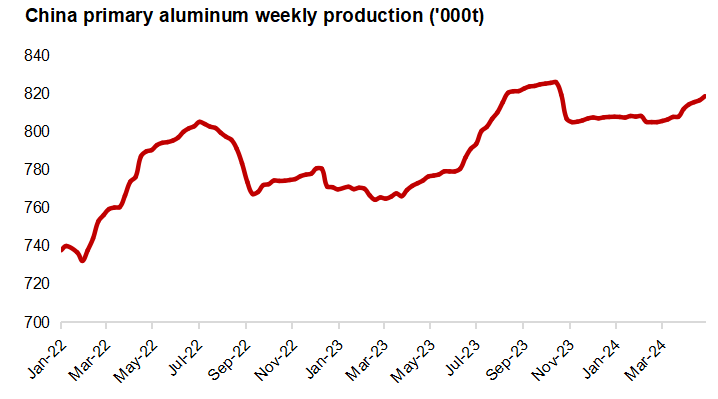

In terms of demand, continuous resumption in Yunnan pushed China's total aluminum operating capacity higher. According to Mysteel data, the operating capacity in Yunnan has recovered to 5.43MTPA as of May 16, making the operating rate in that region up to 88%. The restarts will continue in June. Besides, Inner Mongolia will also see an increase in smelting capacity due to the new commissioning of Huayun Phase III.

Source: Mysteel

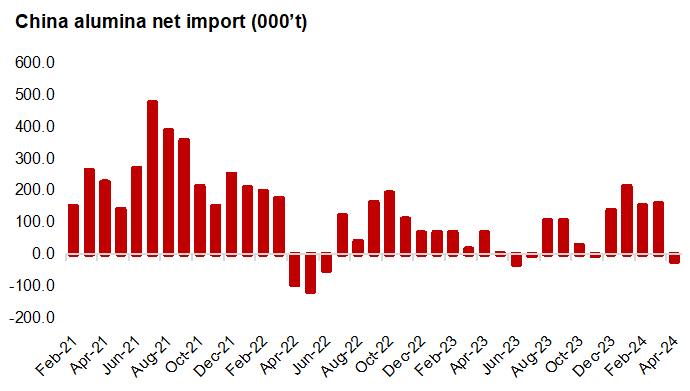

A sharp decrease in imports and a relatively stable export made the Chinese market turning into a net exporter in April. According to GACC, China imported 108kt of alumina in April, down 64% on month, but up 59% on year. Alumina exports were 130kt in April, down 9.5% on month but up 78.4% on year. It is expected that alumina import in May will remain low due to closed import arbitrage.

Source: GACC

Mysteel daily assessments were Yuan3,760-3,820/t for Shanxi spot alumina on May 22, up Yuan20/t from the previous day, and Yuan3,780-3,860/t for Guangxi spot cargo, up Yuan40/t from the previous day. SHFE 2407 alumina contract closed at Yuan4149/t, rising Yuan55/t from the previous trading day. Mysteel expects that China's alumina price will remain on the upward trajectory in June driven by the changes in supply and demand.

Source: Mysteel