Have lithium prices hit the peak?

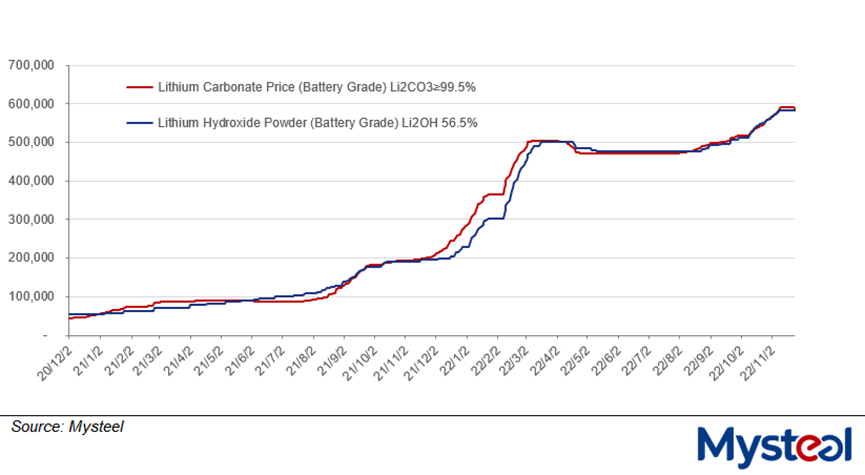

During November 19-25, Chinese price of battery-grade lithium carbonate (Li2CO3) dipped to Yuan 586,500/tonne after hovering high at Yuan 590,000/t for nearly two weeks, while that of battery-grade lithium hydroxide (LiOH) still stood high at Yuan 584,000/t, according to Mysteel's assessment. Despite the slight drop in the survey week, the price of lithium carbonate had risen from Yuan 517,500/t in October to Yuan 586,500/t, an increase of more than 13.3% in the past two months.

Figure 1-1 Lithium Hydroxide & Lithium Carbonate Prices (Unit Yuan/tonne)

In its first weekly report "When Will Lithium Compound Price Stop Rising?" released on October 21, the Nonferrous Metal & New Energy Research Center of Mysteel clearly pointed out that the maximum price of lithium compound that downstream users could accept is Yuan 650,000/t, and the inflection point in lithium compound price is expected to appear in mid-December. As mid-December looms and the price of lithium carbonate has slightly loosened, this weekly report once again suggests that lithium carbonate price may lose its upward momentum in the near term, and buyers need to pay attention to possible risks brought by the decline of lithium carbonate price.

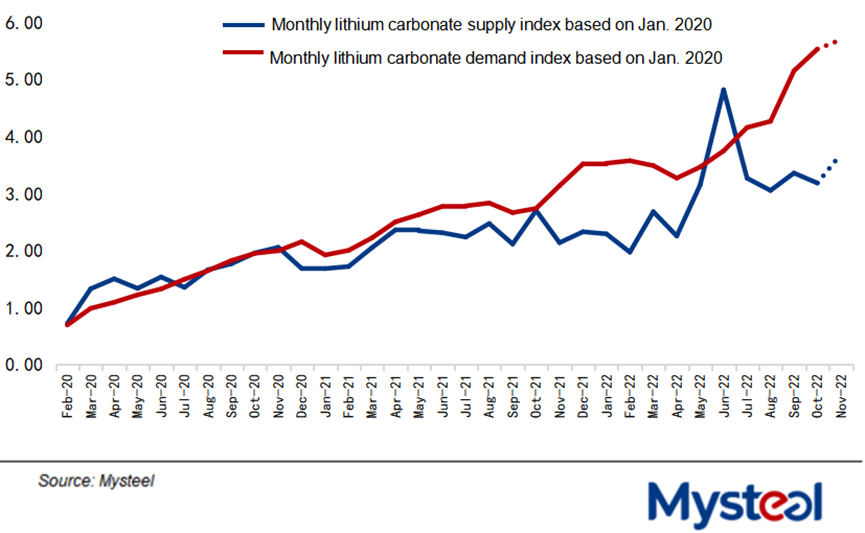

First, let's review the supply and demand gap and price trend of lithium carbonate in October from Figure 1-2. The capacity utilization rate of lithium carbonate rose to 72.86% in October, and the output increased by 1,800 tonnes month on month to 30,600 tonnes. Although the total supply of lithium carbonate dropped in the month due to a decrease of 4,100 tonnes in net import, downstream manufacturers' output of cathode materials still increased month on month. The two curves regarding supply and demand in Figure 1-2 tracked apart further in October, echoing the rise of lithium carbonate price from Yuan 517,500/t in early October to Yuan 561,500/t.

According to Mysteel's survey, the on-month growth of manufacturers' output of cathode materials slowed down in November, while the capacity utilization rate of lithium carbonate continued to increase. Total output and capacity utilization rate of lithium carbonate are expected to reach 31,600 tonnes and 75% respectively. On the other hand, the net import of lithium carbonate is expected to rise month on month. The gap between two curves of supply and demand started to narrow in November, indicating that the price increase of lithium carbonate may slow down.

Figure 1-2 Lithium Carbonate Supply and Demand Gap Model

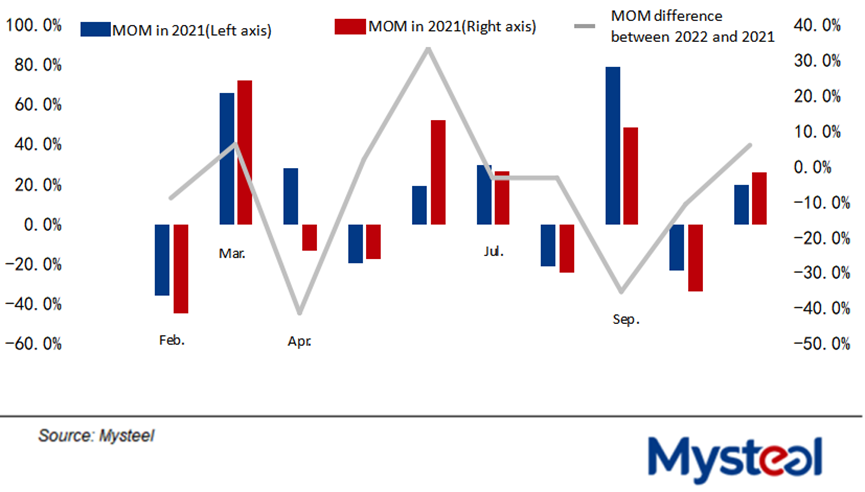

Regarding the downstream market, Mysteel's tracking indicators of the volume data of insured cars in China (Figure 1-3) showed that the on-month growth of the new energy vehicle (NEV) market in 2022 had already reached an inflection point in August 2022, which was repeatedly confirmed in September and October. Based on the analysis of car insurance license volume data in the first three weeks of November, the indicators performed slightly better than those in October, mainly due to automakers' sales promotion which drove up car deliveries. However, it is expected that automakers' scrambling to car assembly at the end of this year may greatly affect car sales in the first quarter of 2023, and further impact their demand for batteries in the next two to three months.

Figure 1-3 Monthly Car Insurance License Volume Data in China

Based on Mysteel's New Energy Survey, all battery plants except BYD have the intention to reduce production. Considering the weakening of downstream demand, some battery plants have lowered their production plan for December, and will not replenish more inventories accordingly.

In addition, cathode manufacturers' current stocks of lithium compound can last for about 15 days of use. Meanwhile, leading cathode manufacturers have also slowed down their production, with stocks sufficient for immediate needs, so they generally keep a wait-and-see stance on restocking, especially when lithium compound price is high.

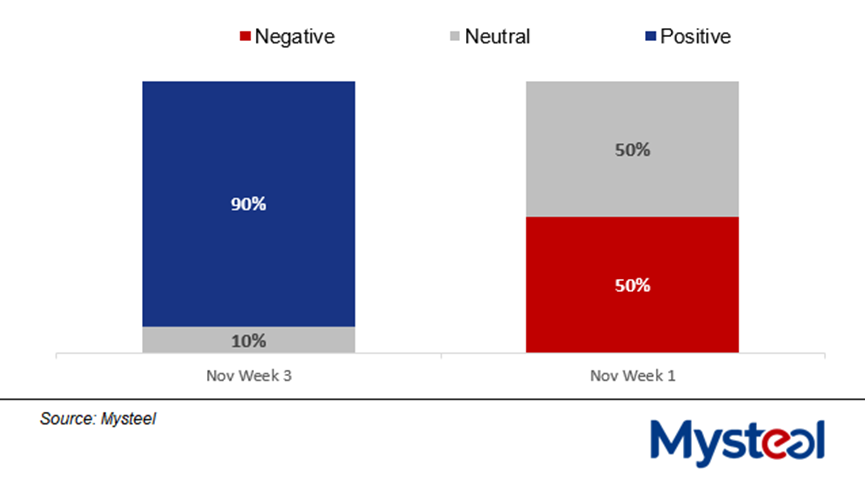

According to Oilchem's statistics of market sentiment on lithium compound price trend among traders (Figure 1-4), in the first week of October, up to 90% of traders were bullish about the future price of lithium compound. Traders with goods at hand opted to hoard them and hold off sales during the period, leading to a shortage of spot goods in the market, which further pushed up prices of lithium compound. However, with downstream demand showing signs of slowdown and the end of restocking activities, in the second week of November, 80% of traders believed that the lithium carbonate price would remain flat going forward, while by the third week of November, 50% of the traders turned negative and anticipated the price to fall, and the remaining 50% expected the price to remain stable. It is expected that in mid-December, more traders will become bearish on lithium compound price.

Figure 1-4 Lithium Compound Market Sentiment Survey

To sum up, although the capacity utilization rate of lithium carbonate has improved modestly in recent two months, the release of new capacity is still limited. The domestic lithium carbonate output is basically maintained at 30,000-32,000 tonnes per month, while the supply side is mainly affected by the monthly imported tonnage. Besides, upstream manufacturers' restocking activities driven by the rising demand from NEV producers at year-end have also gradually come to an end. Considering the impact of year-end assembly enthusiasm among automakers and the withdrawal of purchase subsidies on NEVs on the NEV sales in the first quarter of next year, it is expected that the price of lithium compound has been near the inflection point, and it may decline in mid-December.

Written by Mysteel Nonferrous Metal & New Energy Research Center

Edited by Ruby Zhang, zhangjiajing@mysteel.com; Alyssa Ren, rentingting@mysteel.com

MHP seaborne cargo prices: CIF China

Jun 16, 2026 11:56

Ferronickel seaborne cargo prices: China

Jun 16, 2026 11:55

Nickel ore portside prices: Lanshan port

Jun 16, 2026 11:26

Nickel ore portside prices: Lianyungang port

Jun 16, 2026 11:26

Nickel ore offer prices: Philippines

Jun 16, 2026 11:26