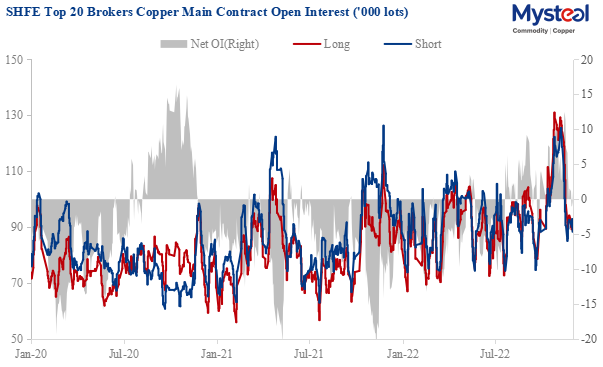

The Shanghai Futures Exchange's (SHFE) warehouse warrants for copper futures fell by 2,971 tonnes day on day to 27,385 tonnes on December 2, leading to a week-on-week decrease of 7,659 tonnes or 21.86%, and an increase of 6,715 tonnes or 32.49% month on month.

Both the ISM and Markit manufacturing indices of the US shrank in November, hitting their lowest levels since May 2020. The ISM manufacturing index came in at 49, while the final Markit manufacturing PMI came in at 47.7, both below the threshold of 50. It is also a sign that the US economy is slipping into recession. Copper prices rose again on the increasing expectations of the Fed's monetary policy shift, but recession expectations have also become stronger. Furthermore, the COVID policies in China are being optimized, giving confidence to the market.

LME copper inventories kept falling, while China's copper social inventories showed an increasing trend. But with the historically low inventories, copper prices are unlikely to fall deeply.

Towards the end of the year, there are more uncertainties about copper prices. The effects of optimistic expectations and incentive policies still need to be verified by the fundamentals. The new release of macroeconomic data and the changes in China's epidemic policies are worth paying attention to.

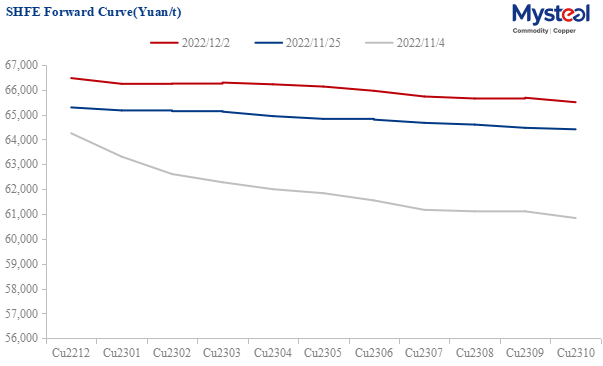

Data Source: SHFE

Data Source: SHFE

Written by Edenlis Huang, huangting@mysteel.com

Edited by Ting Ao, aoting@mysteel.com