China's propylene industry chain will witness rapid development in 2024, up by 10.7 million tonnes/year or 16.74% year on year, compared to 63.908 million t/y in 2023, according to data compiled by OilChem.

Source: OilChem

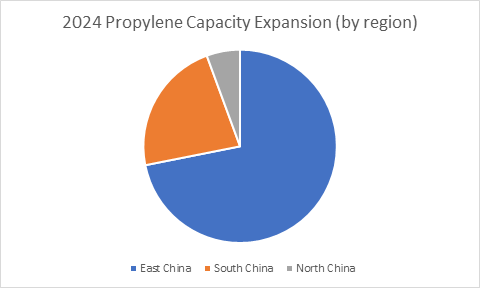

Geographically, new propylene capacities will be most pronounced in East China and South China, which will account for a significant 94.39% of total newly-added capacities in China, with 7.69 million t/y in East China and 2.41 million t/y in South China respectively. East China and South China enjoy location and demand advantages in China's propylene market, not only benefiting from convenient port transportation of feedstock, but also being close to major consuming markets.

Source: OilChem

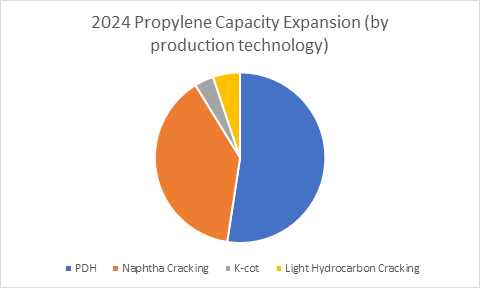

In terms of production technology, the proposed propylene projects will mainly center on PDH and naphtha cracking technologies. Notably, PDH accounts for 52.43%, due to its high yield and environmental protection characteristics.

In addition, with regard to downstream capacity expansion, new propylene capacities will mainly concentrate on PP, PO and phenol and acetone fields, with 10.255 million t/y, 1.25 million t/y and 0.25 million t/y respectively, according to proposed projects collected by OilChem so far.

For the moment, according to the scheduled commissioning plan, totaling 2.1 million t/y, three PDH units in East China might come on stream in Q1, with the possibility of postponement attributed to economic reasons.

Written by Ariel Guo, gq@oilchem.net

Edited by Navy Liu, liuchuanjun@mysteel.com