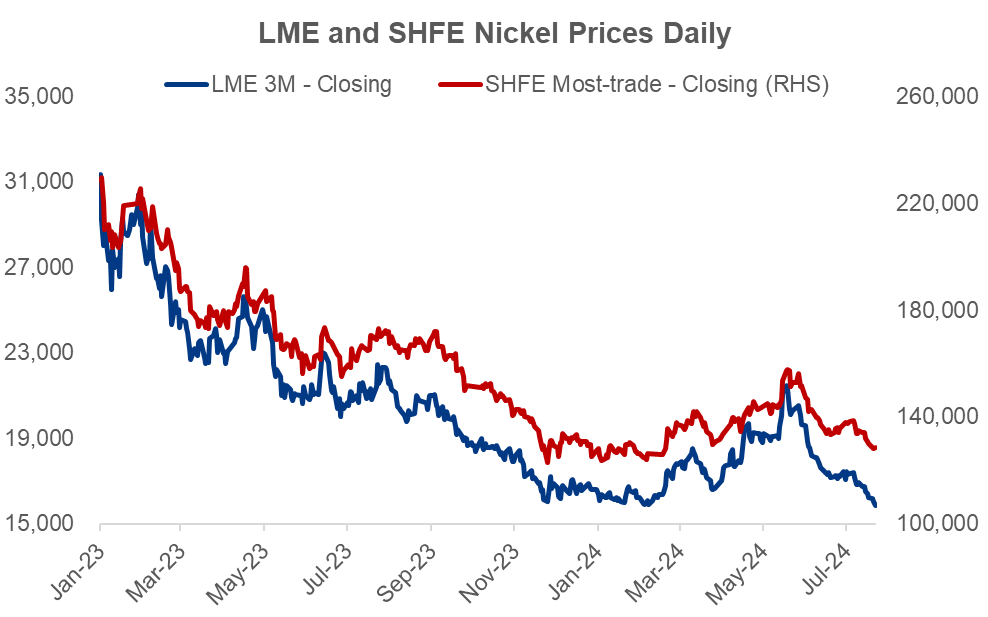

With LME nickel price falling once again below $16,000/tonne on July 24 on rising LME warrants, China's nickel prices are expected to stay on the downtrend in the long term amidst lingering oversupply, based on Mysteel estimate.

Sources: LME, SHFE

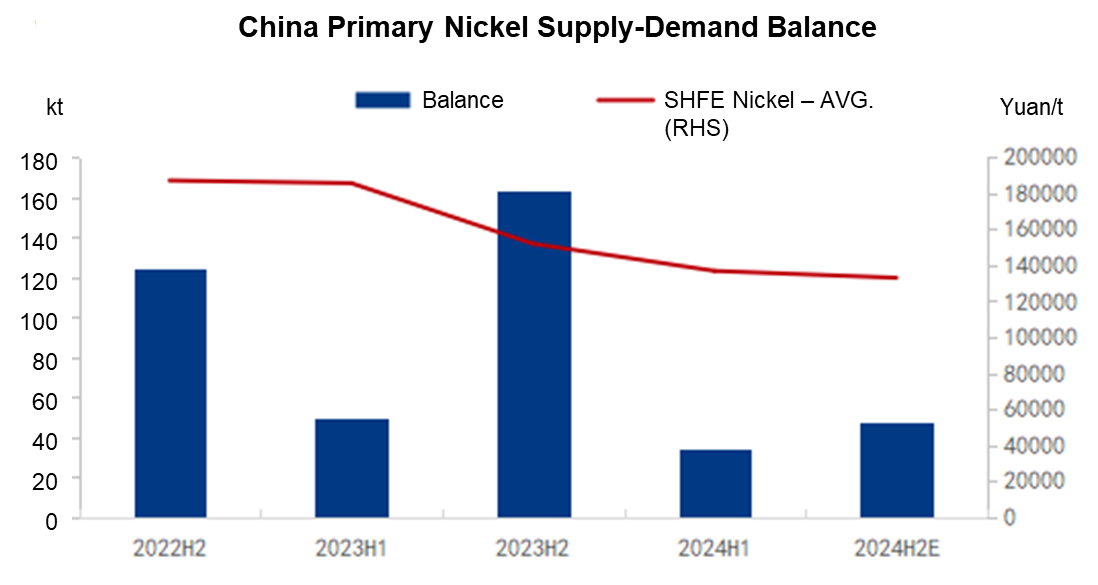

In the first half of 2024, China's primary nickel reported an oversupply of 33,900 tonnes in metal content, which narrowed significantly compared with that last year. But the market structure showed palpable changes.

First, the primary nickel oversupply was mostly contributed by pure nickel in H1 2024, rather than nickel intermediates in 2023. One of the reasons is that the RKAB approval disruption in Indonesia weighed on both the production and exports of nickel pig iron in 2024, and the robust stainless steel production in China quickly turned NPI from oversupply to narrow supply shortfall.

Second, though China and Indonesia still held most of the oversupplied primary nickel, the overseas market as a whole became fractionally short supplied amid narrowing supply and rising demand.

Source: Mysteel

To sum up, it is expected that the nickel prices will remain soft on lingering oversupply, especially pure nickel, in the long run. But the prices are projected to gain certain support from nickel ore supply crunch in Indonesia and nickel prices closing the break-even point of producers replying on outsourced raw materials.

Written by Aggie Hu, huchenying@mysteel.com