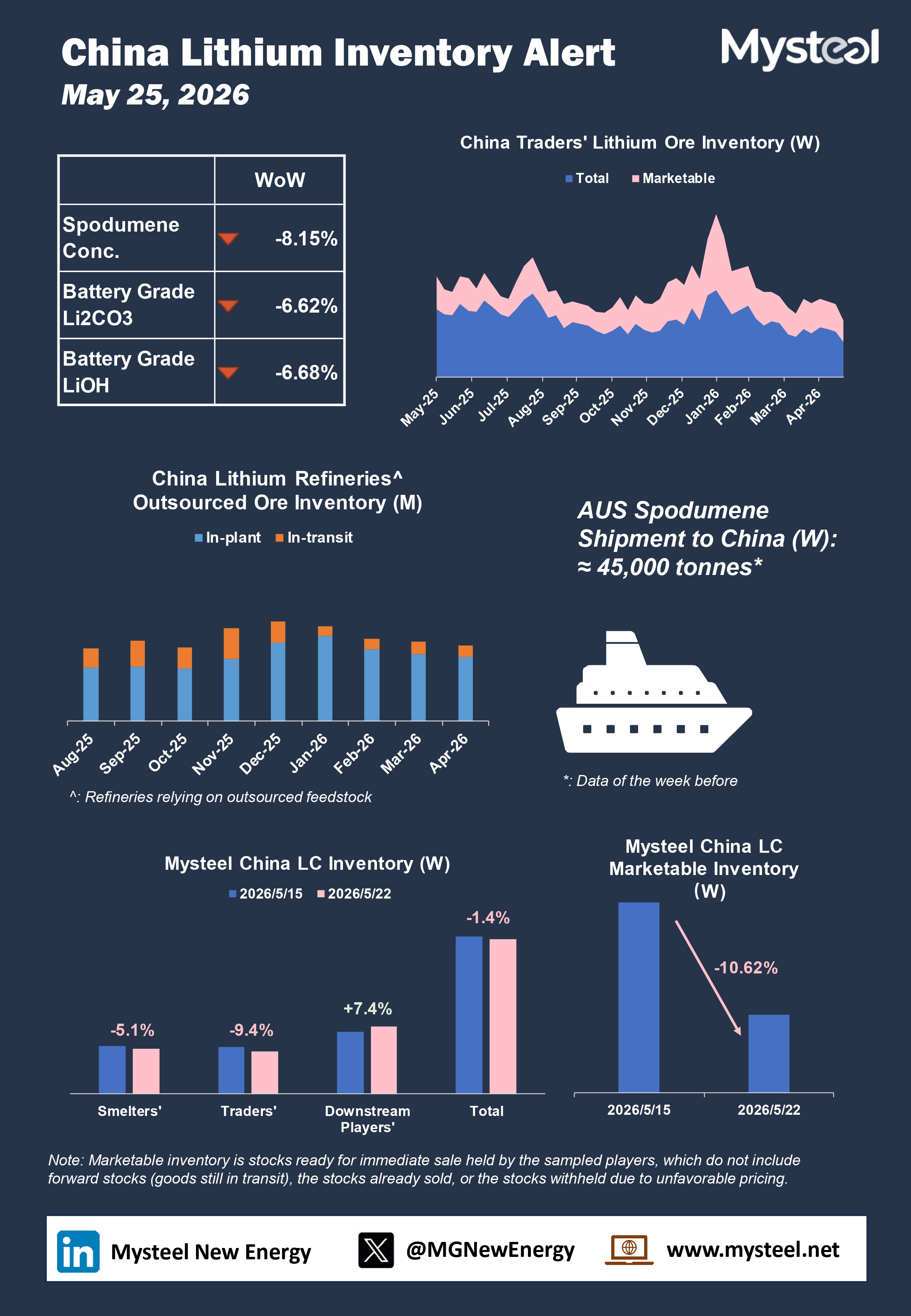

Over the past two weeks, the market has experienced significant volatility. According to Mysteel's analysis, the main drivers were a concentrated sell-off of hidden lithium carbonate inventories around the Yuan 200,000/tonne level, which disrupted the spot market, and a crackdown on invoicing practices among traders, which tightened their liquidity. As a result, the spot market's ability to absorb supply weakened, leading to a rapid price decline.

Our survey indicates that approximately 35,000 tonnes of lithium carbonate changed hands in the spot market over these two weeks, absorbing a significant portion of the excess liquidity.

Looking ahead to this week, market focus will shift to demand in June-July. Based on Mysteel's surveys and cros-validation with the industry chain, demand in June-July remains strong. Production schedules for lithium iron phosphate (LFP) battery cells in June are expected to increase by around 3-4% month-on-month compared with May.

On the supply side, June will continue to be constrained by tight lithium ore availability. While lithium refineries' inventories have been replenished to some extent, most of which came fromt he trader stocks, total domestic lithium ore inventories remain at low levels. A turning point in spot lithium ore supply is not expected until early July.

Therefore, Mysteel expects China's lithium carbonate balance sheet to remain in a drawdown of nearly 10,000 tonnes in June. In a phase highlighted by tight ore, ample lithium carbonate, and solid demand, lithium carbonate spot prices are expected to find effective support near the lithium ore cost line.