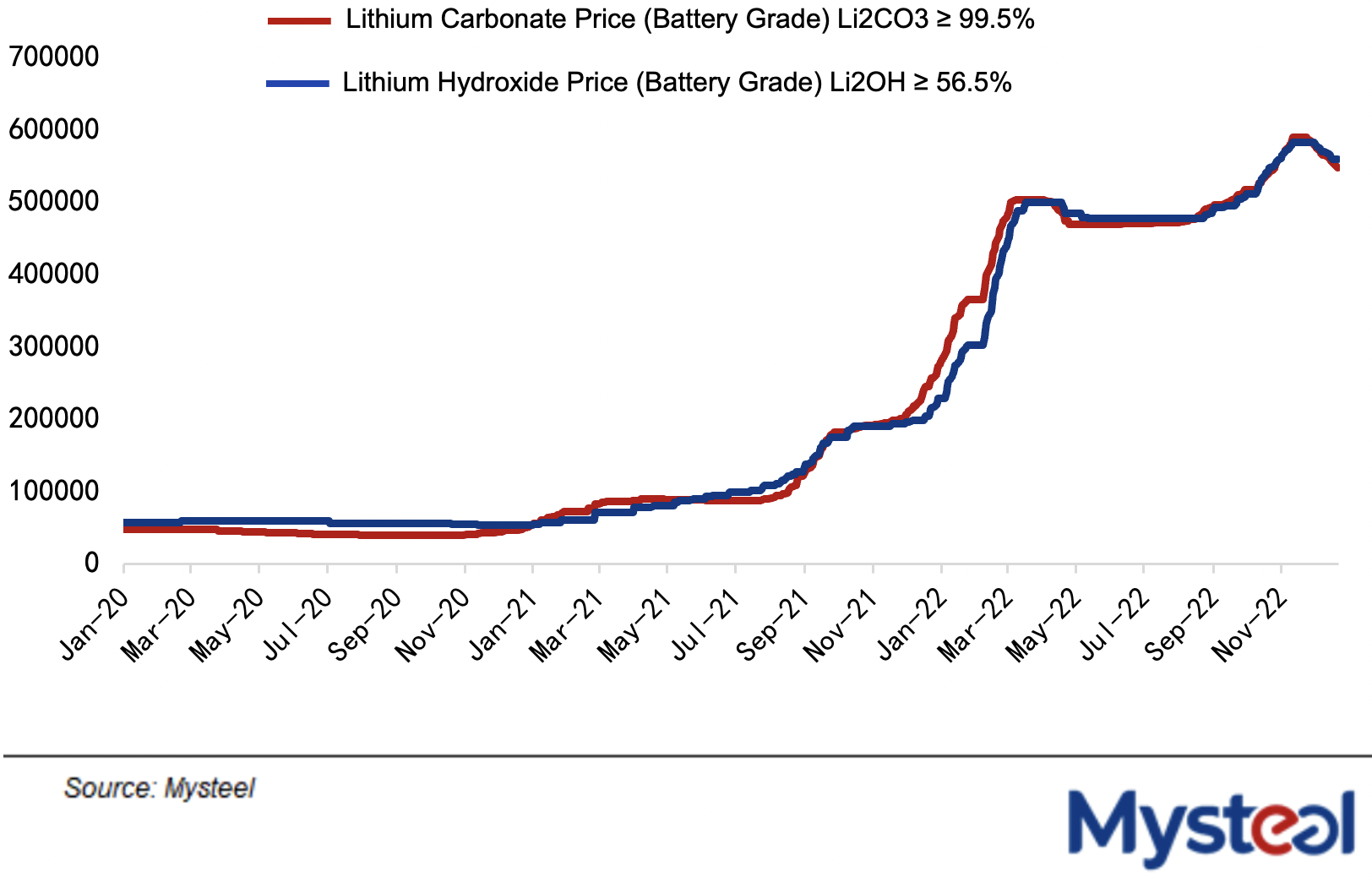

After hovering high at Yuan 590,000/tonne for nearly two weeks since November 11, the Chinese price of battery-grade lithium carbonate (Li2CO3) started to decrease on November 24 and lost a total of 6.89% to Yuan 547,000/t as of December 23, while the price of lithium hydroxide (LiOH) also fell 4.02% to Yuan 560,500/t, according to Mysteel's assessment. The overall price decline of lithium hydroxide was smaller than that of lithium carbonate, mainly owing to the fact that the price of lithium hydroxide is less sensitive to spot market fluctuations than lithium carbonate, as lithium hydroxide products are mostly traded among factories and have a higher proportion of long-term orders compared with lithium carbonate, which leads to fewer bulk goods of lithium hydroxide in the physical market.

Figure 1-1 Lithium hydroxide & lithium carbonate prices (unit Yuan/tonne)

In its sixth weekly report "Have Lithium Prices Hit the Peak" released on November 25, the Nonferrous Metal & New Energy Research Center of Mysteel has clearly pointed out that lithium compound prices were up close to the inflection point. Hence, Mysteel suggests that manufacturers who are not purchasing to meet their immediate production needs can restock lithium carbonate when the price falls to around Yuan 500,000/t. It is expected that transaction prices of lithium carbonate may stay rangebound between Yuan 400,000/t and Yuan 450,000/t next year.

Although the price of lithium carbonate has witnessed certain falls near the end of 2022, this weekly report again suggests that lithium carbonate price may ease further in the short term, and buyers need to pay attention to possible risks brought by the decline of lithium carbonate price.

On the supply side, the output of lithium carbonate decreased by around 3,000 tonnes due to the impact of the previous environmental protection investigation on lithium compound manufacturers in Yichun, Jiangxi province in early December, thus the domestic output in December is expected to be less than that in November. Moreover, because of seasonal factors, the output of refined lithium carbonate in the first quarter is usually 20% lower than that in the fourth quarter, and the output from salt lakes in the first quarter will also be lower compared with the fourth quarter due to the colder weather. The decline in lithium ore output will lead the run rate of lithium compound plants to keep dropping. In addition, the lithium compound plants will conduct regular maintenance works in the first quarter of every year, so the output of lithium carbonate is expected to fall by 15%-20% in the first quarter.

On the demand side, according to Mysteel's research, the pickup cycle of popular new energy vehicles (NEVs) has been shortened to one to four weeks, and battery makers have also lowered their scheduled production in December. It is expected that the planned production of key battery plants will still see an on-month decrease of 10% in January. Cathode material manufacturers - major lithium compounds buyers - also revised down their production schedule in December and January. Some ternary cathode manufacturers reduced their output by about 35% month on month in December, and some lithium iron phosphate (LFP) cathode manufacturers trimmed their output by about 15% month on month.

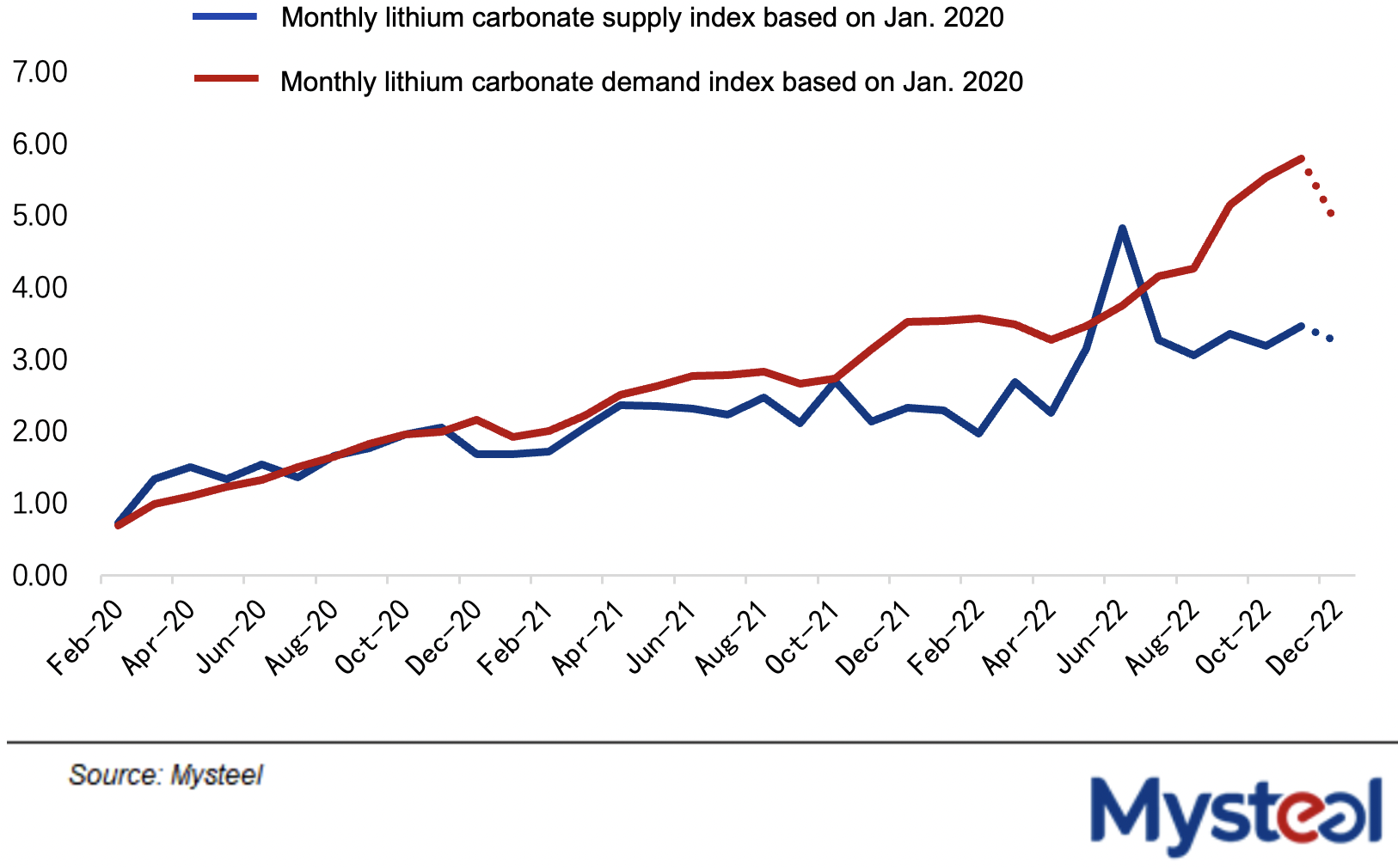

Based on the lithium carbonate supply and demand gap model, the gap between the two curves of supply and demand started to narrow in December, indicating that the price of lithium carbonate may still trend down going forward. However, the curve representing lithium carbonate demand has yet to go down to intersect with the supply curve at present, which means that the current fundamentals will not lead to a persistent decline in the price of lithium carbonate in the long term. The recent price decline is mainly affected by short-term supply and demand fluctuations, and the price of lithium carbonate is expected to rebound somewhat after downstream manufacturers increase their output of cathode materials month on month in March.

Figure 1-2 Lithium carbonate supply and demand gap model

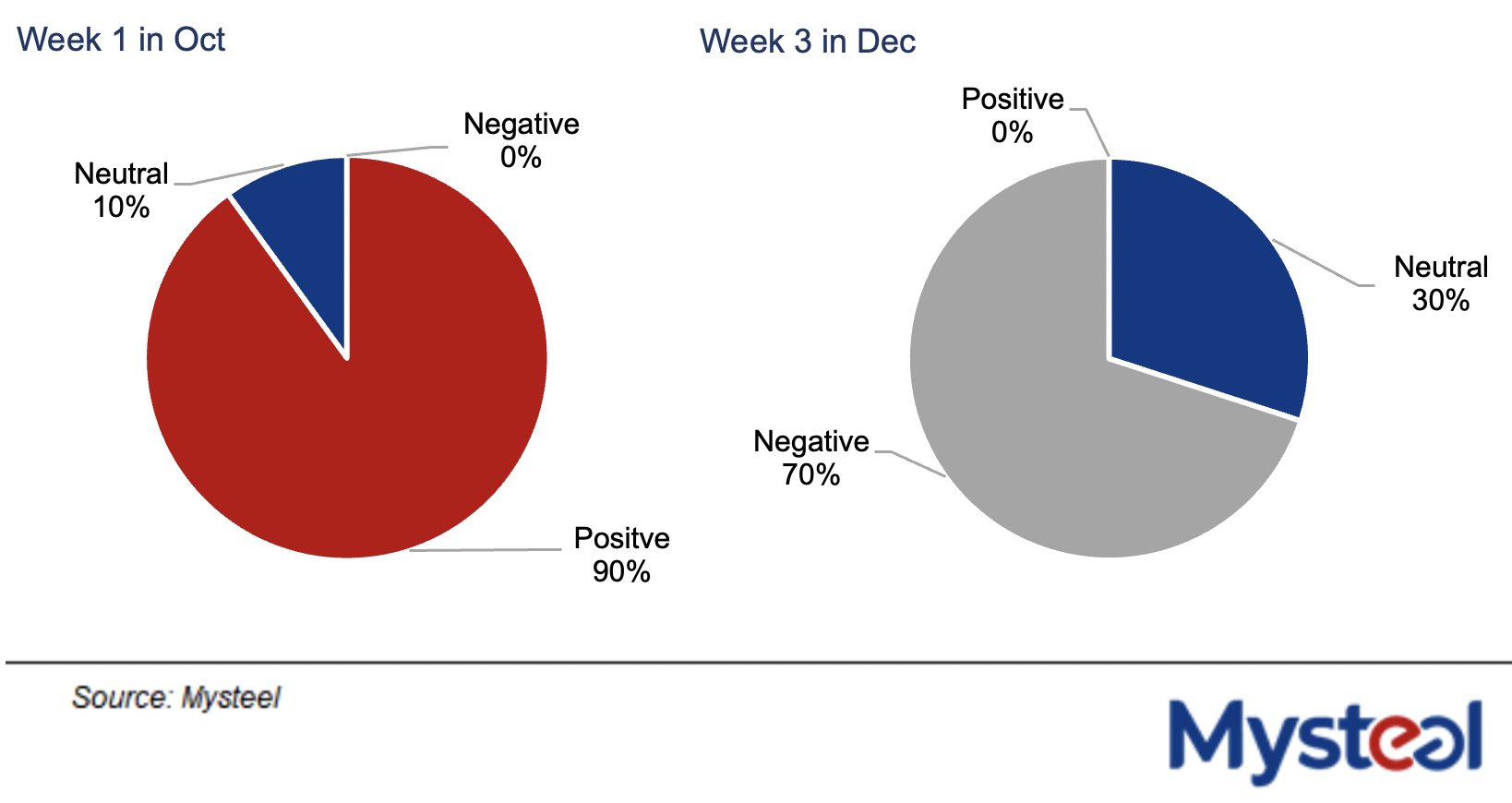

According to Mysteel's survey, the cathode manufacturers' lithium compound inventories can last for about one month of use. Cathode manufacturers indicated that they were mainly consuming stocks at hand and buying low-priced lithium compounds to meet immediate needs given the relatively high prices of lithium compounds. Traders were panicking, and some trimmed their offering prices and concluded deals, mostly back-to-back, whenever there were profit margins in hopes of withdrawing funds quickly, which sped up the decline of lithium compound prices.

Figure 1-3 Lithium compound market sentiment survey

It is expected that the sales of domestic new energy passenger vehicles will reach 1 million units in the first quarter of next year, mainly due to the signs of a weak downstream demand shown in the year-end car assembly data, as well as the impacts of the Chinese New Year holiday break, the widely circulating COVID infections and the end of NEV subsidies. In addition, the downgraded forecast of end-users' demand next year may have a great impact on the production schedules of battery plants and cathode materials plants. The lithium carbonate price is expected to remain weak in January and February, providing more bargaining power for lithium carbonate buyers.

Written by Mysteel Nonferrous Metal & New Energy Research Center

Edited by Ruby Zhang, zhangjiajing@mysteel.com; Alyssa Ren, rentingting@mysteel.com