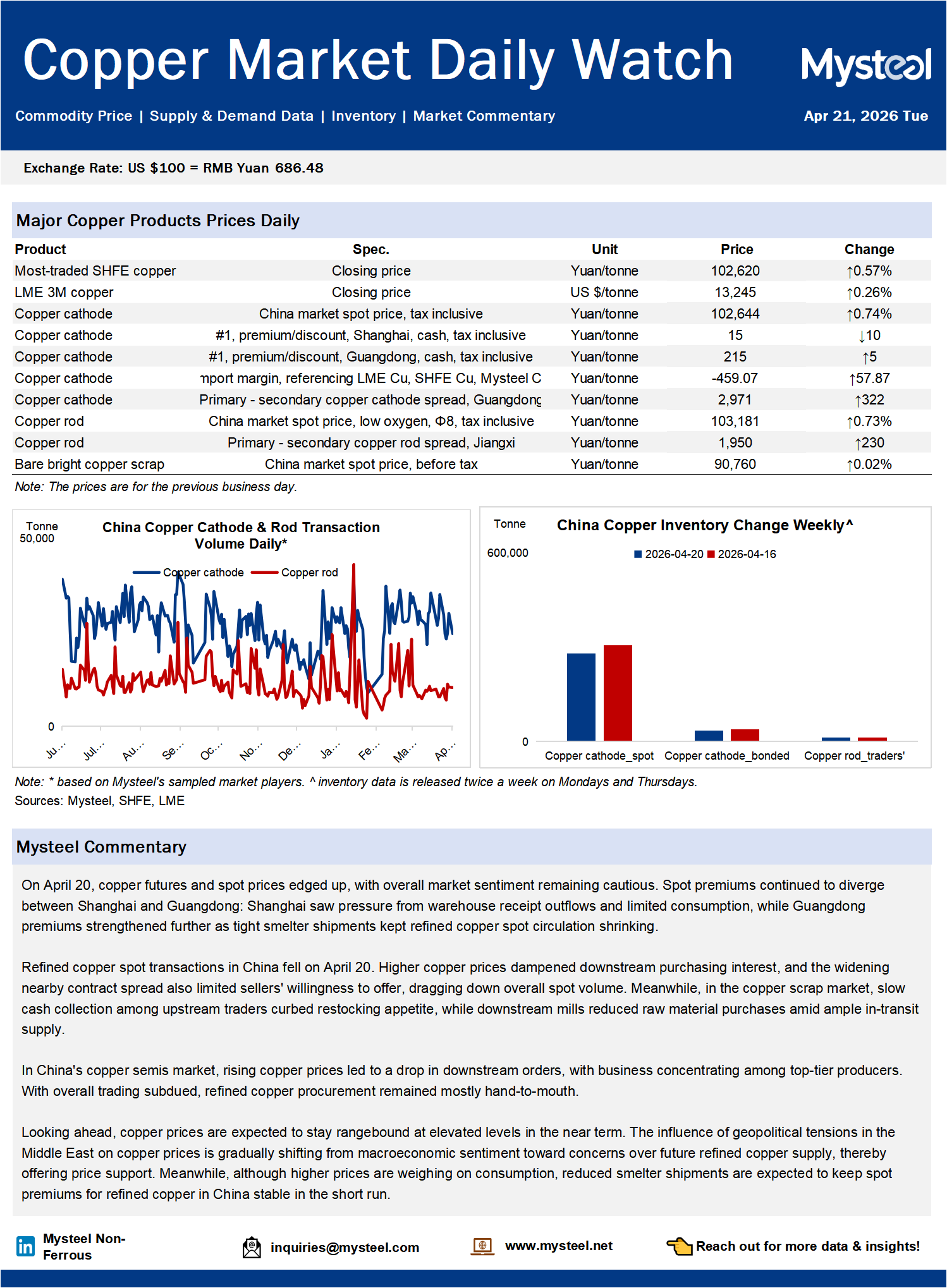

On April 20, copper futures and spot prices edged up, with overall market sentiment remaining cautious. Spot premiums continued to diverge between Shanghai and Guangdong: Shanghai saw pressure from warehouse receipt outflows and limited consumption, while Guangdong premiums strengthened further as tight smelter shipments kept refined copper spot circulation shrinking. Refined copper spot transactions in China fell on April 20. Higher copper prices dampened downstream purchasing interest, and the widening nearby contract spread also limited sellers' willingness to offer, dragging down overall spot volume. Meanwhile, in the copper scrap market, slow cash collection among upstream traders curbed restocking appetite, while downstream mills reduced raw material purchases amid ample in-transit supply. In China's copper semis market, rising copper prices led to a drop in downstream orders, with business concentrating among top-tier producers. With overall trading subdued, refined copper procurement remained mostly hand-to-mouth. Looking ahead, copper prices are expected to stay rangebound at elevated levels in the near term. The influence of geopolitical tensions in the Middle East on copper prices is gradually shifting from macroeconomic sentiment toward concerns over future refined copper supply, thereby offering price support. Meanwhile, although higher prices are weighing on consumption, reduced smelter shipments are expected to keep spot premiums for refined copper in China stable in the short run.

Don't miss Mysteel's Q2 2026 Copper Market FREE Webinar! Check the link below to learn more, and register to secure your spots:

Q2 2026 Copper: Price Volatility, Raw Material Tightness, and What's Next?