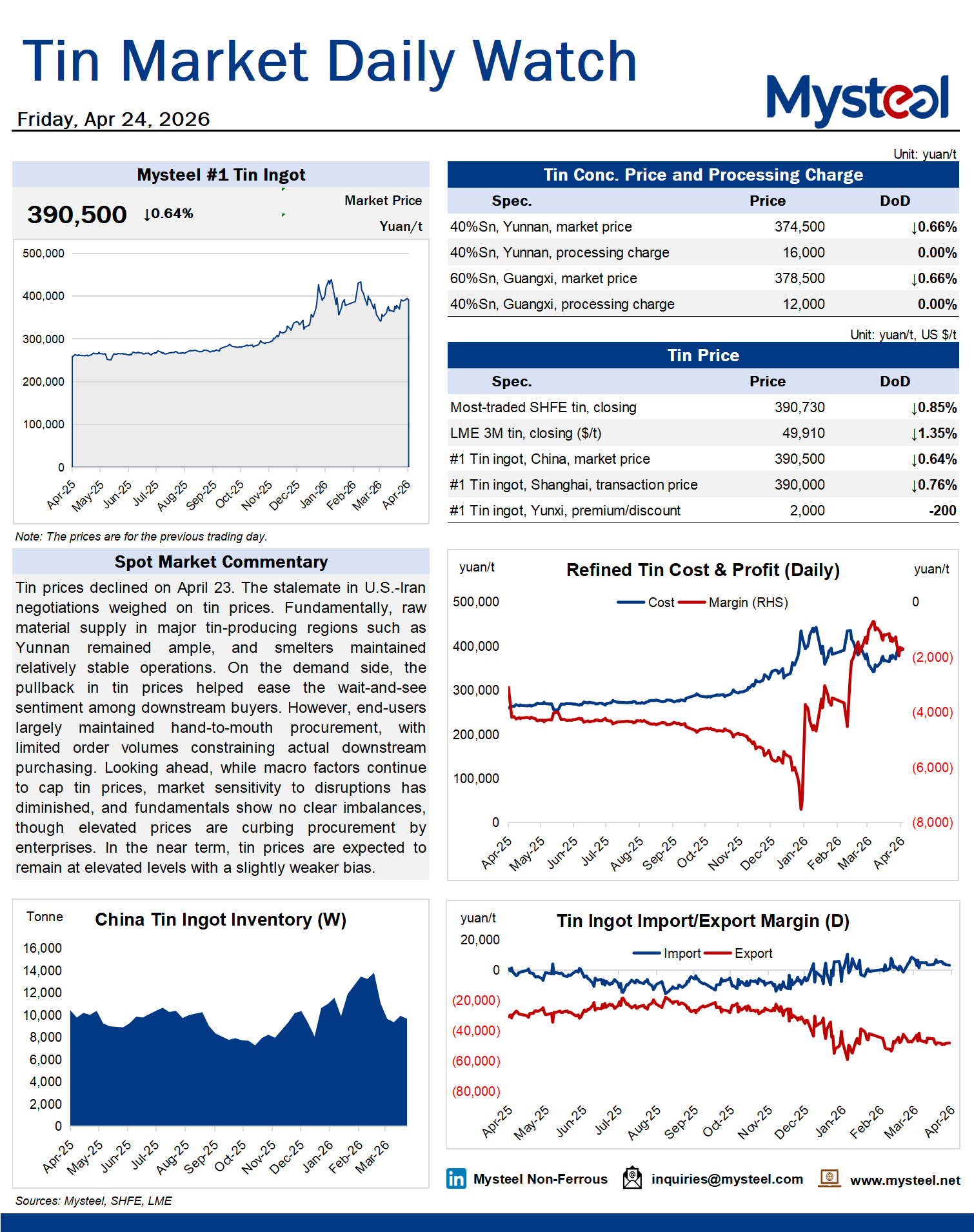

Tin prices declined on April 23. The stalemate in U.S.-Iran negotiations weighed on tin prices. Fundamentally, raw material supply in major tin-producing regions such as Yunnan remained ample, and smelters maintained relatively stable operations. On the demand side, the pullback in tin prices helped ease the wait-and-see sentiment among downstream buyers. However, end-users largely maintained hand-to-mouth procurement, with limited order volumes constraining actual downstream purchasing. Looking ahead, while macro factors continue to cap tin prices, market sensitivity to disruptions has diminished, and fundamentals show no clear imbalances, though elevated prices are curbing procurement by enterprises. In the near term, tin prices are expected to remain at elevated levels with a slightly weaker bias.