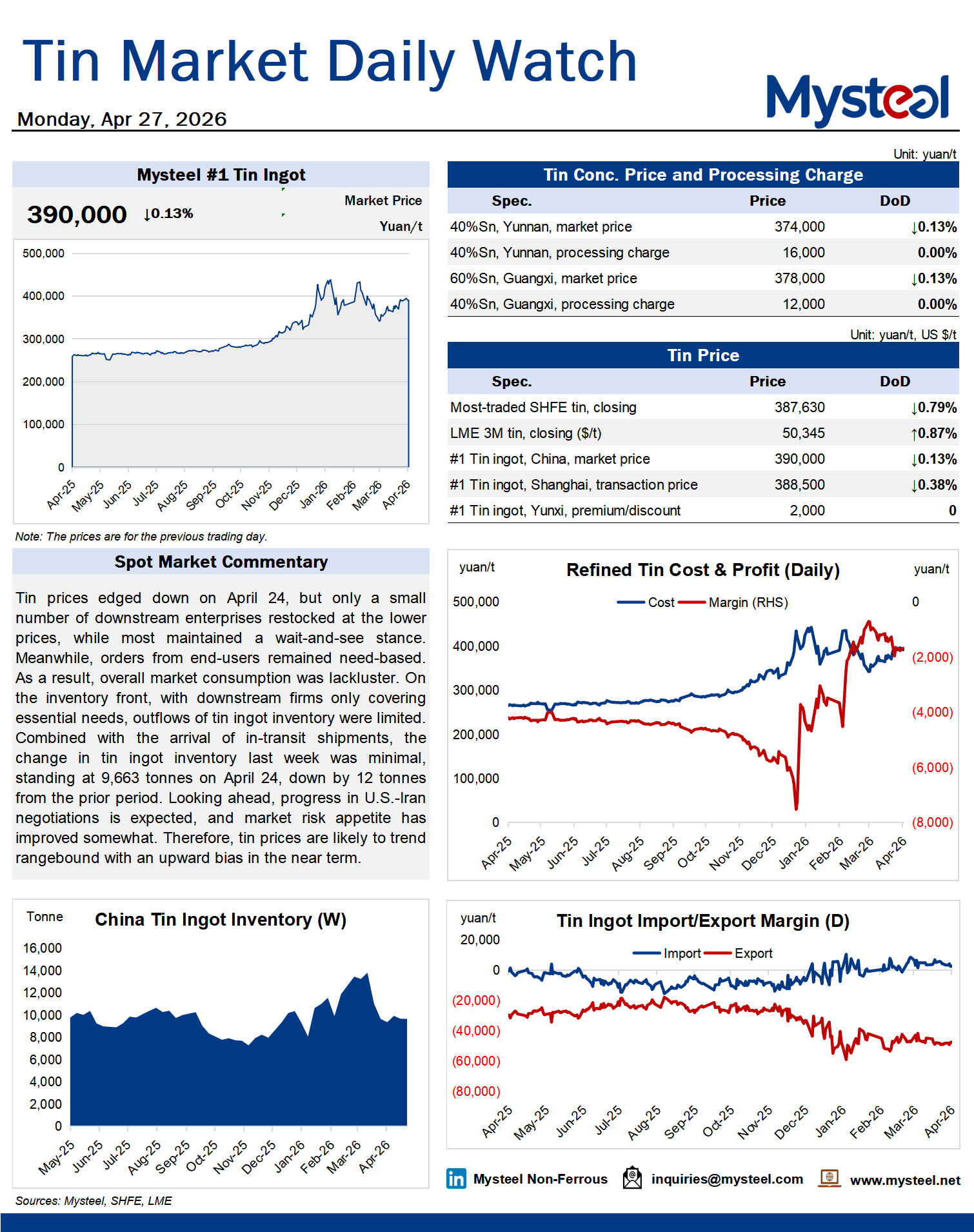

Tin prices edged down on April 24, but only a small number of downstream enterprises restocked at the lower prices, while most maintained a wait-and-see stance. Meanwhile, orders from end-users remained need-based. As a result, overall market consumption was lackluster. On the inventory front, with downstream firms only covering essential needs, outflows of tin ingot inventory were limited. Combined with the arrival of in-transit shipments, the change in tin ingot inventory last week was minimal, standing at 9,663 tonnes on April 24, down by 12 tonnes from the prior period. Looking ahead, progress in U.S.-Iran negotiations is expected, and market risk appetite has improved somewhat. Therefore, tin prices are likely to trend rangebound with an upward bias in the near term.