On April 28, 2026, Huayou Cobalt issued an announcement stating that due to a sharp rise in sulfur prices and high-capacity operation of its production lines, its subsidiary PT. Huafei Nickel Cobalt would temporarily suspend some production lines for maintenance starting May 1, with an estimated impact of about 50% of production. As the world's largest nickel intermediate product project, news of significant production cuts at PT. Huafei Nickel Cobalt quickly triggered market reaction, and nickel prices moved sharply higher during the night session.

According to Mysteel survey, other Indonesia's HPAL projects, including Lygend, Blue Sparking, and Huayue, also experienced varying degrees of maintenance or reduced operation. Although projects such as QMB had recently resumed production and the new project, Excelsior Nickel Cobalt, had entered the commissioning preparation phase, both would still take time to recover or ramp up. Overall, a clear signal of tightening MHP supply had emerged.

Meanwhile, market quotations reacted in advance. The payable rate of MHP had recently risen to 95% for nickel and 92% for cobalt, significantly higher than earlier levels. Sulfur supply shortages were moving from expectation to reality, transmitting step by step along the chain: from sulfur to MHP to nickel sulfate to electrowinning nickel.

I. Multiple Pressures Weigh on MHP Supply

1. RKAB Quota Cuts Take Effect, WBN Production Halt Impact Emerges

Indonesia's Ministry of Energy and Mineral Resources had set the full-year 2026 nickel ore quota at 260-270 million tonnes, a reduction of over 30% from the actual 379 million tonnes implemented in 2025. On April 16, the Ministry issued administrative sanction warnings to 106 companies that had not submitted RKAB applications, of which 39 were sanctioned with 60-day production halts.

In addition, PT Weda Bay Nickel (WBN), Indonesia's largest nickel miner, received an initial 2026 quota of only 12 million tonnes, a sharp reduction from the 42 million tonnes actually executed in 2025. By the second quarter, its quota was nearly exhausted, and the mine would enter care and maintenance from mid-May. WBN is the core mine supplying ore to the IWIP park on Halmahera Island. Its production halt forced HPAL projects in the park to source ore from other islands, increasing logistics costs and causing issues such as unstable quality and lower supply reliability, further pushing up the all-in cost of MHP.

2. Previously Halted Maintenance Projects Resume, but Ramp-up Takes Time

HPAL projects such as QMB, which had been suspended due to a tailings incident in February, had recently resumed production, but overall operating rates remained low and were still far from full capacity. Given the time required to restart and stabilize production systems, significant supply contributions were unlikely in the near term. According to GEM's first-quarter report, its Indonesian nickel resource project had resumed production in April 2026, with first-quarter nickel shipments of 20,422 tonnes (including capacity from equity investments). Nevertheless, given the overall scale of HPAL production cuts in Indonesia, the total MHP supply remained tight.

3. Sulfur Supply Shortage Persists, Prices Hit New Highs

The HPAL process consumes approximately 10 tonnes of sulfur per nickel tonne of MHP. About 76-80% of Indonesia's sulfur is imported from the Middle East, and the blockade of the Strait of Hormuz directly impacted the lifeline of MHP production. To address the supply disruption, Indonesian companies had tried various alternatives. According to Mysteel Oilchem data, three sulfur cargo vessels from Canada had arrived in Indonesia since March, totaling about 150,000 tonnes; other vessels had arrived from Saudi Arabia's Yanbu port. Some companies also directly imported sulfuric acid or used local pyrite to produce acid. However, compared to the huge gap left by the Persian Gulf supply disruption, these supplementary measures were limited in scale and came at high cost.

Currently, sulfur transaction prices in the Indonesian market have surpassed US $1,000/tonne, with some quotations reaching as high as US $1,200/tonne, representing a 3.5-fold increase from the same period last year and a more than 10-fold increase from the same period in 2024. Sulfur's share of total MHP production costs had exceeded 50%. With existing projects already operating at reduced capacity, industry sulfur inventories could sustain at most two to three months. If shipping routes were not restored in the near term, more HPAL projects would face the risk of production cuts or even shutdowns.

4. New HPM Formula Implemented, Nickel Ore Benchmark Prices Surge

On April 14, Indonesia's Ministry of Energy and Mineral Resources issued Ministerial Decree No. 144, which took effect on April 15. The new formula changed nickel ore pricing from a "nickel-only" basis to a multi-element composite valuation including nickel, iron, cobalt, and chromium. Limonite ore used in HPAL refining, which has a higher cobalt content, saw a sharp increase in HPM under the new formula, with benchmark prices for certain grades more than doubling compared to the previous rules. Although the policy had not immediately pushed up actual transaction prices (mines and smelters were still negotiating), it had significantly raised market expectations of future costs. Mines had grown more inclined to hold firm on prices, and smelters faced upward pressure on future raw material costs.

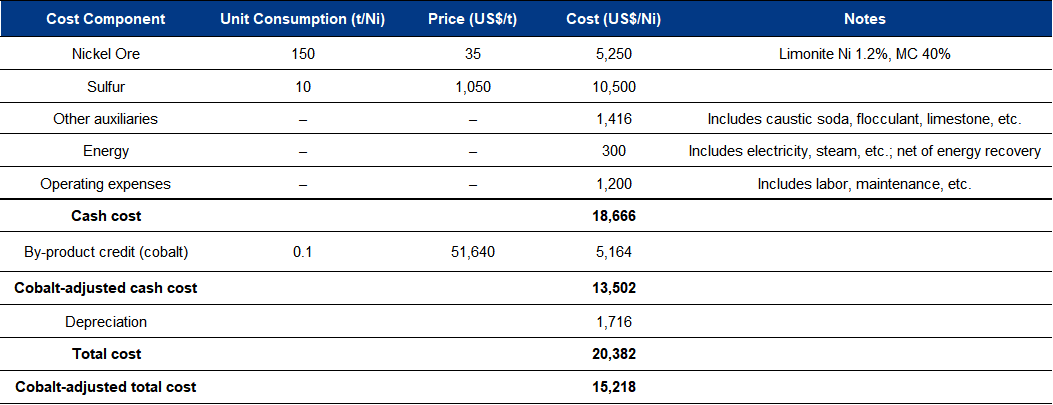

Indonesia's MHP Production Cost Estimate:

Based on the multiple factors discussed above, Mysteel estimated the all-in cost of Indonesian MHP as follows. The unit consumption and price assumptions for each project were based on current market conditions:

Source: Mysteel

Note: The above data are comprehensive estimates by Mysteel based on current market information. Actual costs varied by project depending on differences in process technology, ore sources, scale, and bargaining power.

II. Transmission Effects: How MHP Production Cuts Impact the Industry Chain

1. MHP: Operating Rates Fell Across Projects, and the Production Continued to Decline

According to Mysteel's survey of nine sample projects in Indonesia, MHP production in Indonesia stood at 27,200 tonnes in April 2026 (down 16.31% month-on-month, down 13.07% year-on-year). The cumulative production for January-April reached 139,400 tonnes (down 4.05% year-on-year). Production had declined month by month over the first four months of the year, and May production was estimated to fall further to 26,300 tonnes (down 33.18% year-on-year).

Source: Mysteel

Looking ahead, MHP production trends would depend on the following three key variables:

(1) Whether the Strait of Hormuz would reopen: About 76-80% of Indonesia's sulfur was imported from the Middle East, and the blockade directly cut off the main source. If shipping resumed in the short term, sulfur supply would improve quickly and MHP production would likely recover. Otherwise, the shortage would persist.

(2) Whether alternative solutions could be implemented: Companies had tried importing sulfur from distant regions such as Canada, directly importing sulfuric acid, and using local pyrite to produce acid. However, there was significant uncertainty over whether these alternatives could be sustained in terms of volume and cost.

(3) Changes in HPAL ore prices under the new HPM formula: The new rules had raised the benchmark price for limonite, and mines were more inclined to hold firm on prices. If actual transaction prices rose, smelter margins would be further compressed, potentially forcing additional production cuts.

Consider a scenario: in the extreme case of a continued blockade of the Strait of Hormuz, existing sulfur inventories, based on current production rates, would last approximately 2-4 months. Thereafter, production would rely solely on alternative sources:

- According to Mysteel Oilchem data, sulfur cargo vessels from distant regions such as Canada and from ports on Saudi Arabia's western coast would arrive in Indonesia at an average rate of 1-2 vessels per month, bringing about 50,000-80,000 tonnes of sulfur per month, corresponding to approximately 5,000-8,000 tonnes (in Ni. content) of MHP;

- Direct imports of sulfuric acid: based on an average import volume of about 1.1 million tonnes per year over the past few years, this would support roughly 3,000-4,000 tonnes (in Ni. content) of MHP per month on a monthly average basis;

- Sulfuric acid supply from local pyrite acid plants: would support about 2,000-4,000 tonnes (in Ni. content) per month.

Together, these three sources would only sustain a total MHP production of approximately 10,000-16,000 tonnes in Ni. content per month, a reduction of more than 60% from normal levels at the beginning of the year (about 40,000 tonnes per month). In this scenario, full-year 2026 Indonesian MHP production could be significantly revised downward from the previously expected 550,000 tonnes to a range of 300,000-350,000 tonnes.

2. Nickel Matte: Production Increased Driven by Profits, but Unable to Fully Fill the Gap

(1) MHP Gap Needed to Be Filled by Nickel Matte

China's 2026 nickel sulfate production was expected to reach 600,000 tonnes in Ni. content, of which the MHP route accounted for about 60% and the nickel matte route about 30%. If MHP monthly production fell to 16,000 tonnes in Ni. content, a reduction of about 25,000 tonnes in Ni. Content per month from normal levels, the corresponding monthly raw material gap for nickel sulfate would be approximately 15,000 tonnes in Ni. content, which theoretically needed to be filled by nickel matte.

(2) Comparison of RKEF Production Line and NPI Profits

A key factor in whether nickel matte production could increase was the profitability of NPI produced from the same RKEF lines. The profit comparison between the two directly determined smelters' willingness to switch production lines. According to Mysteel estimates, the cash cost of nickel matte was currently US $15,811/tonne in Ni. content, with a profit of about US $2,000/tonne in Ni. content. For Indonesian NPI, taking the Morowali production area as an example, the cash cost was US $12,735/tonne in Ni. content, and the FOB price reached US $144 per nickel unit, translating to a profit of US $1,665/tonne in Ni. content. Nickel matte profits were more than US $300/tonne in Ni. content higher than NPI profits, strengthening smelters' willingness to switch production driven by profitability.

(3) Production Increases Constrained by Equipment and Grade, Gap Hard to Fill In the Short Term

Currently, about 49 RKEF production lines could switch between nickel matte and NPI, with a total capacity of about 680,000 tonnes in Ni. content, and the current utilization rate was about 50%. However, switching to nickel matte required sulfur addition equipment and converter retrofits, and also had requirements for feed ore grade. It was estimated that only 2,000-3,000 tonnes in Ni. content per month could be added in May-June, a modest increase that would be difficult to fully fill the nickel sulfate raw material gap caused by the MHP reduction.

3. Nickel Sulfate & Refined Nickel: MHP Supply Disruption Had Far-Reaching Effects

(1) Nickel sulfate: Replacing MHP with nickel matte required equipment modifications

MHP was the dominant feedstock for China's nickel sulfate production, accounting for about 60% of the raw material mix. If MHP production fell sharply, nickel matte could theoretically fill the gap. However, the processing routes for MHP and nickel matte differed. Not all existing nickel sulfate production lines could directly switch feedstocks; modifications such as leaching and impurity removal equipment needed to be purchased or retrofitted, a lengthy process that could not respond quickly. Therefore, even if nickel matte production increased, it would be difficult to effectively offset the impact of the MHP gap on nickel sulfate production in the short term.

(2) Refined nickel: MHP accounted for a significant share of feedstock, and the production faced downward pressure

China's refined nickel production in 2026 was expected to reach approximately 436,300 tonnes in Ni. content, of which about 144,000 tonnes in Ni. Content (approximately 33%) would be produced using MHP as feedstock. If MHP supply continued to tighten, this portion of refined nickel capacity would face the risk of raw material shortages, potentially forcing production cuts or a switch to alternative feedstocks such as nickel matte. However, such a switch would also face process adjustments and upward cost pressure. If refined nickel production fell as a result, global refined nickel supply would tighten further, providing support to nickel prices.

Looking ahead, in the near term, the market is expected to digest the above supply contraction news after the Labour Day holiday. SHFE nickel is expected to find support above Yuan 150,000/tonne, and a move toward Yuan 155,000-160,000/tonne could not be ruled out. If the sulfur supply channel is not reopened before June, MHP production cuts would move from expectation to full-scale reality, potentially pushing SHFE nickel toward Yuan 160,000-170,000/tonne, with LME nickel prices correspondingly at US $22,000-23,500/tonne. Conversely, nickel prices could fall back below Yuan 140,000/tonne. Market participants are advised to closely monitor changes in the international situation, the implementation of production cuts at Indonesian projects, and the latest developments in Indonesian nickel ore policies.

Written by Cora Ji, jiruyan@mysteel.com

----------------------------------

Stay Ahead – Subscribe to Our Nickel Weekly Report | Get weekly updates on prices, supply-demand, production status, raw material costs, and short-term forecasts. Please contact inquiries@mysteel.com for trial reading!