On May 7, copper prices saw limited fluctuations, with slight increases in China's futures and spot markets but a constrained decline at the London Metal Exchange. Entering May, attention is needed on potential macroeconomic disruptions on copper prices, amid the U.S. president's plan to visit China in mid-May, uncertainty regarding the Middle East conflict, as well as the Federal Reserve's leadership transition.

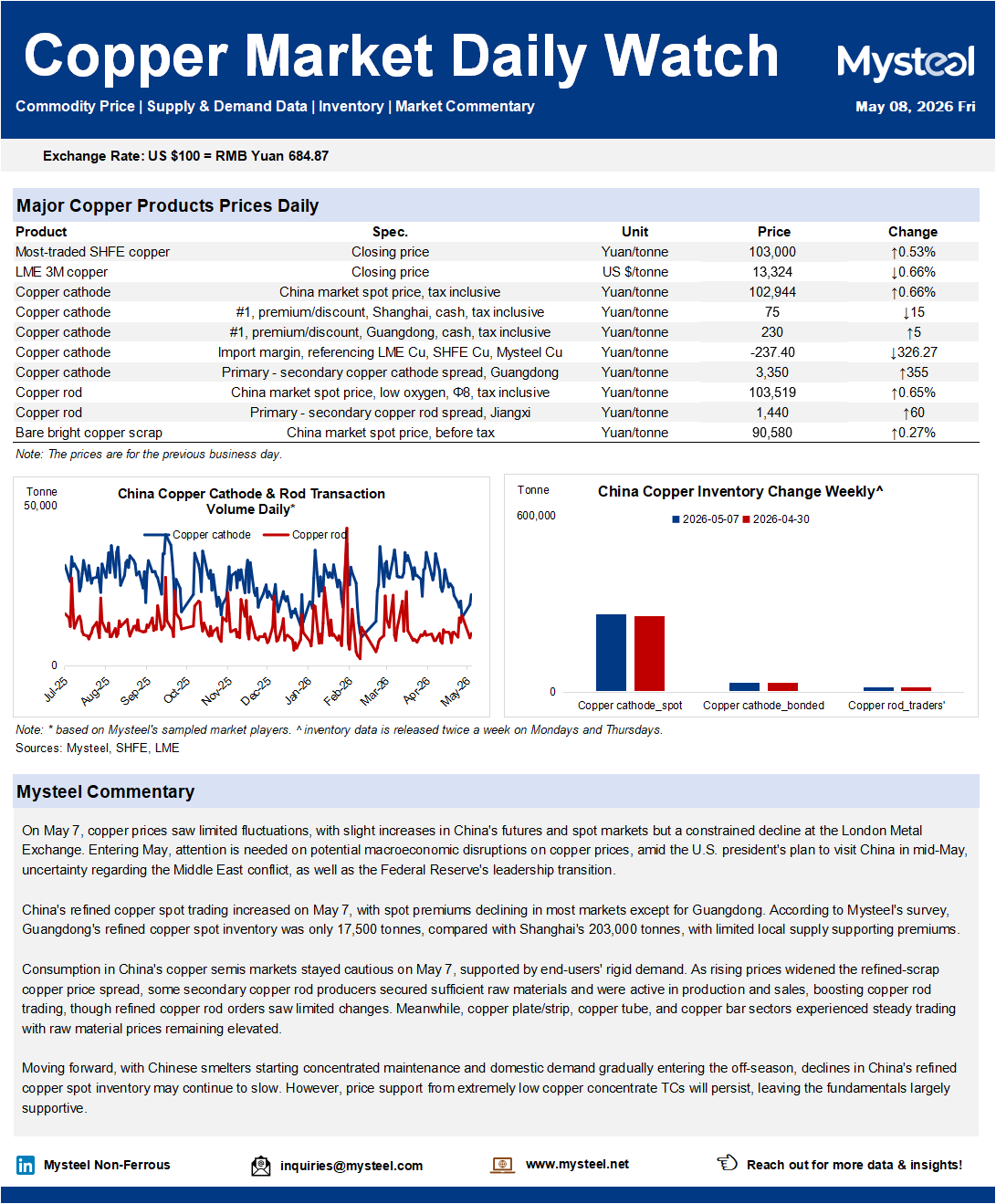

China's refined copper spot trading increased on May 7, with spot premiums declining in most markets except for Guangdong. According to Mysteel's survey, Guangdong's refined copper spot inventory was only 17,500 tonnes, compared with Shanghai's 203,000 tonnes, with limited local supply supporting premiums.

Consumption in China's copper semis markets stayed cautious on May 7, supported by end-users' rigid demand. As rising prices widened the refined-scrap copper price spread, some secondary copper rod producers secured sufficient raw materials and were active in production and sales, boosting copper rod trading, though refined copper rod orders saw limited changes. Meanwhile, copper plate/strip, copper tube, and copper bar sectors experienced steady trading with raw material prices remaining elevated.

Moving forward, with Chinese smelters starting concentrated maintenance and domestic demand gradually entering the off-season, declines in China's refined copper spot inventory may continue to slow. However, price support from extremely low copper concentrate TCs will persist, leaving the fundamentals largely supportive.