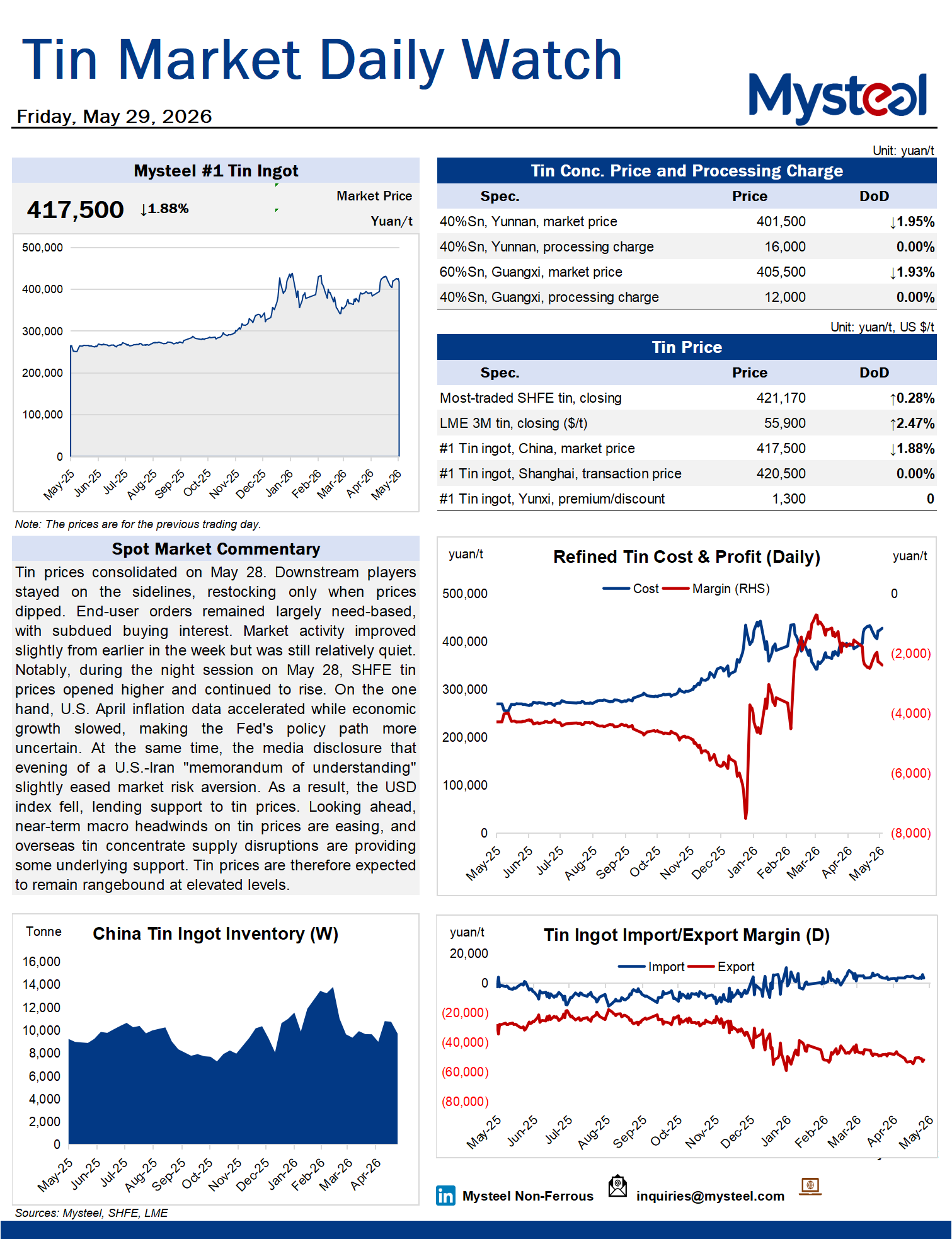

Tin prices consolidated on May 28. Downstream players stayed on the sidelines, restocking only when prices dipped. End-user orders remained largely need-based, with subdued buying interest. Market activity improved slightly from earlier in the week but was still relatively quiet. Notably, during the night session on May 28, SHFE tin prices opened higher and continued to rise. On the one hand, U.S. April inflation data accelerated while economic growth slowed, making the Fed's policy path more uncertain. At the same time, the media disclosure that evening of a U.S.-Iran "memorandum of understanding" slightly eased market risk aversion. As a result, the USD index fell, lending support to tin prices. Looking ahead, near-term macro headwinds on tin prices are easing, and overseas tin concentrate supply disruptions are providing some underlying support. Tin prices are therefore expected to remain rangebound at elevated levels.