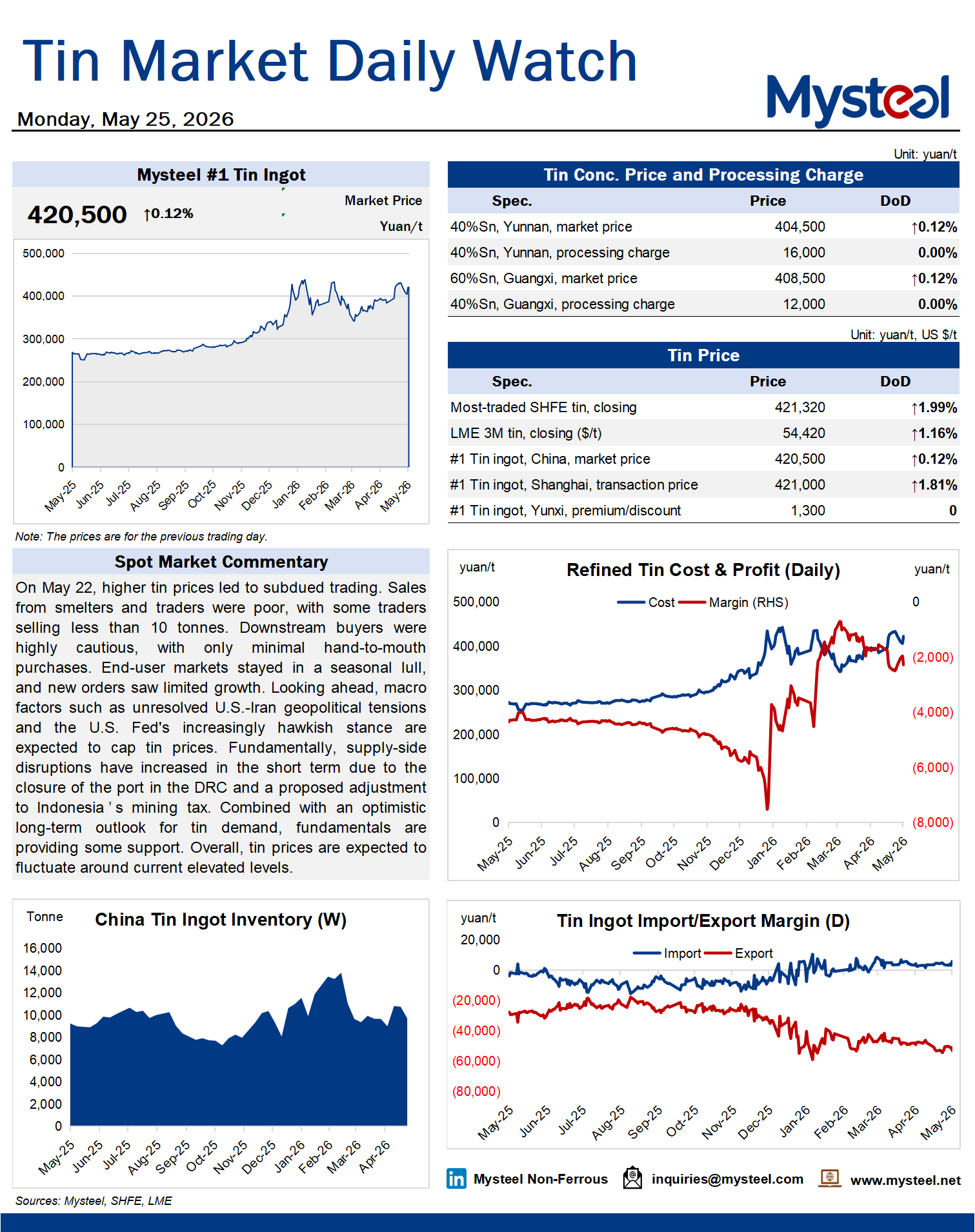

On May 22, higher tin prices led to subdued trading. Sales from smelters and traders were poor, with some traders selling less than 10 tonnes. Downstream buyers were highly cautious, with only minimal hand-to-mouth purchases. End-user markets stayed in a seasonal lull, and new orders saw limited growth. Looking ahead, macro factors such as unresolved U.S.-Iran geopolitical tensions and the U.S. Fed's increasingly hawkish stance are expected to cap tin prices. Fundamentally, supply-side disruptions have increased in the short term due to the closure of the port in the DRC and a proposed adjustment to Indonesia's mining tax. Combined with an optimistic long-term outlook for tin demand, fundamentals are providing some support. Overall, tin prices are expected to fluctuate around current elevated levels.